Moonstar Co is a property development company which is planning to undertake a $200 million commercial property development. Moonstar Co has had some difficulties over the last few years, with some developments not generating the expected returns and the

题目

Moonstar Co is a property development company which is planning to undertake a $200 million commercial property development. Moonstar Co has had some difficulties over the last few years, with some developments not generating the expected returns and the company has at times struggled to pay its finance costs. As a result Moonstar Co’s credit rating has been lowered, affecting the terms it can obtain for bank finance. Although Moonstar Co is listed on its local stock exchange, 75% of the share capital is held by members of the family who founded the company. The family members who are shareholders do not wish to subscribe for a rights issue and are unwilling to dilute their control over the company by authorising a new issue of equity shares. Moonstar Co’s board is therefore considering other methods of financing the development, which the directors believe will generate higher returns than other recent investments, as the country where Moonstar Co is based appears to be emerging from recession.

Securitisation proposals

One of the non-executive directors of Moonstar Co has proposed that it should raise funds by means of a securitisation process, transferring the rights to the rental income from the commercial property development to a special purpose vehicle. Her proposals assume that the leases will generate an income of 11% per annum to Moonstar Co over a ten-year period. She proposes that Moonstar Co should use 90% of the value of the investment for a collateralised loan obligation which should be structured as follows:

– 60% of the collateral value to support a tranche of A-rated floating rate loan notes offering investors LIBOR plus 150 basis points

– 15% of the collateral value to support a tranche of B-rated fixed rate loan notes offering investors 12%

– 15% of the collateral value to support a tranche of C-rated fixed rate loan notes offering investors 13%

– 10% of the collateral value to support a tranche as subordinated certificates, with the return being the excess of receipts over payments from the securitisation process

The non-executive director believes that there will be sufficient demand for all tranches of the loan notes from investors. Investors will expect that the income stream from the development to be low risk, as they will expect the property market to improve with the recession coming to an end and enough potential lessees to be attracted by the new development.

The non-executive director predicts that there would be annual costs of $200,000 in administering the loan. She acknowledges that there would be interest rate risks associated with the proposal, and proposes a fixed for variable interest rate swap on the A-rated floating rate notes, exchanging LIBOR for 9·5%.

However the finance director believes that the prediction of the income from the development that the non-executive director has made is over-optimistic. He believes that it is most likely that the total value of the rental income will be 5% lower than the non-executive director has forecast. He believes that there is some risk that the returns could be so low as to jeopardise the income for the C-rated fixed rate loan note holders.

Islamic finance

Moonstar Co’s chief executive has wondered whether Sukuk finance would be a better way of funding the development than the securitisation.

Moonstar Co’s chairman has pointed out that a major bank in the country where Moonstar Co is located has begun to offer a range of Islamic financial products. The chairman has suggested that a Mudaraba contract would be the most appropriate method of providing the funds required for the investment.

Required:

(a) Calculate the amounts in $ which each of the tranches can expect to receive from the securitisation arrangement proposed by the non-executive director and discuss how the variability in rental income affects the returns from the securitisation. (11 marks)

(b) Discuss the benefits and risks for Moonstar Co associated with the securitisation arrangement that the non-executive director has proposed. (6 marks)

(c) (i) Discuss the suitability of Sukuk finance to fund the investment, including an assessment of its appeal to potential investors. (4 marks)

(ii) Discuss whether a Mudaraba contract would be an appropriate method of financing the investment and discuss why the bank may have concerns about providing finance by this method. (4 marks)

相似考题

更多“Moonstar Co is a property development company which is planning to undertake a $200 million commercial property development. Moonstar Co has had some difficulties over the last few years, with some developments not generating the expected returns and the ”相关问题

-

第1题:

6 Alasdair, aged 42, is single. He is considering investing in property, as he has heard that this represents a good

investment. In order to raise the funds to buy the property, he wants to extract cash from his personal company, Beezer

Limited, whose year end is 31 December.

Beezer Limited was formed on 1 May 1998 with £1,000 of capital issued as 1,000 £1 ordinary shares, and traded

until 1 January 2005 when Alasdair sold the trade and related assets. The company’s only asset is cash of

£120,000. Alasdair wants to extract this cash from the company with the minimum amount of tax payable. He is

considering either, paying himself a dividend of £120,000, on 31 March 2006, after which the company would have

no assets and be wound up or, leaving the cash in the company and then liquidating the company. Costs of liquidation

of £5,000 would then be incurred.

Since Beezer Limited ceased trading, Alasdair has been taken on as a partner at a marketing firm, Gallus & Co. He

estimates his profit share for the year of assessment 2005/06 will be £30,000. He has not made any capital disposals

in the current tax year.

