名词解释题年净现金流量(F,Net Annual Cash Flow)

题目

相似考题

更多“年净现金流量(F,Net Annual Cash Flow)”相关问题

-

第1题:

115 The technique most commonly used to determine the profitability of a project includes _____ methods.

A. Net present value (NPV).

B. Return on investment (ROI).

C. Discounted cash flow (DCF)

D. Payout time and risk sensitivity analysis.

E. All of the above

正确答案:E

-

第2题:

56 The future value of an annual income flow of $1000 for 2 years at 10% is:

A. $2,200

B. $2,280

C. $2,300

D. $2,310

E. None of the above

正确答案:D

-

第3题:

127 Using the situation stated in the Special window, what is net present value of an annual income flow of $1600 at 14% over the next three years?

A. $3713.60

B. $0.68

C. $1080.00

D. $476.19

E. $2.32

正确答案:A

-

第4题:

听力原文:If a statement that presents a summary of the revenues and expenses of a business unit for a specific period, what is it called?

(3)

A.the income statement

B.the balance sheet

C.the financial statement

D.the statement of cash flow

正确答案:A

解析:单句问的是“在一特定日期总结一家事业单位收益和亏损的报表是什么报表”,根据所学知识,这应是指损益表。 -

第5题:

Which term means “the amount of money which a business obtains (in a year) from customers by selling goods or services”?A、Annual income

B、operation profit

C、annual turnover

D、net profit

参考答案:C

-

第6题:

企业新增车辆后的年经营现金流入量的计算方法为( )。

A.年经营现金流量=年净收益

B.年经营现金流量=年净收益+残值

C.年经营现金流量=年营业收入-付现成本-所得税

D.年经营现金流量=年净收益+年折旧额

E.年经营现金流量=年净收益-残值

正确答案:CD

-

第7题:

某项目第6年累计净现金流量开始出现正值,第五年末累计净现金流量为-60万元,第6年当年净现金流量为240万元,则该项目的静态投资回收期为:A.4. 25 年

B.4.75 年

C.5.25 年

D.6.25 年答案:C解析:提示 根据静态投资回收期的计算公式:Pt = 6-1+ -60 /240=5.25(年)。 -

第8题:

自由现金流(Free Cash Flow)作为一种企业价值评估的新概念、理论、方法和体系。最早是由( )于20世纪80年代提出的。

Ⅰ.拉巴波特

Ⅱ.詹森

Ⅲ.斯科尔斯

Ⅳ.夏普

A、Ⅱ.Ⅳ

B、Ⅰ.Ⅳ

C、Ⅱ.Ⅲ

D、Ⅰ.Ⅱ答案:D解析:自由现金流(Free Cas hFlow)作为一种企业价值评估的新概念、理论、方法和体系,最早是由美国西北大学拉巴波特、哈佛大学詹森等学者于20世纪80年代提出的,经历20多年的发展,特别在以美国安然、世通等为代表的之前在财务报告中利润指标完美无瑕的所谓绩优公司纷纷破产后,已成为企业价值评估领域使用最广泛,理论最健全的指标。美国证监会更是要求公司年报中必须揭露这一指标。 -

第9题:

现金流量表(The Statement of Cash Flows)THCF

正确答案: 主要是要反映出资产负债表中各个项目对现金流量的影响,并根据其用途划分为经营、投资及融资三个活动分类。现金流量表可用于分析一家机构在短期内有没有足够现金去应付开销。 -

第10题:

填空题已知某项目第五年的净现金流量和累计净现金流量分别是100万元和-100万元,第六年的净现金流量和累计净现金流量分别是200万元和100万元,则该项目的投资回收期是()年。正确答案: 5.5解析: 暂无解析 -

第11题:

单选题(2013年)投资回收期小数部分等于()。A上年累计净现金流量的绝对值与当年净现金流量之比

B上年累计净现金流量的绝对值与当年净现金流量之积

C上年累计净现金流量的绝对值与当年净现金流量之和

D上年累计净现金流量的绝对值与当年净现金流量之差

正确答案: C解析: 暂无解析 -

第12题:

