The value of the collateral must be ______.A.greater than the loan amountB.the same as or be greater than the loan amountC.smaller than the loan amountD.the same as the loan amount

题目

The value of the collateral must be ______.

A.greater than the loan amount

B.the same as or be greater than the loan amount

C.smaller than the loan amount

D.the same as the loan amount

相似考题

更多“The value of the collateral must be ______.A.greater than the loan amountB.the same as or be greater than the loan amountC.smaller than the loan amountD.the same as the loan amount”相关问题

-

第1题:

From this selection we may conclude that the king's crown______.

A. moved less water than pure gold of the same size

B. moved more water than pure gold of the same weight

C. moved more water than pure gold of the same size

D. moved less water than pure gold of the same weight

正确答案:B

51.答案为B 此题为推断题。根据阿基米德定理,我们可以得出关于国王的王冠的结论,答案选B。 -

第2题:

Usually the borrowing firm of term loans promises to repay ______.

A.the principal and interest until the end of the loan period

B.the principal and interest at the end of the loan period

C.the loan in a series of installments

D.at any time when cash is more abundant ______.

正确答案:C

解析:第一段第二句后半句...and then pledges to meet the scheduled repayment in a series of installments(often payments are made every quarter or even monthly),意指借款企业向银行保证分期还款,通常是按月或者按季度分期还款。Installment分期还款。 -

第3题:

听力原文: Some banks offer other types of loans repayable by monthly installments, such as business development loans, house improvement loans, and farm development loans. These may be either secured or unsecured. Secured loans attract a slightly lower rate of interest than unsecured loans. Some banks offer revolving credit schemes. These normally involve loans repayable by regular monthly installments, but they differ from other loans repayable by installments in two respects. First, the borrower need not take up the full amount of the loan at the outset. Secondly, as his repayments reduce his indebtedness, he can "top up" his loan by borrowing more, provided that the total debt outstanding does not exceed his agreed credit limit. In 1967 some banks introduced a new form. of account called a "budget account". The object is to allow personal customers to spread the incidence of normal personal and household expenditure.

24. Which of the following loans is not repaid by installments?

25.Which of the following loans would attract a lower rate of interest?

26.How does a borrower "top up" his loan?

27.What is the objective of introduction of the budget account?

(24)

A.Business development loans.

B.House improvement loans.

C.Farm development loans.

D.Overdrafts.

正确答案:D

解析:录音原文一开始提到Some banks offer...and farm development loans. 一些银行推出其他种类按月分期还款的贷款,例如商业发展贷款、住房改善贷款和农业发展贷款。 -

第4题:

听力原文:M: Most banks tend to decline loan proposals which are highly speculative.

W: I think because the banks expect the loan to generate sufficient profit and positive cash-flow for themselves and for the clients.

Q: What will the banks usually do to the highly speculative loan proposals?

(15)

A.The banks will disapprove them.

B.The banks will approve them.

C.The Bank will benefit from the loans.

D.The bank will make profit from lending.

正确答案:A

解析:根据男士的话可知银行对投机性高的贷款申请的态度是“decline”,即“拒绝”,A项正确。 -

第5题:

______ is a large loan, generally more than USD10 million, negotiated between a borrower and a single bank, but actually funded by a number of banks.

A.A project loan

B.A syndicated loan

C.An export credit

D.Consumer credit

正确答案:B

解析:project loan项目贷款。export credit出口信贷。consumer credit消费信贷。 -

第6题:

The bank's request for loan security is ______.

A.to make the loan more profitable

B.to make the loan more diversified

C.to reduce the loss in case of default

D.to guard against deterioration of loan collateral

正确答案:C

解析:文章第一段提到The main reason for requesting that…to repay the loan at maturity.银行在发放贷款时向借款人要求一定的抵押品,主要是为了降低风险,在借款人不能按时还款时,可以处置抵押品来降低贷款损失。 -

第7题:

By origin, English words can be classified as “native words” and “loan words”.( )此题为判断题(对,错)。

正确答案:正确

-

第8题:

听力原文:M: The rate on a personal loan is fixed according to the base rate at the time when the loan is made.