Alasdair wishes to reinvest the cash extracted from Beezer Limited in property but is not sure whether he should invest

directly in residential or commercial property, or do so via some form. of collective investment. He is aware that Gallus

& Co are looking to rent a new warehouse which could be bought for £200,000. Alasdair thinks that he may be able

to buy the warehouse himself and lease it to his firm, but only if he can borrow the additional money to buy the

property.

Alasdair has a 25% shareholding in another company, Glaikit Limited, whose year end is 31 March. The remaining

shares in this company are held by his friend, Gill. Alasdair is considering borrowing £15,000 from Glaikit Limited

on 1 January 2006. He does not intend to pay any interest on the loan, which is likely to be written off some time

in 2007. Alasdair does not have any connection with Glaikit Limited other than his shareholding.

Required:

(a) Advise Alasdair whether or not a dividend payment will result in a higher after-tax cash sum than the

liquidation of Beezer Limited. Assume that either the dividend would be paid on 31 March 2006 or the

liquidation would take place on 31 March 2006. (9 marks)

Assume that Beezer Limited has always paid corporation tax at or above the small companies rate of 19%

and that the tax rates and allowances for 2004/05 apply throughout this part.

正确答案:

-

第2题:

(b) Historically, all owned premises have been measured at cost depreciated over 10 to 50 years. The management

board has decided to revalue these premises for the year ended 30 September 2005. At the balance sheet date

two properties had been revalued by a total of $1·7 million. Another 15 properties have since been revalued by

$5·4 million and there remain a further three properties which are expected to be revalued during 2006. A

revaluation surplus of $7·1 million has been credited to equity. (7 marks)

Required:

For each of the above issues:

(i) comment on the matters that you should consider; and

(ii) state the audit evidence that you should expect to find,

in undertaking your review of the audit working papers and financial statements of Albreda Co for the year ended

30 September 2005.

NOTE: The mark allocation is shown against each of the three issues.

正确答案:

(b) Revaluation of owned premises

(i) Matters

■ The revaluations are clearly material as $1·7 million, $5·4 million and $7·1 million represent 5·5% , 17·6% and

23·1% of total assets, respectively.

■ The change in accounting policy, from a cost model to a revaluation model, should be accounted for in accordance

with IAS 16 ‘Property, Plant and Equipment’ (i.e. as a revaluation).

Tutorial note: IAS 8 ‘Accounting Policies, Changes in Accounting Estimates and Errors’ does not apply to the initial

application of a policy to revalue assets in accordance with IAS 16.

■ The basis on which the valuations have been carried out, for example, market-based fair value (IAS 16).

■ Independence, qualifications and expertise of valuer(s).

■ IAS 16 does not permit the selective revaluation of assets thus the whole class of premises should have been

revalued.

■ The valuations of properties after the year end are adjusting events (i.e. providing additional evidence of conditions

existing at the year end) per IAS 10 ‘Events After the Balance Sheet Date’.

Tutorial note: It is ‘now’ still less than three months after the year end so these valuations can reasonably be

expected to reflect year-end values.

■ If $5·4 million is a net amount of surpluses and deficits it should be grossed up so that the credit to equity reflects

the sum of the surpluses with any deficits being expensed through profit and loss (IAS 36 ‘Impairment of Assets’).

■ The revaluation exercise is incomplete. If the revaluations on the remaining three properties are expected to be

material and cannot be reasonably estimated for inclusion in the financial statements for the year ended

30 September 2005 perhaps the change in policy should be deferred for a year.

■ Depreciation for the year should have been calculated on cost as usual to establish carrying amount before

revaluation.

■ Any premises held under finance leases should be similarly revalued.

(ii) Audit evidence

■ A schedule of depreciated cost of owned premises extracted from the non-current asset register.

■ Calculation of difference between valuation and depreciated cost by property. Separate summation of surpluses

and deficits.

■ Copy of valuation certificate for each property.

■ Physical inspection of properties with largest surpluses (including the two valued before the year end) to confirm

condition.

■ Extracts from local property guides/magazines indicating a range of values of similarly styled/sized properties.

■ Separate presentation of the revaluation surpluses (gross) in:

– the statement of changes in equity; and

– reconciliation of carrying amount at the beginning and end of the period.

■ IAS 16 disclosures in the notes to the financial statements including:

– the effective date of revaluation;

– whether an independent valuer was involved;

– the methods and significant assumptions applied in estimating fair values; and

– the carrying amount that would have been recognised under the cost model. -

第3题:

5 You are the manager responsible for the audit of Blod Co, a listed company, for the year ended 31 March 2008. Your

firm was appointed as auditors of Blod Co in September 2007. The audit work has been completed, and you are

reviewing the working papers in order to draft a report to those charged with governance. The statement of financial

position (balance sheet) shows total assets of $78 million (2007 – $66 million). The main business activity of Blod

Co is the manufacture of farm machinery.

