3 Mary Hobbes joined the board of Rosh and Company, a large retailer, as finance director earlier this year. Whilst shewas glad to have finally been given the chance to become finance director after several years as a financialaccountant, she also quickly

题目

3 Mary Hobbes joined the board of Rosh and Company, a large retailer, as finance director earlier this year. Whilst she

was glad to have finally been given the chance to become finance director after several years as a financial

accountant, she also quickly realised that the new appointment would offer her a lot of challenges. In the first board

meeting, she realised that not only was she the only woman but she was also the youngest by many years.

Rosh was established almost 100 years ago. Members of the Rosh family have occupied senior board positions since

the outset and even after the company’s flotation 20 years ago a member of the Rosh family has either been executive

chairman or chief executive. The current longstanding chairman, Timothy Rosh, has already prepared his slightly

younger brother, Geoffrey (also a longstanding member of the board) to succeed him in two years’ time when he plans

to retire. The Rosh family, who still own 40% of the shares, consider it their right to occupy the most senior positions

in the company so have never been very active in external recruitment. They only appointed Mary because they felt

they needed a qualified accountant on the board to deal with changes in international financial reporting standards.

Several former executive members have been recruited as non-executives immediately after they retired from full-time

service. A recent death, however, has reduced the number of non-executive directors to two. These sit alongside an

executive board of seven that, apart from Mary, have all been in post for over ten years.

Mary noted that board meetings very rarely contain any significant discussion of strategy and never involve any debate

or disagreement. When she asked why this was, she was told that the directors had all known each other for so long

that they knew how each other thought. All of the other directors came from similar backgrounds, she was told, and

had worked for the company for so long that they all knew what was ‘best’ for the company in any given situation.

Mary observed that notes on strategy were not presented at board meetings and she asked Timothy Rosh whether the

existing board was fully equipped to formulate strategy in the changing world of retailing. She did not receive a reply.

Required:

(a) Explain ‘agency’ in the context of corporate governance and criticise the governance arrangements of Rosh

and Company. (12 marks)

相似考题

更多“3 Mary Hobbes joined the board of Rosh and Company, a large retailer, as finance director earlier this year. Whilst shewas glad to have finally been given the chance to become finance director after several years as a financialaccountant, she also quickly”相关问题

-

第1题:

(b) Explain the roles of a nominations committee and assess the potential usefulness of a nominations committee

to the board of Rosh and Company. (8 marks)

正确答案:

(b) Nominations committees

General roles of a nominations committee.

It advises on the balance between executives and independent non-executive directors and establishes the appropriate

number and type of NEDs on the board. The nominations committee is usually made up of NEDs.

It establishes the skills, knowledge and experience possessed by current board and notes any gaps that will need to be filled.

It acts to meet the needs for continuity and succession planning, especially among the most senior members of the board.

It establishes the desirable and optimal size of the board, bearing in mind the current size and complexity of existing and

planned activities and strategies.

It seeks to ensure that the board is balanced in terms of it having board members from a diversity of backgrounds so as to

reflect its main constituencies and ensure a flow of new ideas and the scrutiny of existing strategies.

In the case of Rosh, the needs that a nominations committee could address are:

To recommend how many directors would be needed to run the business and plan for recruitment accordingly. The perceived

similarity of skills and interests of existing directors is also likely to be an issue.

To resolve the issues over numbers of NEDs. It seems likely that the current number is inadequate and would put Rosh in a

position of non-compliance with many of the corporate governance guidelines pertaining to NEDs.

To resolve the issues over the independence of NEDs. The closeness that the NEDs have to existing executive board members

potentially undermines their independence and a nominations committee should be able to identify this as an issue and make

recommendations to rectify it.

To make recommendations over the succession of the chairmanship. It may not be in the interests of Rosh for family members

to always occupy senior positions in the business. -

第2题:

(ii) State the taxation implications of both equity and loan finance from the point of view of a company.

(3 marks)

正确答案:

(ii) A company needs to be aware of the following issues:

Equity

(1) Costs incurred in issuing share capital are not allowed as a trading deduction.

(2) Distributions to investors are not allowed as a trading deduction.

(3) The cost of making distributions to shareholders are disallowable.

(4) Where profits are taxed at an effective rate of less than 19%, any profits used to make a distribution to noncorporate

shareholders will themselves be taxed at the full 19% rate.

Loan finance/debt

(1) The incidental costs of obtaining/raising loan finance are broadly deductible as a trading expense.

(2) Capital costs of raising loan finance (for example, loans issued at a discount) are not deductible for tax purposes.

(3) Interest incurred on a loan to finance a business is deductible from trading income. -

第3题:

TQ Company, a listed company, recently went into administration (it had become insolvent and was being managed by a firm of insolvency practitioners). A group of shareholders expressed the belief that it was the chairman, Miss Heike Hoiku, who was primarily to blame. Although the company’s management had made a number of strategic errors that brought about the company failure, the shareholders blamed the chairman for failing to hold senior management to account. In particular, they were angry that Miss Hoiku had not challenged chief executive Rupert Smith who was regarded by some as arrogant and domineering. Some said that Miss Hoiku was scared of Mr Smith.

Some shareholders wrote a letter to Miss Hoiku last year demanding that she hold Mr Smith to account for a number of previous strategic errors. They also asked her to explain why she had not warned of the strategic problems in her chairman’s statement in the annual report earlier in the year. In particular, they asked if she could remove Mr Smith from office for incompetence. Miss Hoiku replied saying that whilst she understood their concerns, it was difficult to remove a serving chief executive from office.

Some of the shareholders believed that Mr Smith may have performed better in his role had his reward package been better designed in the first place. There was previously a remuneration committee at TQ but when two of its four non-executive members left the company, they were not replaced and so the committee effectively collapsed.

Mr Smith was then able to propose his own remuneration package and Miss Hoiku did not feel able to refuse him.

He massively increased the proportion of the package that was basic salary and also awarded himself a new and much more expensive company car. Some shareholders regarded the car as ‘excessively’ expensive. In addition, suspecting that the company’s performance might deteriorate this year, he exercised all of his share options last year and immediately sold all of his shares in TQ Company.

It was noted that Mr Smith spent long periods of time travelling away on company business whilst less experienced directors struggled with implementing strategy at the company headquarters. This meant that operational procedures were often uncoordinated and this was one of the causes of the eventual strategic failure.

(a) Miss Hoiku stated that it was difficult to remove a serving chief executive from office.

Required:

(i) Explain the ways in which a company director can leave the service of a board. (4 marks)

(ii) Discuss Miss Hoiku’s statement that it is difficult to remove a serving chief executive from a board.

(4 marks)

(b) Assess, in the context of the case, the importance of the chairman’s statement to shareholders in TQ

Company’s annual report. (5 marks)

(c) Criticise the structure of the reward package that Mr Smith awarded himself. (4 marks)

(d) Criticise Miss Hoiku’s performance as chairman of TQ Company. (8 marks)

正确答案:(a) (i) Leaving the service of a board

Resignation with or without notice. Any director is free to withdraw his or her labour at any time but there is normally

a notice period required to facilitate an orderly transition from the outgoing chief executive to the incoming one.