W: But it is always higher than the base rate, isn't it?

Q: What is determined when a personal loan is made?

(14)

A.Rate on the personal loan.

B.Base rate of the bank.

C.The amount of payment.

D.Personal loan's time period.

正确答案:A

解析:根据对话中"The rate on a personal loan is fixed"可知A项正确。 -

第9题:

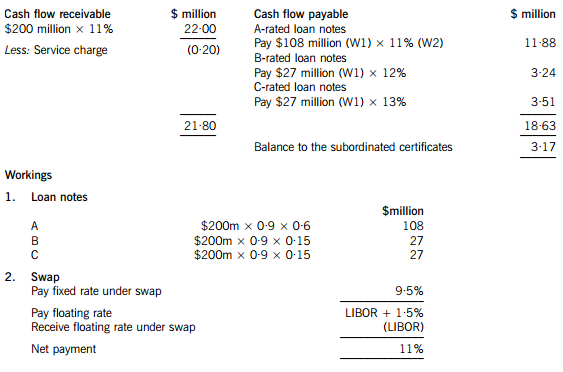

Moonstar Co is a property development company which is planning to undertake a $200 million commercial property development. Moonstar Co has had some difficulties over the last few years, with some developments not generating the expected returns and the company has at times struggled to pay its finance costs. As a result Moonstar Co’s credit rating has been lowered, affecting the terms it can obtain for bank finance. Although Moonstar Co is listed on its local stock exchange, 75% of the share capital is held by members of the family who founded the company. The family members who are shareholders do not wish to subscribe for a rights issue and are unwilling to dilute their control over the company by authorising a new issue of equity shares. Moonstar Co’s board is therefore considering other methods of financing the development, which the directors believe will generate higher returns than other recent investments, as the country where Moonstar Co is based appears to be emerging from recession.

Securitisation proposals

One of the non-executive directors of Moonstar Co has proposed that it should raise funds by means of a securitisation process, transferring the rights to the rental income from the commercial property development to a special purpose vehicle. Her proposals assume that the leases will generate an income of 11% per annum to Moonstar Co over a ten-year period. She proposes that Moonstar Co should use 90% of the value of the investment for a collateralised loan obligation which should be structured as follows:

– 60% of the collateral value to support a tranche of A-rated floating rate loan notes offering investors LIBOR plus 150 basis points

– 15% of the collateral value to support a tranche of B-rated fixed rate loan notes offering investors 12%

– 15% of the collateral value to support a tranche of C-rated fixed rate loan notes offering investors 13%

– 10% of the collateral value to support a tranche as subordinated certificates, with the return being the excess of receipts over payments from the securitisation process

The non-executive director believes that there will be sufficient demand for all tranches of the loan notes from investors. Investors will expect that the income stream from the development to be low risk, as they will expect the property market to improve with the recession coming to an end and enough potential lessees to be attracted by the new development.

The non-executive director predicts that there would be annual costs of $200,000 in administering the loan. She acknowledges that there would be interest rate risks associated with the proposal, and proposes a fixed for variable interest rate swap on the A-rated floating rate notes, exchanging LIBOR for 9·5%.

However the finance director believes that the prediction of the income from the development that the non-executive director has made is over-optimistic. He believes that it is most likely that the total value of the rental income will be 5% lower than the non-executive director has forecast. He believes that there is some risk that the returns could be so low as to jeopardise the income for the C-rated fixed rate loan note holders.

Islamic finance

Moonstar Co’s chief executive has wondered whether Sukuk finance would be a better way of funding the development than the securitisation.