During the audit of property, plant and equipment it was discovered that controls over capital expenditure transactions

had deteriorated during the year. Authorisation had not been gained for the purchase of office equipment with a cost

of $225,000. No material errors in the financial statements were revealed by audit procedures performed on property,

plant and equipment.

An internally generated brand name has been included in the statement of financial position (balance sheet) at a fair

value of $10 million. Audit working papers show that the matter was discussed with the financial controller, who

stated that the $10 million represents the present value of future cash flows estimated to be generated by the brand

name. The member of the audit team who completed the work programme on intangible assets has noted that this

treatment appears to be in breach of IAS 38 Intangible Assets, and that the management refuses to derecognise the

asset.

Problems were experienced in the audit of inventories. Due to an oversight by the internal auditors of Blod Co, the

external audit team did not receive a copy of inventory counting procedures prior to attending the count. This caused

a delay at the beginning of the inventory count, when the audit team had to quickly familiarise themselves with the

procedures. In addition, on the final audit, when the audit senior requested documentation to support the final

inventory valuation, it took two weeks for the information to be received because the accountant who had prepared

the schedules had mislaid them.

Required:

(a) (i) Identify the main purpose of including ‘findings from the audit’ (management letter points) in a report

to those charged with governance. (2 marks)

正确答案:

5 Blod Co

(a) (i) A report to those charged with governance is produced to communicate matters relating to the external audit to those

who are ultimately responsible for the financial statements. ISA 260 Communication of Audit Matters With Those

Charged With Governance requires the auditor to communicate many matters, including independence and other ethical

issues, the audit approach and scope, the details of management representations, and the findings of the audit. The

findings of the audit are commonly referred to as management letter points. By communicating these matters, the auditor

is confident that there is written documentation outlining all significant matters raised during the audit process, and that

such matters have been formally notified to the highest level of management of the client. For the management, the

report should ensure that they fully understand the scope and results of the audit service which has been provided, and

is likely to provide constructive comments to help them to fulfil their duties in relation to the financial statements and

accounting systems and controls more effectively. The report should also include, where relevant, any actions that

management has indicated they will take in relation to recommendations made by the auditors. -

第4题:

The development of agriculture in this area has reached a new ________ in the last few years.A、belt

B、bicycle

C、build

D、level

正确答案:D

-

第5题:

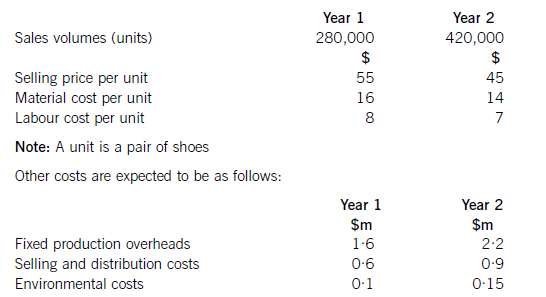

Shoe Co, a shoe manufacturer, has developed a new product called the ‘Smart Shoe’ for children, which has a built-in tracking device. The shoes are expected to have a life cycle of two years, at which point Shoe Co hopes to introduce a new type of Smart Shoe with even more advanced technology. Shoe Co plans to use life cycle costing to work out the total production cost of the Smart Shoe and the total estimated profit for the two-year period.

Shoe Co has spent $5·6m developing the Smart Shoe. The time spent on this development meant that the company missed out on the opportunity of earning an estimated $800,000 contribution from the sale of another product.

The company has applied for and been granted a ten-year patent for the technology, although it must be renewed each year at a cost of $200,000. The costs of the patent application were $500,000, which included $20,000 for the salary costs of Shoe Co’s lawyer, who is a permanent employee of the company and was responsible for preparing the application.

The following information is also available for the next two years:

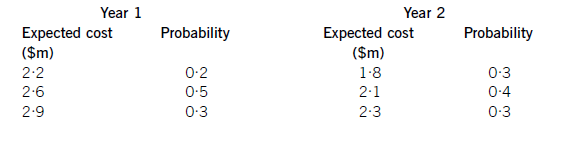

Shoe Co is still negotiating with marketing companies with regard to its advertising campaign, so is uncertain as to what the total marketing costs will be each year. However, the following information is available as regards the probabilities of the range of costs which are likely to be incurred:

Required:

Applying the principles of life cycle costing, calculate the total expected profit for Shoe Co for the two-year period.