Not offering himself/herself for re-election. Terms of office, which are typically three years, are renewable if the director

offers him or herself for re-election and the shareholders support the renewal. Retirement usually takes place at the end

of a three-year term when the director decides not to seek re-election.

Death in service when, obviously, the director is unable to either provide notice or seek retirement.

Failure of the company. When a company fails, all directors’ contracts are cancelled although this need not signal the

end of the directors’ involvement with company affairs as there may be ongoing legal issues to be resolved.

Being removed e.g. by being dismissed for disciplinary offences. It is relatively easy to ‘prove’ a disciplinary offence but

much more difficult to ‘prove’ incompetence. The nature of disciplinary offences are usually made clear in the terms and

conditions of employment and company policy.

Prolonged absence. Directors unable to perform. their duties owing to protracted absence, for any reason, may be

removed. The length of qualifying absence period varies by jurisdiction.

Being disqualified from being a company director by a court. Directors can be banned from holding directorships by a

court for a number of reasons including personal bankruptcy and other legal issues.

Failing to be re-elected if, having offered him or herself for re-election, shareholders elect not to re-appoint.

An ‘agreed departure’ such as by providing compensation to a director to leave.(ii) Discuss Miss Hoiku’s statement

The way that directors’ contracts and company law are written (in most countries) makes it difficult to remove a director

such as Mr Smith from office during an elected term of office so in that respect, Miss Hoiku is correct. Unless his contract

has highly specific performance targets built in to it, it is difficult to remove Mr Smith for incompetence in the

short-term as it is sometimes difficult to assess the success of strategies until some time has passed. If the alleged

incompetence is within Mr Smith’s term of office (typically three years) then it will usually be necessary to wait until the

director offers himself for re-election. The shareholders can then simply not re-elect the incompetent director (in this

case, Mr Smith). The most likely way to achieve the departure of Mr Smith within his term of office will be to ‘encourage’

him to resign by other directors failing to support him or by shareholders issuing a vote of no confidence at an AGM or

EGM. This would probably involve offering him a suitable financial package to depart at a time chosen by the other

members of the board or company shareholders.

(b) Importance of the chairman’s statement

The chairman’s statement (or president’s letter in some countries) is an important and usually voluntary item, typically carried

at the very beginning of an annual report. In general terms, it is intended to convey important messages to shareholders in

general, strategic terms. As a separate section from other narrative reporting sections of an annual report, it offers the

chairman the opportunity to inform. shareholders about issues that he or she feels it would be beneficial for them to be aware

of. This independent communication is an important part of the separation of the roles of CEO and chairman.

In the case of TQ Company, the role of the chairman is of particular importance because of the dominance of Mr Smith.

Miss Hoiku had a particular responsibility to use her most recent statement to inform. shareholders about going concern issues

notwithstanding the difficulties that might cause in her relationship with Mr Smith. Miss Hoiku has an ethical as well as an

agency responsibility to express her independence in the chairman’s statement and convey issues relevant to company value

to the company’s shareholders. She can use her chairman’s statement for this purpose.(c) Criticise the structure of the reward package that Mr Smith awarded himself

The balance between basic to performance related pay was very poor. Mr Smith, perhaps being aware that the prospect of

gaining much performance related income was low, took the opportunity to increase the fixed element of his income to

compensate. This was not only unprofessional and unethical on Mr Smith’s part, but it also represented very bad value for

shareholders. Having exercised his share options and sold the resulting shares, there was now no element of alignment of

his package with shareholder interests at all. His award to himself of an ‘excessively’ expensive company car was also not

in the shareholders’ interests. The fact that he exercised and sold all of his share options means that he will now have no

personal financial motivation to take strategic decisions intended to increase TQ Company’s share value. This represents a

poor degree of alignment between Mr Smith’s package and the interests of TQ’s shareholders.

(d) Criticise Miss Hoiku’s performance as chairman of TQ Company

The case describes a particularly poor performance by a company chairman. It is a key function of the chairman to represent

the shareholders’ interests in the company and Miss Hoiku has clearly failed in this duty.

A key reason for her poor performance was her reported inability or unwillingness to face up to Mr Smith who was clearly a

domineering personality. A key quality of a company chairman is his or her ability and willingness to personally challenge the

chief executive if necessary.

She failed to ensure that a committee structure was in place, allowing as she did, the remunerations committee to atrophy

when two members left the company.

Linked to this, it appears from the case that the two non-executive directors that left were not replaced and again, it is a part

of the chairman’s responsibility to ensure that an adequate number of non-executives are in place on the board.

She inexplicably allowed Mr Smith to design his own rewards package and presided over him reducing the performance

related element of his package which was clearly misaligned with the shareholders’ interests.

When Mr Smith failed to co-ordinate the other directors because of his unspecified business travel, she failed to hold him to

account thereby allowing the company’s strategy to fail.

There seems to have been some under-reporting of potential strategic problems in the most recent annual report. A ‘future

prospects’ or ‘continuing business’ statement is often a required disclosure in an annual report (in many countries) and there is evidence that this statement may have been missing or misleading in the most recent annual report. -

第4题:

The finance director of Blod Co, Uma Thorton, has requested that your firm type the financial statements in the form

to be presented to shareholders at the forthcoming company general meeting. Uma has also commented that the

previous auditors did not use a liability disclaimer in their audit report, and would like more information about the use

of liability disclaimer paragraphs.

Required:

(b) Discuss the ethical issues raised by the request for your firm to type the financial statements of Blod Co.

(3 marks)

正确答案:

(b) It is not uncommon for audit firms to word process and typeset the financial statements of their clients, especially where the

client is a relatively small entity, which may lack the resources and skills to perform. this task. It is not prohibited by ethical

standards.

However, there could be a perceived threat to independence, with risk magnified in the case of Blod Co, which is a listed

company. The auditors could be perceived to be involved with the preparation of the financial statements of a listed client

company, which is prohibited by ethical standards. IFAC’s Code of Ethics for Professional Accountants states that for a listed

client, the audit firm should not be involved with the preparation of financial statements, which would create a self-review

threat so severe that safeguards could not reduce the threat to an acceptable level. Although the typing of financial statements

itself is not prohibited by ethical guidance, the risk is that providing such a service could be perceived to be an element of

the preparation of the financial statements.

It is possible that during the process of typing the financial statements, decisions and judgments would be made. This could

be perceived as making management decisions in relation to the financial statements, a clear breach of independence.

Therefore to eliminate any risk exposure, the prudent decision would be not to type the financial statements, ensuring that

Blod Co appreciates the ethical problems that this would cause.