Moonstar Co’s chairman has pointed out that a major bank in the country where Moonstar Co is located has begun to offer a range of Islamic financial products. The chairman has suggested that a Mudaraba contract would be the most appropriate method of providing the funds required for the investment.

Required:

(a) Calculate the amounts in $ which each of the tranches can expect to receive from the securitisation arrangement proposed by the non-executive director and discuss how the variability in rental income affects the returns from the securitisation. (11 marks)

(b) Discuss the benefits and risks for Moonstar Co associated with the securitisation arrangement that the non-executive director has proposed. (6 marks)

(c) (i) Discuss the suitability of Sukuk finance to fund the investment, including an assessment of its appeal to potential investors. (4 marks)

(ii) Discuss whether a Mudaraba contract would be an appropriate method of financing the investment and discuss why the bank may have concerns about providing finance by this method. (4 marks)

正确答案:(a) An annual cash flow account compares the estimated cash flows receivable from the property against the liabilities within the securitisation process. The swap introduces leverage into the arrangement.

The holders of the certificates are expected to receive $3·17million on $18 million, giving them a return of 17·6%. If the cash flows are 5% lower than the non-executive director has predicted, annual revenue received will fall to $20·90 million, reducing the balance available for the subordinated certificates to $2·07 million, giving a return of 11·5% on the subordinated certificates, which is below the returns offered on the B and C-rated loan notes. The point at which the holders of the certificates will receive nothing and below which the holders of the C-rated loan notes will not receive their full income will be an annual income of $18·83 million (a return of 9·4%), which is 14·4% less than the income that the non-executive director has forecast.

(b) Benefits

The finance costs of the securitisation may be lower than the finance costs of ordinary loan capital. The cash flows from the commercial property development may be regarded as lower risk than Moonstar Co’s other revenue streams. This will impact upon the rates that Moonstar Co is able to offer borrowers.

The securitisation matches the assets of the future cash flows to the liabilities to loan note holders. The non-executive director is assuming a steady stream of lease income over the next 10 years, with the development probably being close to being fully occupied over that period.

The securitisation means that Moonstar Co is no longer concerned with the risk that the level of earnings from the properties will be insufficient to pay the finance costs. Risks have effectively been transferred to the loan note holders.

Risks

Not all of the tranches may appeal to investors. The risk-return relationship on the subordinated certificates does not look very appealing, with the return quite likely to be below what is received on the C-rated loan notes. Even the C-rated loan note holders may question the relationship between the risk and return if there is continued uncertainty in the property sector.

If Moonstar Co seeks funding from other sources for other developments, transferring out a lower risk income stream means that the residual risks associated with the rest of Moonstar Co’s portfolio will be higher. This may affect the availability and terms of other borrowing.

It appears that the size of the securitisation should be large enough for the costs to be bearable. However Moonstar Co may face unforeseen costs, possibly unexpected management or legal expenses.

(c) (i) Sukuk finance could be appropriate for the securitisation of the leasing portfolio. An asset-backed Sukuk would be the same kind of arrangement as the securitisation, where assets are transferred to a special purpose vehicle and the returns and repayments are directly financed by the income from the assets. The Sukuk holders would bear the risks and returns of the relationship.

The other type of Sukuk would be more like a sale and leaseback of the development. Here the Sukuk holders would be guaranteed a rental, so it would seem less appropriate for Moonstar Co if there is significant uncertainty about the returns from the development.

The main issue with the asset-backed Sukuk finance is whether it would be as appealing as certainly the A-tranche of the securitisation arrangement which the non-executive director has proposed. The safer income that the securitisation offers A-tranche investors may be more appealing to investors than a marginally better return from the Sukuk. There will also be costs involved in establishing and gaining approval for the Sukuk, although these costs may be less than for the securitisation arrangement described above.