(10 marks)

正确答案:

Totalsalesrevenue=(280,000x$55)+(420,000x$45)=$15·4m+18·9m=$34·3m.NoteTheexpectedprofithasbeencalculatedusinglifecyclecostingnotrelevantcosting.Hence,the$20,000salarycostincludedinpatentcostsshouldbeincludedinthelifecyclecost.Similarly,theopportunitycostof$800,000isnotincludedusinglifecyclecostingwhereasifrelevantcostingwasbeingusedtodecideonaparticularcourseofaction,theopportunitycostwouldbeincluded.Working1Expectedmarketingcostinyear1:(0·2x$2·2m)+(0·5x$2·6m)+(0·3x$2·9m)=$2·61mExpectedmarketingcostyear2:(0·3x$1·8m)+(0·4x$2·1m)+(0·3x$2·3m)=$2·07mTotalexpectedmarketingcost=$4·68m -

第6题:

On my last voyage it ______ at the discharging port that some watches were pilfered.

A.happens

B.has happened

C.happened

D.had happened

正确答案:C

-

第7题:

The CEO of the company has been consistent ________ his policy associated with foreign investments over the last few years.A.of

B.with

C.at

D.for答案:B解析: -

第8题:

Expansion at Everall

After four consecutive years of record-breaking growth, Everall Technologies has announced plans to 41 its office facilities on Warner Road. The company has added over 200 employees in the last ten years alone, and is desperately in need of more space.

According to an Everall spokesperson, the construction firm chosen to undertake the project is Build Lite Inc., and the work is estimated to take a little over a year to complete.42in the plans are a four-storey sales center, an auditorium with seating for 500, and a parking lot able to accommodate up to 1,200 vehicles. Both Everall and Build Lite have declined to43the cost of the project at this time. However, independent analysts predict it could reach over $10 million.

阅读以上短文,回答191-193题。

第41题答案是__________A.submit

B.expand

C.release

D.organize答案:B解析:A“submit”提交,B“expand”拓展,扩大,C"release”发布,D“organize”组织。 -

第9题:

共用题干

第二篇

Around 45%of the UK's carbon dioxide emissions come from the energy people use every day-at home and when they travel.In order to generate that energy,fossil fuels(coal oil,and gas)are burnt,and these produce greenhouse gases-in particular carbon dioxide(CO2).Car emissions are a major problem, but the truth is that more CO2 comes from the energy used at home.The average household creates around

five and a half tonnes of CO2 a year,and it is the same CO2 that is changing the climate and damaging the environment.

CO2 and various other gases wrap the earth in an invisible blanket helping to prevent heat from escaping.Without this greenhouse effect,the average temperature on Earth would be around-18℃, compared with the current average of around+15℃.The composition of this blanket of gases has remained relatively constant for many thousands of years.However,since the industrial revolution began around 200 years ago,people have been burning increasing amounts of fossil fuels,thus releasing more CO2 and other greenhouse gases in the process.This has increased the heating effect of the blanket,trapping more of the sun's energy inside the Earth's atmosphere in turn the Earth's temperature has increased more rapidly in a shorter period of time than it has for thousands of years.

In 2008,the total UK CO2 emissions were 533 million tonnes.27%(144 million tonnes)of those emissions came from the energy used to heat,light,and power homes.Transport emissions caused by passenger cars,buses and motorcycles accounted for a further 16%(87 million tonnes)of the UK's CO2 emissions.These figures show that a significant amount of CO2 results from ordinary citizens carbon footprint in their daily activities and lifestyle.

The effects of climate change can be seen all around us.Weather patterns are becoming more and more fractured and uncertain,and over the last century trends in warm weather have become increasingly common.In the UK in the last 40 years,winters have grown warmer,with much heavier rainfall.One of the clearest shifts over the last 200 years is towards summers that are hotter and drier,causing pervasive(普遍的)water shortages.Recent years have been the hottest since records began and during August 2003,the hottest ever outdoor temperature in the UK was recorded-38.5℃.What is the author's opinion about the level of CO2 emissions in the UK?

A:The majority of CO2 emissions come from motorized transport.

B:CO2 emissions may cause climate change in the future.

C:More CO2 emissions come from homes than from cars.

