6 Andrew is aged 38 and is single. He is employed as a consultant by Bestadvice & Co and pays income tax at thehigher rate.Andrew is considering investing in a new business, and to provide funds for this investment he has recently disposedof the following

题目

6 Andrew is aged 38 and is single. He is employed as a consultant by Bestadvice & Co and pays income tax at the

higher rate.

Andrew is considering investing in a new business, and to provide funds for this investment he has recently disposed

of the following assets:

(1) A short leasehold interest in a residential property. Andrew originally paid £50,000 for a 47 year lease of the

property in May 1995, and assigned the lease in May 2006 for £90,000.

(2) His holding of £10,000 7% Government Stock, on which interest is payable half-yearly on 20 April and

20 October. Andrew originally purchased this holding on 1 June 1999 for £9,980 and he sold it for £11,250

on 14 March 2005.

Andrew intends to subscribe for ordinary shares in a new company, Scalar Limited, which will be a UK based

manufacturing company. Three investors (including Andrew) have been identified, but a fourth investor may also be

invited to subscribe for shares. The investors are all unconnected, and would subscribe for shares in equal measure.

The intention is to raise £450,000 in this manner. The company will also raise a further £50,000 from the investors

in the form. of loans. Andrew has been told that he can take advantage of some tax reliefs on his investment in Scalar

Limited, but does not know anything about the details of these reliefs

Andrew’s employer, Bestadvice & Co, is proposing to change the staff pension scheme from a defined benefit scheme

to which the firm and the employees each contribute 6% of their annual salary, to a defined contribution scheme, to

which the employees will continue to contribute 6%, but the firm will contribute 8% of their annual salary. The

majority of Andrew’s colleagues are opposed to this move, but, given the increase in the firm’s contribution rate

Andrew himself is less sure that the proposal is without merit.

Required:

(a) (i) Calculate the chargeable gain arising on the assignment of the residential property lease in May 2006.

(2 marks)

相似考题

更多“6 Andrew is aged 38 and is single. He is employed as a consultant by Bestadvice Co and pays income tax at thehigher rate.Andrew is considering investing in a new business, and to provide funds for this investment he has recently disposedof the following ”相关问题

-

第1题:

6 Alasdair, aged 42, is single. He is considering investing in property, as he has heard that this represents a good

investment. In order to raise the funds to buy the property, he wants to extract cash from his personal company, Beezer

Limited, whose year end is 31 December.

Beezer Limited was formed on 1 May 1998 with £1,000 of capital issued as 1,000 £1 ordinary shares, and traded

until 1 January 2005 when Alasdair sold the trade and related assets. The company’s only asset is cash of

£120,000. Alasdair wants to extract this cash from the company with the minimum amount of tax payable. He is

considering either, paying himself a dividend of £120,000, on 31 March 2006, after which the company would have

no assets and be wound up or, leaving the cash in the company and then liquidating the company. Costs of liquidation

of £5,000 would then be incurred.

Since Beezer Limited ceased trading, Alasdair has been taken on as a partner at a marketing firm, Gallus & Co. He

estimates his profit share for the year of assessment 2005/06 will be £30,000. He has not made any capital disposals

in the current tax year.

Alasdair wishes to reinvest the cash extracted from Beezer Limited in property but is not sure whether he should invest

directly in residential or commercial property, or do so via some form. of collective investment. He is aware that Gallus

& Co are looking to rent a new warehouse which could be bought for £200,000. Alasdair thinks that he may be able

to buy the warehouse himself and lease it to his firm, but only if he can borrow the additional money to buy the

property.

Alasdair has a 25% shareholding in another company, Glaikit Limited, whose year end is 31 March. The remaining

shares in this company are held by his friend, Gill. Alasdair is considering borrowing £15,000 from Glaikit Limited

on 1 January 2006. He does not intend to pay any interest on the loan, which is likely to be written off some time

in 2007. Alasdair does not have any connection with Glaikit Limited other than his shareholding.

Required:

(a) Advise Alasdair whether or not a dividend payment will result in a higher after-tax cash sum than the

liquidation of Beezer Limited. Assume that either the dividend would be paid on 31 March 2006 or the

liquidation would take place on 31 March 2006. (9 marks)

Assume that Beezer Limited has always paid corporation tax at or above the small companies rate of 19%

and that the tax rates and allowances for 2004/05 apply throughout this part.