Tutorial note: This is an area not specifically covered by ethical guides, where different audit firms may have different views

on whether it is acceptable to provide a typing service for the financial statements of their clients. Credit will be awarded for

sensible discussion of the issues raised bearing in mind other options for the audit firm, for example, it could be argued that

it is acceptable to offer the typing service provided that it is performed by people independent of the audit team, and that

the matter has been discussed with the audit committee/those charged with governance -

第5题:

Mary is so happy today because she finally ________ the degree from Harvard after three years hard work.A. receives

B. steals

C. requires

D. finds

参考答案:A

-

第6题:

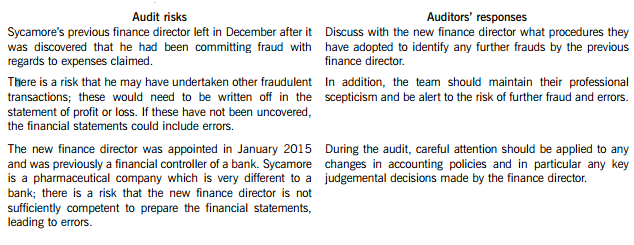

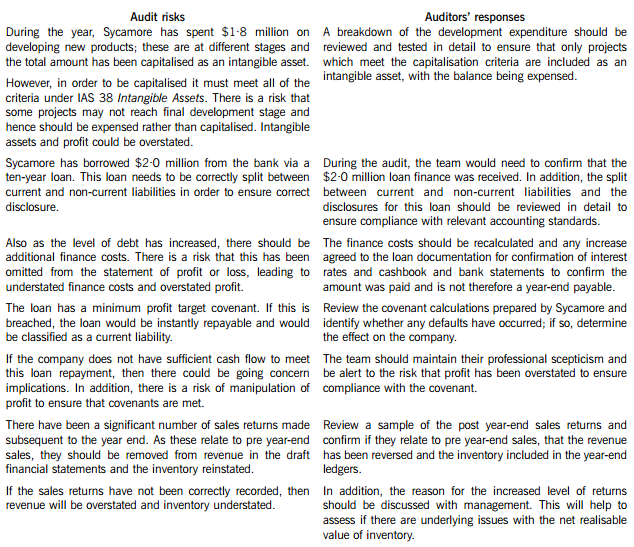

You are the audit supervisor of Maple & Co and are currently planning the audit of an existing client, Sycamore Science Co (Sycamore), whose year end was 30 April 2015. Sycamore is a pharmaceutical company, which manufactures and supplies a wide range of medical supplies. The draft financial statements show revenue of $35·6 million and profit before tax of $5·9 million.

Sycamore’s previous finance director left the company in December 2014 after it was discovered that he had been claiming fraudulent expenses from the company for a significant period of time. A new finance director was appointed in January 2015 who was previously a financial controller of a bank, and she has expressed surprise that Maple & Co had not uncovered the fraud during last year’s audit.

During the year Sycamore has spent $1·8 million on developing several new products. These projects are at different stages of development and the draft financial statements show the full amount of $1·8 million within intangible assets. In order to fund this development, $2·0 million was borrowed from the bank and is due for repayment over a ten-year period. The bank has attached minimum profit targets as part of the loan covenants.

The new finance director has informed the audit partner that since the year end there has been an increased number of sales returns and that in the month of May over $0·5 million of goods sold in April were returned.

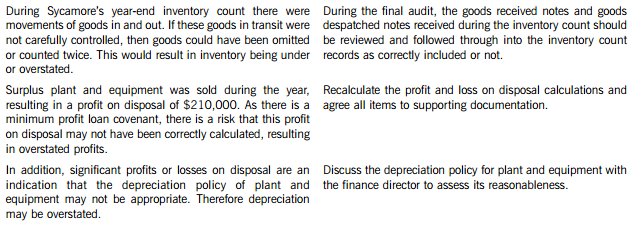

Maple & Co attended the year-end inventory count at Sycamore’s warehouse. The auditor present raised concerns that during the count there were movements of goods in and out the warehouse and this process did not seem well controlled.

During the year, a review of plant and equipment in the factory was undertaken and surplus plant was sold, resulting in a profit on disposal of $210,000.

Required:

(a) State Maples & Co’s responsibilities in relation to the prevention and detection of fraud and error. (4 marks)

(b) Describe SIX audit risks, and explain the auditor’s response to each risk, in planning the audit of Sycamore Science Co. (12 marks)

(c) Sycamore’s new finance director has read about review engagements and is interested in the possibility of Maple & Co undertaking these in the future. However, she is unsure how these engagements differ from an external audit and how much assurance would be gained from this type of engagement.

Required:

(i) Explain the purpose of review engagements and how these differ from external audits; and (2 marks)

(ii) Describe the level of assurance provided by external audits and review engagements. (2 marks)

正确答案:(a) Fraud responsibility

Maple & Co must conduct an audit in accordance with ISA 240 The Auditor’s Responsibilities Relating to Fraud in an Audit of Financial Statements and are responsible for obtaining reasonable assurance that the financial statements taken as a whole are free from material misstatement, whether caused by fraud or error.

In order to fulfil this responsibility, Maple & Co is required to identify and assess the risks of material misstatement of the financial statements due to fraud.

They need to obtain sufficient appropriate audit evidence regarding the assessed risks of material misstatement due to fraud, through designing and implementing appropriate responses. In addition, Maple & Co must respond appropriately to fraud or suspected fraud identified during the audit.

When obtaining reasonable assurance, Maple & Co is responsible for maintaining professional scepticism throughout the audit, considering the potential for management override of controls and recognising the fact that audit procedures which are effective in detecting error may not be effective in detecting fraud.

To ensure that the whole engagement team is aware of the risks and responsibilities for fraud and error, ISAs require that a discussion is held within the team. For members not present at the meeting, Sycamore’s audit engagement partner should determine which matters are to be communicated to them.

(b) Audit risks and auditors’ responses

(c) (i) Review engagements

Review engagements are often undertaken as an alternative to an audit, and involve a practitioner reviewing financial data, such as six-monthly figures. This would involve the practitioner undertaking procedures to state whether anything has come to their attention which causes the practitioner to believe that the financial data is not in accordance with the financial reporting framework.

A review engagement differs to an external audit in that the procedures undertaken are not nearly as comprehensive as those in an audit, with procedures such as analytical review and enquiry used extensively. In addition, the practitioner does not need to comply with ISAs as these only relate to external audits.

(ii) Levels of assurance

The level of assurance provided by audit and review engagements is as follows:

External audit – A high but not absolute level of assurance is provided, this is known as reasonable assurance. This provides comfort that the financial statements present fairly in all material respects (or are true and fair) and are free of material misstatements.

Review engagements – where an opinion is being provided, the practitioner gathers sufficient evidence to be satisfied that the subject matter is plausible; in this case negative assurance is given whereby the practitioner confirms that nothing has come to their attention which indicates that the subject matter contains material misstatements.