D:The average citizen does not create much CO2.答案:C解析:本文以英国的情况为例,主要讲述了人们在日常生活中排出大量二氧化碳气体及这种情次对地球环境的影响。文章以英国二氧化碳气体的排放来源展开论述,指出由于人们活动消耗能源,使得大气中产生大量的二氧化碳。并通过具体数据来论述人类的日常活动排放的大量二氧化碳及其对气候所产生的不良影响。故本题选C。

由文章第一段第三句和第四句话的内容可知,家庭排放的二氧化碳气体占据二氧化碳排放量的主要部分,比汽车排放的多,故选C。

由文章第三段中的内容可知,2008年,在英国有16%的二氧化碳气体来自于交通工具的排放,这和D项意思相符,故选D。

文章第四段第三句话中提到,在过去40年里,英国的冬天变得更暖,降雨也更加猛烈, A、B、D三项的内容文中均未提及,故选C。

由第36题的解析可知,文章主要围绕在英国人们日常生活所排放的大量二氧化碳气体及其对气候的影响来展开。故本题最佳答案为B。 -

第10题:

Which of the following statements concerning intellectual property is wrong?()

- A、Intellectual property is an intangible creation

- B、Intellectual property in ludes patents,trademarks,copyrights,etc.

- C、Intellectual property is a visible creation

- D、There are some agreement sconcerning intellectual property under the WTO

正确答案:C -

第11题:

单选题The company has()some major changes in the last five years.Astood

Bsuffered

Cundergone

Dtolerated

正确答案: A解析: 暂无解析 -

第12题:

单选题______ my opinion, customer service here has improved but not as much as expected over the last 2 years.AOn

BIn

CFor

DWith

正确答案: C解析:

本题考查固定搭配。句意:在我看来,在过去的两年里,这里的客服质量有了改善,但仍未如预料中的理想。in one’s opinion为固定搭配,意为“在……看来”。故B项为正确答案。 -

第13题:

(b) (i) Advise Alasdair of the tax implications and relative financial risks attached to the following property

investments:

(1) buy to let residential property;

(2) commercial property; and

(3) shares in a property investment company/unit trust. (9 marks)

正确答案:

(b) (i) Income tax:

Direct investment in residential or commercial property

The income will be taxed under Schedule A for both residential and commercial property investment. Expenses can be

offset against income under the normal trading rules. These will include interest charges incurred in borrowing funds to

acquire the properties. Schedule A losses are restricted to use against future Schedule A profits, with the earliest profits

being relieved first.

When acquiring commercial properties, it may be possible to claim capital allowances on the fixtures and plant held in

the building. In addition, industrial buildings allowances (IBA) may also be available if the property qualifies as an

industrial building.

Capital allowances are not normally available for fixtures and fittings included in a residential property. Instead, a wear

and tear allowance can be claimed if the property is furnished. This is equal to 10% of the rental income after any

tenants cost (for example, council tax) paid by the landlord.

Income tax is levied at the normal tax rates (10/22/40%) as appropriate.

Collective investment (shares in a property investment company/unit trust)

With collective investments, the investor either buys shares (in an investment company) or units (in an equity unit trust).

The income tax treatment of both is the same in that the investor receives dividends. These are taxed at 10% and 32·5%

respectively (for basic and higher rate taxpayers).

Investors are not able to claim income tax relief on either interest costs (of borrowing) or any other expenses.

Capital gains tax (CGT):

The normal rules apply for CGT purposes in all situations. Property investments do not normally qualify for business

rates of taper relief unless they are furnished holiday lets or in certain circumstances, commercial property. Investments

in unit trusts or property investment companies will never qualify for business taper rates.

It is possible to use an individual savings account (ISA) to make collective investments. If this is done, income and

capital gains will be exempt from tax.

Other taxes:

New commercial property is subject to value added tax (VAT) at the standard rate, but new residential property is subject

to VAT at the zero rate. If a commercial building is acquired second hand as an investment, VAT may be payable if a

previous owner has opted to tax the property. If this is the case, VAT at the standard rate will be payable on the purchase

price, and rental charges to tenants will also be subject to VAT, again at the standard rate.

The acquisition of shares is not subject ot VAT.

Stamp duty land tax (SDLT) will be payable broadly on the direct acquisition of any property. The rates vary from 0 to

4% depending on the value of the land and building and its nature (whether residential or non-residential). Stamp duty

is payable at a rate of 0·5% on the acquisition of shares.

Investment risks/benefits

Direct investment

Investing directly in property represents a long term investment, and unless this is the case, investment risks are high.

Substantial initial costs (such as SDLT, VAT and transactions costs) are incurred, and ongoing running costs (such as

letting agents’ fees and vacant periods) can be significant. The investments are illiquid, particularly commercial

properties which can take months to sell.

All types of properties are dependent on a cyclical market, and the values of property investments can vary significantly

as a result. However, residential property has (on a long term basis) proven to be a good hedge against inflation.

Collective investments

The nature of collective investments is that the investor’s risk is reduced by the investment being spread over a large

portfolio as opposed to one or a few properties. In addition, investors can take advantage of the higher levels of liquidity

afforded by such vehicles. -

第14题:

(b) You are the manager responsible for the audit of Poppy Co, a manufacturing company with a year ended

31 October 2008. In the last year, several investment properties have been purchased to utilise surplus funds

and to provide rental income. The properties have been revalued at the year end in accordance with IAS 40

Investment Property, they are recognised on the statement of financial position at a fair value of $8 million, and

the total assets of Poppy Co are $160 million at 31 October 2008. An external valuer has been used to provide

the fair value for each property.