正确答案:

-

第2题:

(b) (i) Advise Andrew of the income tax (IT) and capital gains tax (CGT) reliefs available on his investment in

the ordinary share capital of Scalar Limited, together with any conditions which need to be satisfied.

Your answer should clearly identify any steps that should be taken by Andrew and the other investors

to obtain the maximum relief. (13 marks)

正确答案:

(b) (i) Andrew may be able to take advantage of tax reliefs under the enterprise investment scheme (EIS) provided the

necessary conditions are met. The conditions that have to be satisfied before full relief is available fall into three areas,

and broadly require that a ‘qualifying individual’ subscribes for ‘eligible shares’ in a ‘qualifying company’.

‘Qualifying Individual’

To be a qualifying individual, Andrew must not be connected with the EIS company. This means that he should not be

an employee (or, at the time the shares are issued, a director) or have an interest in (i.e. control) 30% or more of the

capital of the company. These conditions need to be satisfied throughout the period beginning two years before the share

issue and three years after the ‘relevant date’. Where the relevant date is defined as the later of the date the shares were

issued and the date on which the company commenced trading.

Andrew does not intend to become an employee (or director) of Scalar Limited, but he needs to exercise caution as to

how many shares he subscribes for. If only three investors subscribe for 100% of the shares, each will hold 33% of the

share capital. This exceeds the 30% limit and will mean that EIS relief (other than deferral relief) will not be available.

Therefore, Andrew and the other two investors should ensure not only that the potential fourth investor is recruited, but

that s/he subscribes for sufficient shares, such that none of them will hold 30% or more of the issued share capital, as

only then will they all attain qualifying individual status.

‘Eligible shares’

Qualifying shares need to be new ordinary shares which are subscribed for in cash and fully paid up at the time of issue.

The shares must not be redeemable for at least three years from the relevant date, and not carry any preferential rights

to dividends. On the basis of the information provided, the shares of Scalar Limited would qualify as eligible shares.

‘Qualifying Company’

The company must be unquoted, not controlled by another company, and engaged in qualifying business activities. The

latter requires that the company engage in a trading activity, which is carried on wholly or mainly in the UK, throughout

the three years following the relevant date. While certain trading activities, such as dealing in shares or trading in land,

are excluded, the manufacturing trade Scalar Limited proposes to carry on will qualify.

However, it is also necessary for at least 80% of the money raised to be used for the qualifying business activity within

12 months of the relevant date and the remaining 20% to be so used within the following 12 months. Andrew and the

other investors will thus have to ensure that Scalar Limited has not raised more funds than it is able to employ in the

business within the appropriate time periods.

Reliefs available:

Andrew can claim income tax relief at 20% income tax relief on the amount invested up to a maximum of £200,000

in any one tax year. The relief is given in the form. of a tax reducing allowance, which can reduce the investor’s income

tax liability to nil, but cannot be used to generate a tax refund. If the investment is made prior to 6 October in the tax

year, then 50% of the amount invested (up to a maximum of £25,000) can be treated as having been made in the

previous tax year.

Any capital gains arising on the sale of EIS shares will be fully exempt from capital gains tax provided that income tax

relief was given on the investment when made and has not been withdrawn. If the EIS shares are disposed of at a loss,

capital losses are still allowable, but reduced by the amount of any EIS relief attributable to the shares disposed of.

In addition, gains from the disposal of other assets can be deferred against the base cost of EIS shares acquired within

one year before and three years after their disposal. Such gains will, thus, not normally become chargeable until the EIS

shares themselves are disposed of. Further, for deferral relief to be available, it is not necessary for the investment to

qualify for EIS income tax relief, i.e. deferral is available even where the investor is not a qualifying individual. Thus,

Andrew could still defer the gain arising on the disposal of the residential property lease made in order to raise part of

the funds for his EIS investment, even if no fourth investor were to be found and his shareholding were to exceed 30%

of the issued share capital of Scalar Limited. Does not require the existence of income tax relief in order to be claimed.

Withdrawal of relief:

Any EIS relief claimed by Andrew will be withdrawn (partially or fully) if, within three year of the relevant date:

(1) he disposes of the shares;

(2) he receives value from the company;

(3) he ceases to be a qualifying individual; or

(4) Scalar Limited ceases to be a qualifying company.