(ii) A Mudaraba contract would involve the bank providing capital for Moonstar Co to invest in the development. Moonstar Co would manage the investment which the capital funded. Profits from the investment would be shared with the bank, but losses would be solely borne by the bank. A Mudaraba contract is essentially an equity partnership, so Moonstar Co might not face the threat to its credit rating which it would if it obtained ordinary loan finance for the development. A Mudaraba contract would also represent a diversification of sources of finance. It would not require the commitment to pay interest that loan finance would involve.

Moonstar Co would maintain control over the running of the project. A Mudaraba contract would offer a method of obtaining equity funding without the dilution of control which an issue of shares to external shareholders would bring. This is likely to make it appealing to Moonstar Co’s directors, given their desire to maintain a dominant influence over the business.

The bank would be concerned about the uncertainties regarding the rental income from the development. Although the lack of involvement by the bank might appeal to Moonstar Co's directors, the bank might not find it so attractive. The bank might be concerned about information asymmetry – that Moonstar Co’s management might be reluctant to supply the bank with the information it needs to judge how well its investment is performing.

-

第10题:

John, CPA, is auditing the financial statements of ABC Bank Co.for the year ended December 31,20×8. The following information is available:

(a)John assessed the risk of material misstatements in short-term loan account at 80% and plans to limit to 10% the risk of failing to detect misstatements in the account equal to the tolerable error assigned to the account.

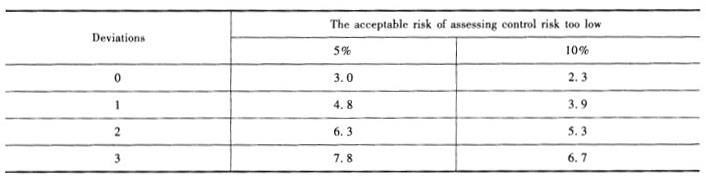

(b) John is testing the operating effectiveness of the loan approval procedure(a control activ- ity) related to granting loans. In 20×8,ABC Bank granted to 10 000 loans in total. John deter- mined that the acceptable risk of assessing control risk too low is 10%. He selected a sample made up of 60 sampling units and tested without any deviation found. Some Poisson Risk Factors(Relia- bility Factors) are reprinted as follows:

(c) John is using the Ratio Estimation Variable Sampling method to test the long-term loan balance at December 31, 20×8. The total recorded balance is RMB¥300 billion , made up of 4 000 items. John designed a sample made up of 200 items . The book value of the sample is RMB¥16. 5 billion. However, the audited value is RMB¥15. 6 billion.

(d) John is performing substantive procedures on interest income from short-term loan. The average annual market interest rate for short-term loan is 5 percent. The audited short-term loan balances of ABC Bank Co. at the end of each month in 20×8 are as follows:

Required :

(1) Based on (a) , calculate the acceptable detection risk.

(2) Based on (b) , calculate the upper limit of population deviation rate.

(3) Based on (c), make a point estimate of the misstatement in the population. Sampling error need not to be considered.

(4) Based on (d) , develop the expected result of interest income from short-term loan.

(5) Assume that after the tests mentioned in (d) , John found that the interest income from short-term loan was understated by RMB¥0. 05billion. Prepare the adjusting entry.

答案:解析:(1) acceptable detection risk = audit risk/the risk of material misstatement s = 10%/80% = 12. 5%

(2) The upper limit of population deviation rate = Poisson risk factor/sample size = 2. 3/60 = 3. 83 %

(3) ratio = 156/165 = 94. 54%

estimate the actual value of the population = 3 000*94. 54% = 283. 62 billion a point estimate of the misstatement in of the population =3 000 -283. 62 *10 = 16. 38 billion

(4) the expected result of interest income from short-term loan = (300 +320 +310 +300 + 330 +320 +320 +290 +310 +330 +300 +290)*5% =18. 6 billion

(5) the adjusting accounting entry:

Dr: Interest suspense 156

Cr: Interest income 156

-

第11题:

单选题Hot air can hold().Aless moisture than cold air

Bmore moisture than cold air

Cthe same amount of moisture as cold air

Dmoisture independent of air temperature

正确答案: A解析: 暂无解析 -

第12题:

单选题What kind of businesses are regarded as “small” in the UK?AThose with fewer than 50 employees.