-

第7题:

The new colleague__________ to have worked in several big corporations before he joined our company.A.confesses

B.declares

C.claims

D.confirms答案:C解析:考查动词辨析。句意为“那位新同事( )他在进入我们公司之前在好几家大公司工作过”。claim意为“宣称,声称”,符合题意。confess意为“承认”,declare意为“宣布”.confirm意为“确认,证实”,均不符合题意。故选C。 -

第8题:

Text 1 Ruth Simmons joined Goldman Sachs's board as an outside director in January 2000;a year later she became president of Brown University.For the rest of the decade she apparently managed both roles without attracting much criticism.But by the end of 2009 Ms.Simmons was under fire for having sat on Goldman's compensation committee;how could she have let those enormous bonus payouts pass unremarked?By February the next year Ms.Simmons had left the board.The position was just taking up too much time,she said.Outside directors are supposed to serve as helpful,yet less biased,advisers on a firm's board.Having made their wealth and their reputations elsewhere,they presumably have enough independence to disagree with the chief executive's proposals.If the sky,and the share price,is falling,outside directors should be able to give advice based on having weathered their own crises.The researchers from Ohio University used a database that covered more than 10,000 firms and more than 64,000 different directors between 1989 and 2004.Then they simply checked which directors stayed from one proxy statement to the next.The most likely reason for departing a board was age,so the researchers concentrated on those“surprise”disappearances by directors under the age of 70.They found that after a surprise departure,the probability that the company will subsequently have to restate earnings increases by nearly 20%.The likelihood of being named in a federal classaction lawsuit also increases,and the stock is likely to perform worse.The effect tended to be larger for larger firms.Although a correlation between them leaving and subsequent bad performance at the firm is suggestive,it does not mean that such directors are always jumping off a sinking ship.Often they“trade up,”leaving riskier,smaller firms for larger and more stable firms.But the researchers believe that outside directors have an easier time of avoiding a blow to their reputations if they leave a firm before bad news break,even if a review of history shows they were on the board at the time any wrongdoing occurred.Firms who want to keep their outside directors through tough times may have to create incentives.Otherwise outside directors will follow the example of Ms.Simmons,once again very popular on campus.

According to the researchers from Ohio University,after an outside director's surprise departure,the firm is likely to_____A.become more stable

B.report increased earnings

C.do less well in the stock market

D.perform worse in lawsuits答案:C解析:细节题【命题思路】这是一道局部细节题,需要根据题干的关键信息对文章相关内容进行锁定,从而在准确定位之后得出答案。【直击答案】根据题干定位到第三段第四句和第五句,这两句列出了外部董事离开后可能出现的三种情况。其中“the stock is likely to perform worse”即为C项的意思,选项中的“do less well”等于原文中的“perform worse”,故C项正确。【干扰排除】从文中可知外部董事突然离开公司后,公司需要重申盈利的可能性增加了近20%,说明外部董事的离开会让公司境况变得不好,A项与原文信息完全相反,应排除。B项干扰来自文中“the probability…earnings increases…”分析句子主干“the probability increases by nearly 20%”可知不是earnings增加20%。D项干扰来自文中“The likelihood…also increases”。表现不佳是在“stock”中(the stock is likely to perform worse),选项把对“stock”的描述强加到“lawsuit”上,张冠李戴,故不选。 -

第9题:

He appreciated ______ the chance to deliver his thesis in the annual symposium on Comparative Literature.A.to have been given

B.to have given

C.having given

D.having been given答案:D解析:本题考察非谓语动词,题目意为“他对获得这次在比较文学年会上发表自己论点的机会表示感激。”appreciate后面必须接名词或动名词,本句题意要求使用被动语态,故选D。

-

第10题:

You are customizing the user interface options for the finance department in your organization. Users in the department are able to see a session counter on the Web interface of the Junos Pulse Access Control Service. The CFO is unable to see the session counter.Which explanation would cause this behavior?()

- A、The CFO is mapped to the finance role, but the session counter was enabled prior to the role mapping.

- B、The CFO is mapped to the finance role, but the session counter was enabled after the role mapping.

- C、The CFO is mapped to the executive and finance roles, but the CFO was mapped to the executive role first, which does not have the session counter enabled.

- D、The CFO is mapped to the executive and finance roles, but the CFO was mapped to the executive role last, which does not have the session counter enabled.

正确答案:C -

第11题:

单选题You are customizing the user interface options for the finance department in your organization. Users in the department are able to see a session counter on the Web interface of the Junos Pulse Access Control Service. The CFO is unable to see the session counter.Which explanation would cause this behavior?()AThe CFO is mapped to the finance role, but the session counter was enabled prior to the role mapping.

BThe CFO is mapped to the finance role, but the session counter was enabled after the role mapping.

CThe CFO is mapped to the executive and finance roles, but the CFO was mapped to the executive role first, which does not have the session counter enabled.

DThe CFO is mapped to the executive and finance roles, but the CFO was mapped to the executive role last, which does not have the session counter enabled.

正确答案: B解析: 暂无解析 -

第12题:

单选题MRK Consulting Ltd has been operating in the global market since 1988. We have successfully placed hundreds of IT & Banking professionals in leading companies in the Finance, Banking and IT industries.AMRK is a leading company in Finance and IT Industries.

BThere are many IT and Banking talents working with MRK.

CMRK has helped many people found good jobs.

正确答案: C解析:

公司的名称“MRK Consulting Ltd”表示“MRK咨询公司”,所以选项A可以被排除。根据原文第二句可知,MRK为成百上千的IT业和银行业的专业人士在一流的企业中找到了工作,而不是这些IT业和银行业的精英在MRK工作,所以选项B可以排除,C项正确。 -

第13题:

3 The Chemical Services Group plc (CSG), which operates a divisionalised structure, provides services to industrial and

domestic customers in Swingland, a country whose economic climate is subject to significant variations. There have

been a number of recent changes at board level within CSG and therefore the managing director called a meeting of

the board of directors at which each of four recently appointed directors put forward their view as to what their primary

focus should be. These were as follows:

The research and development director stated that ‘my primary focus is upon ensuring that we continue to develop

the products and services that satisfy the requirements of our existing and potential customers’.

The finance director stated that ‘my primary focus is upon keeping our investors satisfied’.

The human resources director stated that ‘my primary focus is upon ensuring that we take all the steps necessary to

establish and maintain our reputation as a responsible employer’.

The corporate affairs director stated that ‘my primary focus is upon the need to ensure that we are recognised as a

socially responsible organisation’.

Required:

(a) Discuss the criteria that should be considered in deciding upon suitable performance measures in respect of

the primary focus of each of the FOUR directors of CSG providing THREE appropriate quantitative measures

for each primary focus.

Note: your answer may include financial or non-financial quantitative measures. (12 marks)

正确答案:

(a) The primary focus of the research and development director

There is a need to measure the ability of CSG to offer up to date services that are sought after by existing and potential

customers. In this regard it would be relatively easy to determine the number of new products/services introduced in previous

periods. The performance of individual innovations should also be assessed. Also the aggregate expenditure on the

development of new services may indicate how CSG has performed with regard to offering up to date, customer focused

services.