With regard to receiving value from the company, the definition excludes dividends which do not exceed a normal rate

of return, but does include the repayment of any loans made to the company before the shares were issued, the provision

of benefits and the purchase of assets from the company at an undervalue. In this regard, Andrew and the other

subscribers should ensure that the £50,000 they are to invest in Scalar Limited as loan capital is appropriately timed

and structured relative to the issue of the EIS shares. -

第3题:

(c) Calculate and explain the amount of income tax relief that Gerard will obtain in respect of the pension

contributions he proposes to make in the tax year 2007/08 and contrast this with how his position could be

improved by delaying some of the contributions that he could have made in 2007/08 until 2008/09. You

should include relevant supporting calculations and quantify the additional tax savings arising as a result of

your advice.

You should ignore the proposed changes to the bonus scheme for this part of this question and assume that

Gerard’s income will not change in 2008/09. (12 marks)

正确答案:

-

第4题:

1 Stuart is a self-employed business consultant aged 58. He is married to Rebecca, aged 55. They have one child,

Sam, who is aged 24 and single.

In November 2005 Stuart sold a house in Plymouth for £422,100. Stuart had inherited the house on the death of

his mother on 1 May 1994 when it had a probate value of £185,000. The subsequent pattern of occupation was as

follows:

1 May 1994 to 28 February 1995 occupied by Stuart and Rebecca as main residence

1 March 1995 to 31 December 1998 unoccupied

1 January 1999 to 31 March 2001 let out (unfurnished)

1 April 2001 to 30 November 2001 occupied by Stuart and Rebecca

1 December 2001 to 30 November 2005 used occasionally as second home

Both Stuart and Rebecca had lived in London from March 1995 onwards. On 1 March 2001 Stuart and Rebecca

bought a house in London in their joint names. On 1 January 2002 they elected for their London house to be their

principal private residence with effect from that date, up until that point the Plymouth property had been their principal

private residence.

No other capital disposals were made by Stuart in the tax year 2005/06. He has £29,500 of capital losses brought

forward from previous years.

Stuart intends to invest the gross sale proceeds from the sale of the Plymouth house, and is considering two

investment options, both of which he believes will provide equal risk and returns. These are as follows:

(1) acquiring shares in Omikron plc; or

(2) acquiring further shares in Omega plc.

Notes:

1. Omikron plc is a listed UK trading company, with 50,250,000 shares in issue. Its shares currently trade at 42p

per share.

2. Stuart and Rebecca helped start up the company, which was then Omega Ltd. The company was formed on

1 June 1990, when they each bought 24,000 shares for £1 per share. The company became listed on 1 May

1997. On this date their holding was subdivided, with each of them receiving 100 shares in Omega plc for each

share held in Omega Ltd. The issued share capital of Omega plc is currently 10,000,000 shares. The share price

is quoted at 208p – 216p with marked bargains at 207p, 211p, and 215p.

Stuart and Rebecca’s assets (following the sale of the Plymouth house but before any investment of the proceeds) are

as follows:

Assets Stuart Rebecca

£ £

Family house in London 450,000 450,000

Cash from property sale 422,100 –

Cash deposits 165,000 165,000

Portfolio of quoted investments – 250,000

Shares in Omega plc see above see above

Life insurance policy note 1 note 1

Note:

1. The life insurance policy will pay out a sum of £200,000 on the death of the first spouse to die.

Stuart has recently been diagnosed with a serious illness. He is expected to live for another two or three years only.

He is concerned about the possible inheritance tax that will arise on his death. Both he and Rebecca have wills whose

terms transfer all assets to the surviving spouse. Rebecca is in good health.

Neither Stuart nor Rebecca has made any previous chargeable lifetime transfers for the purposes of inheritance tax.

Required:

(a) Calculate the taxable capital gain on the sale of the Plymouth house in November 2005 (9 marks)

正确答案:

Note that the last 36 months count as deemed occupation, as the house was Stuart’s principal private residence (PPR)

at some point during his period of ownership.

The first 36 months of the period from 1 March 1995 to 31 March 2001 qualifies as a deemed occupation period as

Stuart and Rebecca returned to occupy the property on 1 April 2001. The remainder of the period will be treated as a

period of absence, although letting relief is available for part of the period (see below).

The exempt element of the gain is the proportion during which the property was occupied, real or deemed. This is

£138,665 (90/139 x £214,160).