问答题Net Flow技术正确答案: 每一个数据报仍采用一般的第三层路由交换方式,处理之后路由器把第一个数据报文的信息记录在NetFlow高速缓存中,后继的数据报文到达之后首先在高速缓存中进行匹配查找,如果命中就使用高速缓存中的路由信息直接进行交换转发,否则再按通常的路由转发。解析: 暂无解析 -

第13题:

137 Which of the following is not a measure of the profitability of a project or program?

A. Return on original investment.

B. Net present value.

C. Depreciation.

D. Discounted cash flow.

E. None of the above

正确答案:C

-

第14题:

136 A technique that can be used to measure the total income of a project compared to the total moneys expended at any period of time is:

A. return on investment (ROI)

B. net present value (NPV)

C. discounted cash flow (DCF)

D. B and C

E. All of the above

正确答案:E

-

第15题:

(b) Discuss the key issues which the statement of cash flows highlights regarding the cash flow of the company.

(10 marks)

正确答案:

(b) Financial statement ratios can provide useful measures of liquidity but an analysis of the information in the cash flow

statement, particularly cash flow generated from operations, can provide specific insights into the liquidity of Warrburt. It is

important to look at the generation of cash and its efficient usage. An entity must generate cash from trading activity in order

to avoid the constant raising of funds from non-trading sources. The ‘quality of the profits’ is a measure of an entity’s ability

to do this. The statement of cash flow shows that the company has generated cash in the period despite sustaining a

significant loss ($92m cash flow but $21m loss). The problem is the fact that the entity will not be able to sustain this level

of cash generation if losses continue.

An important measure of cash flow is the comparison of the cash from operating activity to current liabilities. In the case of

Warrburt, this is $92m as compared to $155m. Thus the cash flow has not covered the current liabilities.

Operating cash flow ($92 million) determines the extent to which Warrburt has generated sufficient funds to repay loans,

maintain operating capability, pay dividends and make new investments without external financing. Operating cash flow

appears to be healthy, partially through the release of cash from working capital. This cash flow has been used to pay

contributions to the pension scheme, pay finance costs and income taxes. These uses of cash generated would be normal for

any entity. However, the release of working capital has also financed in part the investing activities of the entity which includes

the purchase of an associate and property, plant and equipment. The investing activities show a net cash outflow of

$43 million which has been financed partly out of working capital, partly from the sale of PPE and AFS financial assets and

partly out of cash generated from operations which include changes in working capital. It seems also that the issue of share

capital has been utilised to repay the long term borrowings and pay dividends. Also a significant amount of cash has been

raised through selling AFS investments. This may not continue in the future as it will depend on the liquidity of the market.

This action seems to indicate that the long term borrowings have effectively been ‘capitalised’. The main issue raised by the

cash flow statement is the use of working capital to partially finance investing activities. However, the working capital ratio

and liquidity ratios are still quite healthy but these ratios will deteriorate if the trend continues. -

第16题:

请根据短文内容判断给出的语句是否正确,正确的写“T”,错误的写“F”。

An annual report of a company provides information about its business performance for certain people. These people include the investors, potential investors and other stakeholders. From the report, people can understand the company's business scope, recent situation and future development. The main parts of an annual report usually include chairman's letter, operation analysis and financial statements.

·Chairman's Letter

Usually, an annual report should contain a letter from the chairman. The letter should provide details about the successes and the challenges of the past year. It should also include the future outlook for the company.

·Operation Analysis

The operation analysis is an overview of the business in the past year. It usually includes new hires and new product introductions. At the same time, it will introduce business acquisitions and other important issues.

·Financial Statements

The financial statements are very important for an annual report. People can know the company's performance in the past from the statements. It usually three aspects. The first one is the profit and loss statement. The second one is the balance sheet. And the third one is the cash flow statement.

( ) 26. An annual report of a company provides some information about its business performance for certain people.

( ) 27. People can know everything of the company from the annual report.

( ) 28. An annual report usually includes chairman's letter, financial statements and operation analysis.