The primary focus of the finance director

CSG could use return on capital employed (ROCE), economic value added (EVA) or residual income (RI) as measures of

financial performance. EVA and RI are both superior to return on capital employed (ROCE) in that each method is more likely

to develop goal congruence in terms of acquisition and disposal decisions. It is vital that any performance measure chosen

is consistent with the NPV rule. The use of RI could prove problematic when managers adopt a short term outlook and use

short term performance measures as decisions may not be consistent with the NPV rule. EVA attempts to avoid the problems

associated with understated asset values that arise in the use of ROCE and RI. Current values should be used as opposed to

historical costs.

The primary focus of the human resources director

CSG could use measures such as the rate of staff turnover, the level of absenteeism, training costs per employee and the

number of applications received for each job vacancy. These measures may provide an indication of the extent to which CSG

can be regarded as a socially responsible employer.

These measures should be compared with those of prior periods and targets. Employee attitude surveys may also be

undertaken on a systematic basis in order to assess matters such as the degree of satisfaction with the payment systems that

are in operation, management style. and working conditions.

The primary focus of the corporate affairs director

CSG could use measures such as the amounts spent on the disposal of waste chemicals, the number of complaints received

from clients and members of the public and the total of contributions made to organisations which seek to meet social

objectives, e.g. charities, schools and hospitals. -

第14题:

(ii) Audit work on after-date bank transactions identified a transfer of cash from Batik Co. The audit senior has

documented that the finance director explained that Batik commenced trading on 7 October 2005, after

being set up as a wholly-owned foreign subsidiary of Jinack. No other evidence has been obtained.

(4 marks)

Required:

Identify and comment on the implications of the above matters for the auditor’s report on the financial

statements of Jinack Co for the year ended 30 September 2005 and, where appropriate, the year ending

30 September 2006.

NOTE: The mark allocation is shown against each of the matters.

正确答案:

(ii) Wholly-owned foreign subsidiary

■ The cash transfer is a non-adjusting post balance sheet event. It indicates that Batik was trading after the balance

sheet date. However, that does not preclude Batik having commenced trading before the year end.

■ The finance director’s oral representation is wholly insufficient evidence with regard to the existence (or otherwise)

of Batik at 30 September 2005. If it existed at the balance sheet date its financial statements should have been

consolidated (unless immaterial).

■ The lack of evidence that might reasonably be expected to be available (e.g. legal papers, registration payments,

etc) suggests a limitation on the scope of the audit.

■ If such evidence has been sought but not obtained then the limitation is imposed by the entity (rather than by

circumstances).

■ Whilst the transaction itself may not be material, the information concerning the existence of Batik may be material

to users and should therefore be disclosed (as a non-adjusting event). The absence of such disclosure, if the

auditor considered necessary, would result in a qualified ‘except for’, opinion.

Tutorial note: Any matter that is considered sufficiently material to be worthy of disclosure as a non-adjusting

event must result in such a qualified opinion if the disclosure is not made.

■ If Batik existed at the balance sheet date and had material assets and liabilities then its non-consolidation would

have a pervasive effect. This would warrant an adverse opinion.

■ Also, the nature of the limitation (being imposed by the entity) could have a pervasive effect if the auditor is

suspicious that other audit evidence has been withheld. In this case the auditor should disclaim an opinion. -

第15题:

4 You are a senior manager in Becker & Co, a firm of Chartered Certified Accountants offering audit and assurance

services mainly to large, privately owned companies. The firm has suffered from increased competition, due to two

new firms of accountants setting up in the same town. Several audit clients have moved to the new firms, leading to

loss of revenue, and an over staffed audit department. Bob McEnroe, one of the partners of Becker & Co, has asked

you to consider how the firm could react to this situation. Several possibilities have been raised for your consideration:

1. Murray Co, a manufacturer of electronic equipment, is one of Becker & Co’s audit clients. You are aware that the

company has recently designed a new product, which market research indicates is likely to be very successful.

The development of the product has been a huge drain on cash resources. The managing director of Murray Co

has written to the audit engagement partner to see if Becker & Co would be interested in making an investment

in the new product. It has been suggested that Becker & Co could provide finance for the completion of the

development and the marketing of the product. The finance would be in the form. of convertible debentures.

Alternatively, a joint venture company in which control is shared between Murray Co and Becker & Co could be

established to manufacture, market and distribute the new product.

2. Becker & Co is considering expanding the provision of non-audit services. Ingrid Sharapova, a senior manager in

Becker & Co, has suggested that the firm could offer a recruitment advisory service to clients, specialising in the

recruitment of finance professionals. Becker & Co would charge a fee for this service based on the salary of the

employee recruited. Ingrid Sharapova worked as a recruitment consultant for a year before deciding to train as

an accountant.

3. Several audit clients are experiencing staff shortages, and it has been suggested that temporary staff assignments

could be offered. It is envisaged that a number of audit managers or seniors could be seconded to clients for

periods not exceeding six months, after which time they would return to Becker & Co.

Required:

Identify and explain the ethical and practice management implications in respect of:

(a) A business arrangement with Murray Co. (7 marks)

正确答案:

4 Becker & Co

(a) Joint business arrangement

The business opportunity in respect of Murray Co could be lucrative if the market research is to be believed.

However, IFAC’s Code of Ethics for Professional Accountants states that a mutual business arrangement is likely to give rise

to self-interest and intimidation threats to independence and objectivity. The audit firm must be and be seen to be independent

of the audit client, which clearly cannot be the case if the audit firm and the client are seen to be working together for a

mutual financial gain.

In the scenario, two options are available. Firstly, Becker & Co could provide the audit client with finance to complete the

development and take the product to market. There is a general prohibition on audit firms providing finance to their audit

clients. This would create a clear financial self-interest threat as the audit firm would be receiving a return on investment from

their client. The Code states that if a firm makes a loan (or guarantees a loan) to a client, the self-interest threat created would

be so significant that no safeguard could reduce the threat to an acceptable level.

The provision of finance using convertible debentures raises a further ethical problem, because if the debentures are ultimately

converted to equity, the audit firm would then hold equity shares in their audit client. This is a severe financial self-interest,

which safeguards are unlikely to be able to reduce to an acceptable level.

The finance should not be advanced to Murray Co while the company remains an audit client of Becker & Co.

The second option is for a joint venture company to be established. This would be perceived as a significant mutual business

interest as Becker & Co and Murray Co would be investing together, sharing control and sharing a return on investment in

the form. of dividends. IFAC’s Code of Ethics states that unless the relationship between the two parties is clearly insignificant,

the financial interest is immaterial, and the audit firm is unable to exercise significant influence, then no safeguards could

reduce the threat to an acceptable level. In this case Becker & Co may not enter into the joint venture arrangement while

Murray Co is still an audit client.