Required:

(i) Recommend the enquiries to be made in respect of the external valuer, before placing any reliance on their

work, and explain the reason for the enquiries; (7 marks)

正确答案:

(b) (i) Enquiries in respect of the external valuer

Enquiries would need to be made for two main reasons, firstly to determine the competence, and secondly the objectivity

of the valuer. ISA 620 Using the Work of an Expert contains guidance in this area.

Competence

Enquiries could include:

– Is the valuer a member of a recognised professional body, for example a nationally or internationally recognised

institute of registered surveyors?

– Does the valuer possess any necessary licence to carry out valuations for companies?

– How long has the valuer been a member of the recognised body, or how long has the valuer been licensed under

that body?

– How much experience does the valuer have in providing valuations of the particular type of investment properties

held by Poppy Co?

– Does the valuer have specific experience of evaluating properties for the purpose of including their fair value within

the financial statements?

– Is there any evidence of the reputation of the valuer, e.g. professional references, recommendations from other

companies for which a valuation service has been provided?

– How much experience, if any, does the valuer have with Poppy Co?

Using the above enquiries, the auditor is trying to form. an opinion as to the relevance and reliability of the valuation

provided. ISA 500 Audit Evidence requires that the auditor gathers evidence that is both sufficient and appropriate. The

auditor needs to ensure that the fair values provided by the valuer for inclusion in the financial statements have been

arrived at using appropriate knowledge and skill which should be evidenced by the valuer being a member of a

professional body, and, if necessary, holding a licence under that body.

It is important that the fair values have been arrived at using methods allowed under IAS 40 Investment Property. If any

other valuation method has been used then the value recognised in the statement of financial position may not be in

accordance with financial reporting standards. Thus it is important to understand whether the valuer has experience

specifically in providing valuations that comply with IAS 40, and how many times the valuer has appraised properties

similar to those owned by Poppy Co.

In gauging the reliability of the fair value, the auditor may wish to consider how Poppy Co decided to appoint this

particular valuer, e.g. on the basis of a recommendation or after receiving references from companies for which

valuations had previously been provided.

It will also be important to consider how familiar the valuer is with Poppy Co’s business and environment, as a way to

assess the reliability and appropriateness of any assumptions used in the valuation technique.

Objectivity

Enquiries could include:

– Does the valuer have any financial interest in Poppy Co, e.g. shares held directly or indirectly in the company?

– Does the valuer have any personal relationship with any director or employee of Poppy Co?

– Is the fee paid for the valuation service reasonable and a fair, market based price?

With these enquiries, the auditor is gaining assurance that the valuer will perform. the valuation from an independent

point of view. If the valuer had a financial interest in Poppy Co, there would be incentive to manipulate the valuation in

a way best suited to the financial statements of the company. Equally if the valuer had a personal relationship with a

senior member of staff at Poppy Co, the valuer may feel pressured to give a favourable opinion on the valuation of the

properties.

The level of fee paid is important. It should be commensurate with the market rate paid for this type of valuation. If the

valuer was paid in excess of what might be considered a normal fee, it could indicate that the valuer was encouraged,

or even bribed, to provide a favourable valuation. -

第15题:

-Okay, what is the decision? -As you know, we have been a privately held, family-owned company for over 120 years,_____________.A and I think it definitely has a bright future ;

B but it may be time to consider some major changes ;

C but the company faces tough competition

参考答案:B

-

第16题:

During the last few years ,it has been realized that maintenance of programs is more expensive than development, so reading of programs by humans is as important as(73)them.

A.editing

B.writed

C.written

D.writing

正确答案:D

解析:在过去的几年里,人们已经意识到程序的维护比开发更重要,所以程序的易读性和程序的书写一样重要。 -

第17题:

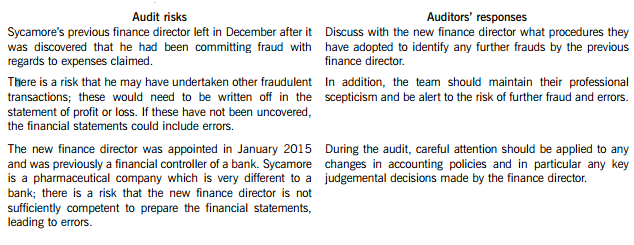

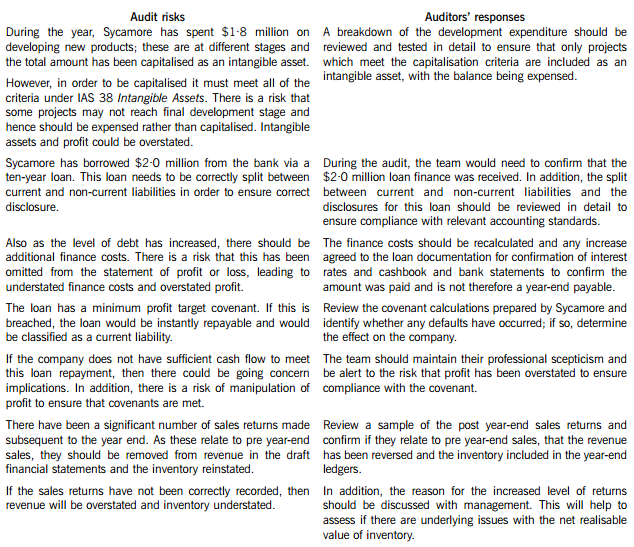

You are the audit supervisor of Maple & Co and are currently planning the audit of an existing client, Sycamore Science Co (Sycamore), whose year end was 30 April 2015. Sycamore is a pharmaceutical company, which manufactures and supplies a wide range of medical supplies. The draft financial statements show revenue of $35·6 million and profit before tax of $5·9 million.

Sycamore’s previous finance director left the company in December 2014 after it was discovered that he had been claiming fraudulent expenses from the company for a significant period of time. A new finance director was appointed in January 2015 who was previously a financial controller of a bank, and she has expressed surprise that Maple & Co had not uncovered the fraud during last year’s audit.

During the year Sycamore has spent $1·8 million on developing several new products. These projects are at different stages of development and the draft financial statements show the full amount of $1·8 million within intangible assets. In order to fund this development, $2·0 million was borrowed from the bank and is due for repayment over a ten-year period. The bank has attached minimum profit targets as part of the loan covenants.

The new finance director has informed the audit partner that since the year end there has been an increased number of sales returns and that in the month of May over $0·5 million of goods sold in April were returned.

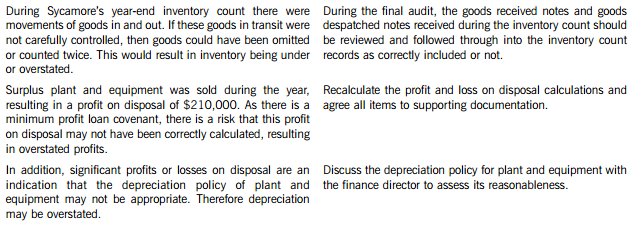

Maple & Co attended the year-end inventory count at Sycamore’s warehouse. The auditor present raised concerns that during the count there were movements of goods in and out the warehouse and this process did not seem well controlled.

During the year, a review of plant and equipment in the factory was undertaken and surplus plant was sold, resulting in a profit on disposal of $210,000.

Required:

(a) State Maples & Co’s responsibilities in relation to the prevention and detection of fraud and error. (4 marks)

(b) Describe SIX audit risks, and explain the auditor’s response to each risk, in planning the audit of Sycamore Science Co. (12 marks)

(c) Sycamore’s new finance director has read about review engagements and is interested in the possibility of Maple & Co undertaking these in the future. However, she is unsure how these engagements differ from an external audit and how much assurance would be gained from this type of engagement.

Required:

(i) Explain the purpose of review engagements and how these differ from external audits; and (2 marks)

(ii) Describe the level of assurance provided by external audits and review engagements. (2 marks)

正确答案:(a) Fraud responsibility

Maple & Co must conduct an audit in accordance with ISA 240 The Auditor’s Responsibilities Relating to Fraud in an Audit of Financial Statements and are responsible for obtaining reasonable assurance that the financial statements taken as a whole are free from material misstatement, whether caused by fraud or error.

In order to fulfil this responsibility, Maple & Co is required to identify and assess the risks of material misstatement of the financial statements due to fraud.

They need to obtain sufficient appropriate audit evidence regarding the assessed risks of material misstatement due to fraud, through designing and implementing appropriate responses. In addition, Maple & Co must respond appropriately to fraud or suspected fraud identified during the audit.

When obtaining reasonable assurance, Maple & Co is responsible for maintaining professional scepticism throughout the audit, considering the potential for management override of controls and recognising the fact that audit procedures which are effective in detecting error may not be effective in detecting fraud.

To ensure that the whole engagement team is aware of the risks and responsibilities for fraud and error, ISAs require that a discussion is held within the team. For members not present at the meeting, Sycamore’s audit engagement partner should determine which matters are to be communicated to them.