BThose with only two or three owners.

CThose with a loan of 99.3%in their capital.

DThose with an output value less than £4 million.

正确答案: A解析:

由题干“small”定位至原文第五段,这里提到在英国拥有400万家公司,99.3%的公司都是小公司,公司人数少于50,由此可知答案是A项。 -

第13题:

单句理解

听力原文:For one full year when the full principal plus interest is paid together, compound interest and simple interest yield the same dollar amount.

(1)

A.If the time period of the loan is one year, the simple interest and compound interest are the same.

B.If the time period of the loan is the same, the simple interest and compound interest are the same.

C.When the full principal plus interest is paid together, compound interest and simple interest are of the same dollar amount.

D.When the full principal plus interest is paid together, compound interest and simple interest are not of the same dollar amount.

正确答案:A

解析:单句意思为“当本金和利息整整一年才一起支付时,复利计息和单利计息的数额一样”。 -

第14题:

The meeting suggested() the loan first.A、repaying

B、replied

C、to reply

参考答案:A

-

第15题:

The following statements concerning long-term debt are true except that ______.

A.long-term debt is a liability of a period longer than one year

B.long-term debts are paid in installments

C.despite of different payment plans, long-term debts are never classified as current liabilities

D.the loan borrowed by the company is a typical example of long-term debt

正确答案:C

-

第16题:

The meeting suggested()the loan first.

A. to reply

B. replied

C. repaying

参考答案:A

-

第17题:

Usually, a loan to government is safer than a loan to a private-sector borrower.

A.Right

B.Wrong

C.Doesn't say

正确答案:A

解析:从文中第三句话In any case, a loan to the foreign nation's government or its agencies is generally safer than a loan to a private-sector borrower.可以看出。 -

第18题:

If the value of the pledged asset is greater than the amount of the loan , ______ is entitled to have the excess.

A.the lending bank

B.the borrower

C.the guarantor

D.the guarantee

正确答案:B

解析:文章第二段提到the bank be forced to liquidate it…to the borrower.在贷款发生违约、银行处理抵押品时,如果抵押的资产价值高于贷款的金额时,银行只能收取贷款金额的相应部分,超过部分应由借款人获得。 -

第19题:

单句理解

听力原文:Collateral can never make a bad loan good, but it can turn a good loan into a better one.

(1)

A.Collateral sometimes turns a bad loan into a good one.

B.Good loans can be turned into better loans with collaterals.

C.Collateral can turn a good loan into a bad one.

D.Collateral can turn a bad loan into a worse one.

正确答案:B

解析:单句给出的信息是“贷款抵押物从不会使账目由坏变好,但可以由好变更好”,B项意思正确。 -

第20题:

(a) The following figures have been calculated from the financial statements (including comparatives) of Barstead for

the year ended 30 September 2009:

increase in profit after taxation 80%

increase in (basic) earnings per share 5%

increase in diluted earnings per share 2%

Required:

Explain why the three measures of earnings (profit) growth for the same company over the same period can

give apparently differing impressions. (4 marks)

(b) The profit after tax for Barstead for the year ended 30 September 2009 was $15 million. At 1 October 2008 the company had in issue 36 million equity shares and a $10 million 8% convertible loan note. The loan note will mature in 2010 and will be redeemed at par or converted to equity shares on the basis of 25 shares for each $100 of loan note at the loan-note holders’ option. On 1 January 2009 Barstead made a fully subscribed rights issue of one new share for every four shares held at a price of $2·80 each. The market price of the equity shares of Barstead immediately before the issue was $3·80. The earnings per share (EPS) reported for the year ended 30 September 2008 was 35 cents.