The audit practice may consider that investing in the new electronic product is a commercial strategy that it wishes to pursue,

either through loan finance or using a joint venture arrangement. In this case the firm should resign as auditor with immediate

effect in order to eliminate any ethical problem with the business arrangement. The partners should carefully consider if the

potential return on investment will more than compensate for the lost audit fee from Murray Co.

The partners should also reflect on whether they want to diversify to such an extent – this investment is unlikely to be in an

area where any of the audit partners have much knowledge or expertise. A thorough commercial evaluation and business risk

analysis must be performed on the new product to ensure that it is a sound business decision for the firm to invest.

The audit partners should also consider how much time they would need to spend on this business development, if they

decided to resign as auditors and to go ahead with the investment. Such a new and important project could mean that they

take their focus off the key business i.e. the audit practice. They should consider if it would be better to spend their time trying

to compete effectively with the two new firms of accountants, trying to retain key clients, and to attract new accounting and

audit clients rather than diversify into something completely different. -

第16题:

--Do you know Mary very well?--Yes, she and I _______ friends since we met in university 20 years ago.A.have become

B.have turned

C.have made

D.have been

参考答案:D

-

第17题:

One of your audit clients is Tye Co a company providing petrol, aviation fuel and similar oil based products to the government of the country it is based in. Although the company is not listed on any stock exchange, it does follow best practice regarding corporate governance regulations. The audit work for this year is complete, apart from the matter referred to below.

As part of Tye Co’s service contract with the government, it is required to hold an emergency inventory reserve of 6,000 barrels of aviation fuel. The inventory is to be used if the supply of aviation fuel is interrupted due to unforeseen events such as natural disaster or terrorist activity.

This fuel has in the past been valued at its cost price of $15 a barrel. The current value of aviation fuel is $120 a barrel. Although the audit work is complete, as noted above, the directors of Tye Co have now decided to show the ‘real’ value of this closing inventory in the financial statements by valuing closing inventory of fuel at market value, which does not comply with relevant accounting standards. The draft financial statements of Tye Co currently show a profit of approximately $500,000 with net assets of $170 million.

Required:

(a) List the audit procedures and actions that you should now take in respect of the above matter. (6 marks)

(b) For the purposes of this section assume from part (a) that the directors have agreed to value inventory at

$15/barrel.

Having investigated the matter in part (a) above, the directors present you with an amended set of financial

statements showing the emergency reserve stated not at 6,000 barrels, but reported as 60,000 barrels. The final financial statements now show a profit following the inclusion of another 54,000 barrels of oil in inventory. When queried about the change from 6,000 to 60,000 barrels of inventory, the finance director stated that this change was made to meet expected amendments to emergency reserve requirements to be published in about six months time. The inventory will be purchased this year, and no liability will be shown in the financial statements for this future purchase. The finance director also pointed out that part of Tye Co’s contract with the government requires Tye Co to disclose an annual profit and that a review of bank loans is due in three months. Finally the finance director stated that if your audit firm qualifies the financial statements in respect of the increase in inventory, they will not be recommended for re-appointment at the annual general meeting. The finance director refuses to amend the financial statements to remove this ‘fictitious’ inventory.

Required:

(i) State the external auditor’s responsibilities regarding the detection of fraud; (4 marks)

(ii) Discuss to which groups the auditors of Tye Co could report the ‘fictitious’ aviation fuel inventory;

(6 marks)

(iii) Discuss the safeguards that the auditors of Tye Co can use in an attempt to overcome the intimidation

threat from the directors of Tye Co. (4 marks)

正确答案:

(a)Valuationofaviationinventory–ReviewGAAPtoensurethattherearenoexceptionsforaviationfuelorinventoryheldforemergencypurposeswhichwouldsuggestamarketvaluationshouldbeused.–Calculatethedifferenceinvaluation.Theerrorininventoryvaluationis$105*6,000barrelsor$630k,whichisamaterialamountcomparedtoprofit.–Reviewprioryearworkingpaperstodeterminewhetherasimilarsituationoccurredlastyearandascertaintheoutcomeatthatstage.–Discussthematterwiththedirectorstoobtainreasonswhytheybelievethatmarketvalueshouldbeusedfortheinventorythisyear.–Warnthedirectorsthatinyouropinion,aviationfuelshouldbevaluedatthelowerofcostornetrealisablevalue(thatis$15/barrel)andthatusingmarketvaluewillresultinamodificationtotheauditreport.–Ifthedirectorsnowamendthefinancialstatementstoshowinventoryvaluedatcost,thenconsidermentioningtheissueintheweaknessletteranddonotmodifytheauditreportinrespectofthismatter.–Ifthedirectorswillnotamendthefinancialstatements,quantifytheeffectofthedisagreementinthevaluationmethod–thesumof$630,000ismaterialtothefinancialstatementsasTyeCo’sincomestatementfigureisdecreasedfromasmalllosstoalossof$130,000althoughnetassetsdecreasebyonlyabout0·3%.–ObtainamanagementrepresentationletterfromthedirectorsofTyeCoconfirmingthatmarketvalueistobeusedfortheemergencyinventoryofaviationfuel.–Ifthedirectorswillnotamendthefinancialstatements,drafttherelevantsectionsoftheauditreport,showingaqualificationonthegroundsofdisagreementwiththeaccountingpolicyforvaluationofinventory.(b)(i)ExternalauditorresponsibilitiesregardingdetectionoffraudOverallresponsibilityofauditorTheexternalauditorisprimarilyresponsiblefortheauditopiniononthefinancialstatementsfollowingtheinternationalauditingstandards(ISAs).ISA240(Redrafted)TheAuditor’sResponsibilitiesRelatingtoFraudinanAuditofFinancialStatementsisrelevanttoauditworkregardingfraud.Themainfocusofauditworkisthereforetoensurethatthefinancialstatementsshowatrueandfairview.Thedetectionoffraudisthereforenotthemainfocusoftheexternalauditor’swork.Anauditorisresponsibleforobtainingreasonableassurancethatthefinancialstatementsasawholearefreefrommaterialmisstatement,whethercausedbyfraudorerror.Theauditorisresponsibleformaintaininganattitudeofprofessionalscepticismthroughouttheaudit,consideringthepotentialformanagementoverrideofcontrolsandrecognisingthefactthatauditproceduresthatareeffectivefordetectingerrormaynotbeeffectivefordetectingfraud.MaterialityISA240statesthattheauditorshouldreduceauditrisktoanacceptablylowlevel.Therefore,inreachingtheauditopinionandperformingauditwork,theexternalauditortakesintoaccounttheconceptofmateriality.Inotherwords,theexternalauditorisnotresponsibleforcheckingallthetransactions.Auditproceduresareplannedtohaveareasonablelikelihoodofidentifyingmaterialfraud.DiscussionamongtheauditteamAdiscussionisrequiredamongtheengagementteamplacingparticularemphasisonhowandwheretheentity’sfinancialstatementsmaybesusceptibletomaterialmisstatementduetofaud,includinghowfraudmightoccur.IdentificationoffraudInsituationswheretheexternalauditordoesdetectfraud,thentheauditorwillneedtoconsidertheimplicationsfortheentireaudit.Inotherwords,theexternalauditorhasaresponsibilitytoextendtestingintootherareasbecausetheriskofprovidinganincorrectauditopinionwillhaveincreased.(ii)GroupstoreportfraudtoReporttoauditcommitteeDisclosethesituationtotheauditcommitteeastheyarechargedwithmaintainingahighstandardofgovernanceinthecompany.Thecommitteeshouldbeabletodiscussthesituationwiththedirectorsandrecommendthattheytakeappropriateactione.g.amendthefinancialstatements.ReporttogovernmentAsTyeCoisactingunderagovernmentcontract,andtheover-statementofinventorywillmeanTyeCobreachesthatcontract(thereportedprofitbecomingaloss),thentheauditormayhavetoreportthesituationdirectlytothegovernment.TheauditorofTyeConeedstoreviewthecontracttoconfirmthereportingrequiredunderthatcontract.ReporttomembersIfthefinancialstatementsdonotshowatrueandfairviewthentheauditorneedstoreportthisfacttothemembersofTyeCo.Theauditreportwillbequalifiedwithanexceptfororadverseopinion(dependingonmateriality)andinformationconcerningthereasonforthedisagreementgiven.Inthiscasetheauditorislikelytostatefactuallytheproblemofinventoryquantitiesbeingincorrect,ratherthanstatingorimplyingthatthedirectorsareinvolvedinfraud.ReporttoprofessionalbodyIftheauditorisuncertainastothecorrectcourseofaction,advicemaybeobtainedfromtheauditor’sprofessionalbody.Dependingontheadvicereceived,theauditormaysimplyreporttothemembersintheauditreport,althoughresignationandtheconveningofageneralmeetingisanotherreportingoption.(iii)Intimidationthreat–safeguardsInresponsetotheimpliedthreatofdismissaliftheauditreportismodifiedregardingthepotentialfraud/error,thefollowingsafeguardsareavailabletotheauditor.DiscusswithauditcommitteeThesituationcanbediscussedwiththeauditcommittee.Astheauditcommitteeshouldcomprisenon-executivedirectors,theywillbeabletodiscussthesituationwiththefinancedirectorandpointoutclearlytheauditor’sopinion.Theycanalsoremindthedirectorsasawholethattheappointmentoftheauditorrestswiththemembersontherecommendationoftheauditcommittee.Iftherecommendationoftheauditcommitteeisrejectedbytheboard,goodcorporategovernancerequiresdisclosureofthereasonforrejection.ObtainsecondpartnerreviewTheengagementpartnercanaskasecondpartnertoreviewtheworkingpapersandotherevidencerelatingtotheissueofpossiblefraud.Whilethisactiondoesnotresolvetheissue,itdoesprovideadditionalassurancethatthefindingsandactionsoftheengagementpartnerarevalid.ResignationIfthematterisserious,thentheauditorcanconsiderresignationratherthannotbeingre-appointed.Resignationhastheadditionalsafeguardthattheauditorcannormallyrequirethedirectorstoconveneageneralmeetingtoconsiderthecircumstancesoftheresignation. -