(b) Audit risks and auditors’ responses

(c) (i) Review engagements

Review engagements are often undertaken as an alternative to an audit, and involve a practitioner reviewing financial data, such as six-monthly figures. This would involve the practitioner undertaking procedures to state whether anything has come to their attention which causes the practitioner to believe that the financial data is not in accordance with the financial reporting framework.

A review engagement differs to an external audit in that the procedures undertaken are not nearly as comprehensive as those in an audit, with procedures such as analytical review and enquiry used extensively. In addition, the practitioner does not need to comply with ISAs as these only relate to external audits.

(ii) Levels of assurance

The level of assurance provided by audit and review engagements is as follows:

External audit – A high but not absolute level of assurance is provided, this is known as reasonable assurance. This provides comfort that the financial statements present fairly in all material respects (or are true and fair) and are free of material misstatements.

Review engagements – where an opinion is being provided, the practitioner gathers sufficient evidence to be satisfied that the subject matter is plausible; in this case negative assurance is given whereby the practitioner confirms that nothing has come to their attention which indicates that the subject matter contains material misstatements.

-

第18题:

Until security has been provided the Contractor shall have a maritime lien on ______ for his remuneration.

A.the property lost

B.the property salved

C.the property involved in the accident which gave rise to the salvage operations

D.any other property in danger which is not and has not been on board the vessel

正确答案:B

-

第19题:

Questions 76-79 refer to the following advertisement.

BONDHAM INTERNATIONAL

Bondham International, one of the leading real estate firm in the world, has been in business for over 50 years. We began our business by specializing in residential sales, primarily in Australia. Over time, our business has grown to include property rental and management services in locations throughout the world. We now sell, and manage over 15000 commercial and residential properties, and our global network includes employees in Australia, Canada, England, Kenya, and Mexico. We have won numerous industry awards, and our firm has been named one of the top ten international real estate firms by the World Association of Property Management.

In our effort to provide the highest quality service available, we have made significant investments in staff training. As a result, our sales agents offer a wealth of real estate expertise that our clients can always rely on. In addition, through market research and customer satisfaction surveys, we have been able to fulfill client expectations by consistently delivering the highest quality of service.

Whether you have interested in selling a home,

purchasing a commercial property, or simply obtaining expert real estate advice, Bondham International can respond effectively to your needs. Learn more about our firm by visiting our Website, www.bondhaminternational.co.au.

What is stated about Bondham International?A. Most of its work is done online.

B. The staff works only in Australia.

C. Its prices are the lowest in the industry.

D. It has expanded over the years.答案:D解析: -

第20题:

Questions 76-79 refer to the following advertisement.

BONDHAM INTERNATIONAL

Bondham International, one of the leading real estate firm in the world, has been in business for over 50 years. We began our business by specializing in residential sales, primarily in Australia. Over time, our business has grown to include property rental and management services in locations throughout the world. We now sell, and manage over 15000 commercial and residential properties, and our global network includes employees in Australia, Canada, England, Kenya, and Mexico. We have won numerous industry awards, and our firm has been named one of the top ten international real estate firms by the World Association of Property Management.

In our effort to provide the highest quality service available, we have made significant investments in staff training. As a result, our sales agents offer a wealth of real estate expertise that our clients can always rely on. In addition, through market research and customer satisfaction surveys, we have been able to fulfill client expectations by consistently delivering the highest quality of service.

Whether you have interested in selling a home,

purchasing a commercial property, or simply obtaining expert real estate advice, Bondham International can respond effectively to your needs. Learn more about our firm by visiting our Website, www.bondhaminternational.co.au.

What is the purpose of the advertisement?A. To advertise job opportunities in different countries.

B. To promote an industry publication.

C. To describe a company's reputation and services.

D. To announce the opening of a training facility.答案:C解析: -

第21题:

Henry's collection of wealth has gradually ______ over the last few years.A.built up

B.set up

C.covered up

D.doubled up答案:A解析:本题考查近义词辨析。题目意为“在过去的几年里,亨利逐渐积累了财富。”A选项“逐渐获得,逐渐建立”,B选项“树立,建立”,C选项“掩盖,盖住”,D选项“弯曲,对折”。 根据句意,逐渐获得财富,使用build up。

-

第22题:

单选题The company has()over the years into a multi-million dollar organization.Ainvolved

Bresolved

Cevolved

Drevolved

正确答案: D解析: 暂无解析 -

第23题:

单选题Which of the following statements concerning intellectual property is wrong?()AIntellectual property is an intangible creation

BIntellectual property in ludes patents,trademarks,copyrights,etc.

CIntellectual property is a visible creation

DThere are some agreement sconcerning intellectual property under the WTO

正确答案: C解析: 暂无解析