( ) 29. A chairman's letter should include the strategic direction moving forward.

( ) 30. This passage is mainly about the main parts of an annual report.

参考答案:26-30:T F T F T

-

第17题:

(三) 假定有A、B两个项目,其净现金流量情况见下表:

年份

项目A

项目B

净现金流量

累计净现金流量

净现金流量

累计净现金流量

1

-500

-500

2

200

-300

300

-200

3

250

-50

350

150

4

250

350

第91题:项目B第4年的累计净现金流量是( )。

A.-50

B.-550

C.350

D.500

正确答案:D量=第3年的累计净现金流量+第4年的净现金流量=350+150=500.

-

第18题:

某项目第5年静态累计净现金流量开始出现正值,第4年年末累计净现金流量为-60万元,第5年当年净现金流量为240万元,则该项目的静态投资回收期为( )年。A.3.25

B.3.75

C.4.25

D.5.25答案:C解析: -

第19题:

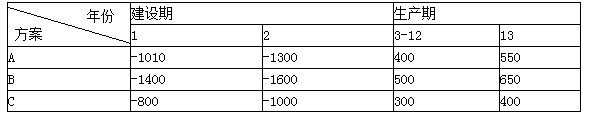

现有A、B、C三个互斥方案,寿命期均为13年,各方案的净现金流量如下表所示,假定ic=10%,净现金流均发生在年末。

各方案的净现金流量表

问题:(计算结果保留二位小数)

试用净现值法分析A、B、C三个方案是否可行,并选择出最佳方案。

已知:

(P/F,10%,1)=0.909

(P/F,10%,2)=0.826

(P/A,10%,10)=6.145

(P/F,10%,13)=0.290答案:解析:A、B、C方案的净现值计算结果分别如下:

NPVA=(-1010)×(P/F,10%,1)+(-1300)×(P/F,10%,2)+400×(P/A,10%,10)×(P/F,10%,2)+550×(P/F,10%,13)=197.9(万元)>0

NPVB=(-1400)×(P/F,10%,1)+(-1600)×(P/F,10%,2)+500×(P/A,10%,10)×(P/F,10%,2)+650×(P/F,10%,13) =132.2(万元)>0

NPVC=(-800)×(P/F,10%,1)+(-1000)×(P/F,10%,2)+300×(P/A,10%,10)×(P/F,10%,2)+400×(P/F,10%,13) =85.5(万元)>0

计算结果表明,A、B、C方案均大于0,方案A的净现值最大。因此三个方案均可行,A方案最佳。 -

第20题:

Net Flow技术

正确答案: 每一个数据报仍采用一般的第三层路由交换方式,处理之后路由器把第一个数据报文的信息记录在NetFlow高速缓存中,后继的数据报文到达之后首先在高速缓存中进行匹配查找,如果命中就使用高速缓存中的路由信息直接进行交换转发,否则再按通常的路由转发。 -

第21题:

已知某项目第五年的净现金流量和累计净现金流量分别是100万元和-100万元,第六年的净现金流量和累计净现金流量分别是200万元和100万元,则该项目的投资回收期是()年。

正确答案:5.5 -

第22题:

名词解释题现金流量分析(Cash Flow Analysis)正确答案: 是工业企业的工程项目从筹备、基建、试车投产、正常运行、直到经济寿命期结束,整个有效寿命期内、现金流出和现金流入的全部资金活动的分析。它反映了该项目的全部经济活动状况,也是计算该项目获利能力的基础。解析: 暂无解析 -

第23题:

名词解释题年净现金流量(F,Net Annual Cash Flow)正确答案: 就是一年内一个企业或一个项目各项现金流入和现金流出的代数和。

年净现金流量F.=净利润+年折旧费解析: 暂无解析 -

第24题:

名词解释题现金流量表(The Statement of Cash Flows)THCF正确答案: 主要是要反映出资产负债表中各个项目对现金流量的影响,并根据其用途划分为经营、投资及融资三个活动分类。现金流量表可用于分析一家机构在短期内有没有足够现金去应付开销。解析: 暂无解析