第18题:

Moonstar Co is a property development company which is planning to undertake a $200 million commercial property development. Moonstar Co has had some difficulties over the last few years, with some developments not generating the expected returns and the company has at times struggled to pay its finance costs. As a result Moonstar Co’s credit rating has been lowered, affecting the terms it can obtain for bank finance. Although Moonstar Co is listed on its local stock exchange, 75% of the share capital is held by members of the family who founded the company. The family members who are shareholders do not wish to subscribe for a rights issue and are unwilling to dilute their control over the company by authorising a new issue of equity shares. Moonstar Co’s board is therefore considering other methods of financing the development, which the directors believe will generate higher returns than other recent investments, as the country where Moonstar Co is based appears to be emerging from recession.

Securitisation proposals

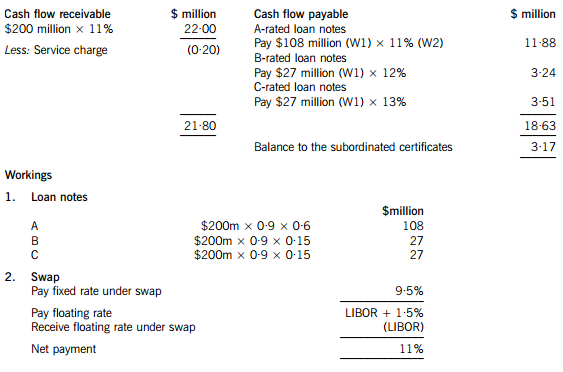

One of the non-executive directors of Moonstar Co has proposed that it should raise funds by means of a securitisation process, transferring the rights to the rental income from the commercial property development to a special purpose vehicle. Her proposals assume that the leases will generate an income of 11% per annum to Moonstar Co over a ten-year period. She proposes that Moonstar Co should use 90% of the value of the investment for a collateralised loan obligation which should be structured as follows:

– 60% of the collateral value to support a tranche of A-rated floating rate loan notes offering investors LIBOR plus 150 basis points

– 15% of the collateral value to support a tranche of B-rated fixed rate loan notes offering investors 12%

– 15% of the collateral value to support a tranche of C-rated fixed rate loan notes offering investors 13%

– 10% of the collateral value to support a tranche as subordinated certificates, with the return being the excess of receipts over payments from the securitisation process

The non-executive director believes that there will be sufficient demand for all tranches of the loan notes from investors. Investors will expect that the income stream from the development to be low risk, as they will expect the property market to improve with the recession coming to an end and enough potential lessees to be attracted by the new development.

The non-executive director predicts that there would be annual costs of $200,000 in administering the loan. She acknowledges that there would be interest rate risks associated with the proposal, and proposes a fixed for variable interest rate swap on the A-rated floating rate notes, exchanging LIBOR for 9·5%.

However the finance director believes that the prediction of the income from the development that the non-executive director has made is over-optimistic. He believes that it is most likely that the total value of the rental income will be 5% lower than the non-executive director has forecast. He believes that there is some risk that the returns could be so low as to jeopardise the income for the C-rated fixed rate loan note holders.

Islamic finance

Moonstar Co’s chief executive has wondered whether Sukuk finance would be a better way of funding the development than the securitisation.

Moonstar Co’s chairman has pointed out that a major bank in the country where Moonstar Co is located has begun to offer a range of Islamic financial products. The chairman has suggested that a Mudaraba contract would be the most appropriate method of providing the funds required for the investment.