Barstead’s income tax rate is 25%.

Required:

Calculate the (basic) EPS figure for Barstead (including comparatives) and the diluted EPS (comparatives not required) that would be disclosed for the year ended 30 September 2009. (6 marks)

正确答案:

(a)Whilstprofitaftertax(anditsgrowth)isausefulmeasure,itmaynotgiveafairrepresentationofthetrueunderlyingearningsperformance.Inthisexample,userscouldinterpretthelargeannualincreaseinprofitaftertaxof80%asbeingindicativeofanunderlyingimprovementinprofitability(ratherthanwhatitreallyis:anincreaseinabsoluteprofit).Itispossible,evenprobable,that(someof)theprofitgrowthhasbeenachievedthroughtheacquisitionofothercompanies(acquisitivegrowth).Wherecompaniesareacquiredfromtheproceedsofanewissueofshares,orwheretheyhavebeenacquiredthroughshareexchanges,thiswillresultinagreaternumberofequitysharesoftheacquiringcompanybeinginissue.ThisiswhatappearstohavehappenedinthecaseofBarsteadastheimprovementindicatedbyitsearningspershare(EPS)isonly5%perannum.ThisexplainswhytheEPS(andthetrendofEPS)isconsideredamorereliableindicatorofperformancebecausetheadditionalprofitswhichcouldbeexpectedfromthegreaterresources(proceedsfromthesharesissued)ismatchedwiththeincreaseinthenumberofshares.Simplylookingatthegrowthinacompany’sprofitaftertaxdoesnottakeintoaccountanyincreasesintheresourcesusedtoearnthem.Anyincreaseingrowthfinancedbyborrowings(debt)wouldnothavethesameimpactonprofit(asbeingfinancedbyequityshares)becausethefinancecostsofthedebtwouldacttoreduceprofit.ThecalculationofadilutedEPStakesintoaccountanypotentialequitysharesinissue.Potentialordinarysharesarisefromfinancialinstruments(e.g.convertibleloannotesandoptions)thatmayentitletheirholderstoequitysharesinthefuture.ThedilutedEPSisusefulasitalertsexistingshareholderstothefactthatfutureEPSmaybereducedasaresultofsharecapitalchanges;inasenseitisawarningsign.InthiscasethelowerincreaseinthedilutedEPSisevidencethatthe(higher)increaseinthebasicEPShas,inpart,beenachievedthroughtheincreaseduseofdilutingfinancialinstruments.Thefinancecostoftheseinstrumentsislessthantheearningstheirproceedshavegeneratedleadingtoanincreaseincurrentprofits(andbasicEPS);however,inthefuturetheywillcausemoresharestobeissued.ThiscausesadilutionwherethefinancecostperpotentialnewshareislessthanthebasicEPS. -

第21题:

A celestial body will cross the prime vertical circle when the latitude is numerically ______.

A.greater than the declination and both are of the same name

B.less than the declination and both are of the same name

C.greater than the declination and both are of contrary name

D.less than the declination and both are of contrary name

正确答案:A

一天体将穿过东西圈,当纬度在数字上大于赤纬并且纬度和赤纬同名。 -

第22题:

When is the connection concentrator enabled?()

- A、When the value of MAX_CONNECTIONS is greater than the value of MAX_COORDAGENTS.

- B、When the value of MAX_AGENTS is greater than the value of MAX_CLIENTS.

- C、When the value of NUM_AGENTS is greater than the value of MAX_AGENTS.

- D、When the value of NUM_CONNECTIONS is greater than the value of NUM_COORDAGENTS.

正确答案:A -

第23题:

单选题When paralleling two AC generators, the frequency of the machine coming on-line, immediately prior to closing its breaker, should be ()Aslightly less than the oncoming generator frequency

Bthe same as the bus frequency

Cslightly greater than the bus frequency

Dthe same as the bus voltage

正确答案: A解析: 暂无解析