Required:

(a) Calculate the amounts in $ which each of the tranches can expect to receive from the securitisation arrangement proposed by the non-executive director and discuss how the variability in rental income affects the returns from the securitisation. (11 marks)

(b) Discuss the benefits and risks for Moonstar Co associated with the securitisation arrangement that the non-executive director has proposed. (6 marks)

(c) (i) Discuss the suitability of Sukuk finance to fund the investment, including an assessment of its appeal to potential investors. (4 marks)

(ii) Discuss whether a Mudaraba contract would be an appropriate method of financing the investment and discuss why the bank may have concerns about providing finance by this method. (4 marks)

正确答案:(a) An annual cash flow account compares the estimated cash flows receivable from the property against the liabilities within the securitisation process. The swap introduces leverage into the arrangement.

The holders of the certificates are expected to receive $3·17million on $18 million, giving them a return of 17·6%. If the cash flows are 5% lower than the non-executive director has predicted, annual revenue received will fall to $20·90 million, reducing the balance available for the subordinated certificates to $2·07 million, giving a return of 11·5% on the subordinated certificates, which is below the returns offered on the B and C-rated loan notes. The point at which the holders of the certificates will receive nothing and below which the holders of the C-rated loan notes will not receive their full income will be an annual income of $18·83 million (a return of 9·4%), which is 14·4% less than the income that the non-executive director has forecast.

(b) Benefits

The finance costs of the securitisation may be lower than the finance costs of ordinary loan capital. The cash flows from the commercial property development may be regarded as lower risk than Moonstar Co’s other revenue streams. This will impact upon the rates that Moonstar Co is able to offer borrowers.

The securitisation matches the assets of the future cash flows to the liabilities to loan note holders. The non-executive director is assuming a steady stream of lease income over the next 10 years, with the development probably being close to being fully occupied over that period.

The securitisation means that Moonstar Co is no longer concerned with the risk that the level of earnings from the properties will be insufficient to pay the finance costs. Risks have effectively been transferred to the loan note holders.

Risks

Not all of the tranches may appeal to investors. The risk-return relationship on the subordinated certificates does not look very appealing, with the return quite likely to be below what is received on the C-rated loan notes. Even the C-rated loan note holders may question the relationship between the risk and return if there is continued uncertainty in the property sector.

If Moonstar Co seeks funding from other sources for other developments, transferring out a lower risk income stream means that the residual risks associated with the rest of Moonstar Co’s portfolio will be higher. This may affect the availability and terms of other borrowing.

It appears that the size of the securitisation should be large enough for the costs to be bearable. However Moonstar Co may face unforeseen costs, possibly unexpected management or legal expenses.

(c) (i) Sukuk finance could be appropriate for the securitisation of the leasing portfolio. An asset-backed Sukuk would be the same kind of arrangement as the securitisation, where assets are transferred to a special purpose vehicle and the returns and repayments are directly financed by the income from the assets. The Sukuk holders would bear the risks and returns of the relationship.

The other type of Sukuk would be more like a sale and leaseback of the development. Here the Sukuk holders would be guaranteed a rental, so it would seem less appropriate for Moonstar Co if there is significant uncertainty about the returns from the development.

The main issue with the asset-backed Sukuk finance is whether it would be as appealing as certainly the A-tranche of the securitisation arrangement which the non-executive director has proposed. The safer income that the securitisation offers A-tranche investors may be more appealing to investors than a marginally better return from the Sukuk. There will also be costs involved in establishing and gaining approval for the Sukuk, although these costs may be less than for the securitisation arrangement described above.

(ii) A Mudaraba contract would involve the bank providing capital for Moonstar Co to invest in the development. Moonstar Co would manage the investment which the capital funded. Profits from the investment would be shared with the bank, but losses would be solely borne by the bank. A Mudaraba contract is essentially an equity partnership, so Moonstar Co might not face the threat to its credit rating which it would if it obtained ordinary loan finance for the development. A Mudaraba contract would also represent a diversification of sources of finance. It would not require the commitment to pay interest that loan finance would involve.

Moonstar Co would maintain control over the running of the project. A Mudaraba contract would offer a method of obtaining equity funding without the dilution of control which an issue of shares to external shareholders would bring. This is likely to make it appealing to Moonstar Co’s directors, given their desire to maintain a dominant influence over the business.

The bank would be concerned about the uncertainties regarding the rental income from the development. Although the lack of involvement by the bank might appeal to Moonstar Co's directors, the bank might not find it so attractive. The bank might be concerned about information asymmetry – that Moonstar Co’s management might be reluctant to supply the bank with the information it needs to judge how well its investment is performing.

-

第19题:

After working for the firm for ten years, he finally_______the rank of deputy director.A.achieved

B.approached

C.attained

D.acquired答案:C解析:考查动词辨析。achieve“成就”,approach“接近”,attain“(通常指经过努力)获得,达到”,acquire“学到,取到”。句意为“在这个公司工作了十年之后,他终于了部门主管的职位”,可知应是获得主管的职位。故选C。 -

第20题:

Next Monday is Tina’s anniversary of the entry to Apple Inc. She ____by the company for 15 whole years by then.A.will have been employed

B.will have employed

C.has been employed

D.will employed答案:A解析:本题考察动词的时态和语态。题目意为“下周一是蒂娜任职苹果公司的周年纪念日,到那时她就为公司工作15个年头了。时间状语next Monday, for 15 whole years;因此应该为将来完成时。蒂娜是被雇佣的关系,所以是被动语态,be employed by。

-

第21题:

A customer is creating an Event Action Plan to monitor CPU utilization on their SQL server. While creating a Simple Event Filter, the event type "Director.Director Agent.CPU Monitors" option is not available. Which of the following is the most likely source of the problem?()

- A、The appropriate Hardware Status monitors have not been set.

- B、The appropriate Resource Monitor thresholds have not been set.

- C、The appropriate Windows Performance monitors have not been set.

- D、The appropriate Process Management thresholds have not been set.

正确答案:B -

第22题:

You are designing a group management strategy for users in the finance department. You need to identify the appropriate changes that need to be made to the current group management strategy. You want to accomplish this goal by using the minimum number of groups. What should you do?()

- A、 Add the finance users to the financeData group to which the necessary permissions have been assigned.

- B、 Add the finance users to the financeGG group to which the necessary permissions have been assigned.

- C、 Add the finance users to the financeGG group. Then add the financeGG group to the financeData group to which the necessary permissions have been assigned.

- D、 Add the finance users to the financeGG group. Add the financeGG group to the financeUG group to the financeDat group to which the necessary permissions have been assigned.

正确答案:B -

第23题:

单选题A customer is creating an Event Action Plan to monitor CPU utilization on their SQL server. While creating a Simple Event Filter, the event type "Director.Director Agent.CPU Monitors" option is not available. Which of the following is the most likely source of the problem?()AThe appropriate Hardware Status monitors have not been set.

BThe appropriate Resource Monitor thresholds have not been set.

CThe appropriate Windows Performance monitors have not been set.

DThe appropriate Process Management thresholds have not been set.

正确答案: B解析: 暂无解析