(2) The chargeable gain is restricted for the period that the property was let out. This is restricted to the lowest of the

following:

(i) the gain attributable to the letting period (27/139 x 214,160) = £41,599

(ii) £40,000

(iii) the total exempt PPR gain = £138,665

i.e. £40,000.

(3) The taper relief is effectively wasted, having restricted losses b/f to preserve the annual exemption. -

第5题:

2 Assume that today’s date is 1 July 2005.

Jan is aged 45 and single. He is of Danish domicile but has been working in the United Kingdom since 1 May 2004

and intends to remain in the UK for the medium to long term. Although Jan worked briefly in the UK in 1986, he

has forgotten how UK taxation works and needs some assistance before preparing his UK income tax return.

Jan’s salary from 1 May 2004 was £74,760 per annum. Jan also has a company car – a Jaguar XJ8 with a list price

of £42,550 including extras, and CO2 emissions of 242g/km. The car was available to him from 1 July 2004. Free

petrol is provided by the company. Jan has other taxable benefits amounting to £3,965.

Jan’s other 2004/05 income comprises:

£

Dividend income from UK companies (cash received) 3,240

Interest received on an ISA account 230

Interest received on a UK bank account 740

Interest remitted from an offshore account (net of 15% withholding tax) 5,100

Income remitted from a villa in Portugal (net of 45% withholding tax) 4,598

The total interest arising on the offshore account was £9,000 (gross). In addition, Jan has not remitted other

Portuguese rental income arising in the year, totalling a further £1,500 (gross).

Jan informs you that his employer is thinking of providing him with rented accommodation while he looks for a house

to buy. The accommodation would be a two bedroom flat, valued at £155,000 with an annual value of £6,000. It

would be made available from 6 August 2005. The company will pay the rent of £600 per month for the first six

months. All other bills will be paid by Jan.

Jan also informs you that he has 25,000 ordinary shares in Gilet Ltd (‘Gilet’), an unquoted UK trading company. He

has held these shares since August 1986 when he bought 2,500 shares at £4.07 per share. In January 1994, a

bonus issue gave each shareholder nine shares for each ordinary share held. In the last week all Gilet’s shareholders

have received an offer from Jumper plc (‘Jumper’) who wishes to acquire the shares. Jumper has offered the following:

– 3 shares in Jumper (currently trading at £3.55 per share) for every 5 shares in Gilet, and

– 25p cash per share

Required:

(a) Calculate Jan’s 2004/05 income tax (IT) payable. (11 marks)

正确答案:

-

第6题:

听力原文:M: Do you provide investment service?

W: Yes. We are a commercial bank. We help customers with the purchase and sales of securities.

Q: What does the man want to do?

(13)

A.He will provide investment service.

B.He will help the customers.

C.He will join the commercial bank.

D.He will purchase or sell securities.

正确答案:D

解析:当男士问对方是否提供投资服务时,女士回答道:"We help customers with the purchase and sales of securities."可知D项正确。 -

第7题:

He always wanted to have ____of books and he has recently bought four____.Ahundreds...hundreds

Bhundred...hundred

Chundreds...hundred

Dhundred...hundreds

正确答案:C

-

第8题:

The customer is considering an IBM System Storage DS8000. Which of the following indicates a requirement for the Business Partner to perform a TDA?()A. capacity above 500 TB

B. first in customer location

C. a new model has been released

D. sold without implementation service

参考答案:B

-

第9题:

A child has his pains because______.

A.he can not do whatever he wants to

B.he is not allowed to play in rain

C.he has a lot of new things to learn

D.he can not play at the seaside freely

正确答案:A

解析:见第二段最后两句话:孩子在他希望去做的事上并不自由,他总是被大人们告知哪些事要做哪些事不要做。 -

第10题:

If one has failed to report his or her income tax for quite a few years, he or she may be put in prison.A.Right

B.Wrong

C.Not mentioned答案:A解析: -

第11题:

Mike has been using RIS (Remote Installation Services), to install all new workstations on his network. A new Service Pack has recently been released from Microsoft and he wants to update his new image. He brings up his test workstation that has Windows 2000 Professional on it and installs the new Service Pack. What is the next step Mike must take?()

- A、Slipstream this Service Pack to the CD image on the RIS Server.

- B、Use xcopy to copy all files to the RIS server.

- C、Run Riprep.exe

- D、Run Sysprep.exe

正确答案:A -

第12题:

单选题The customer is considering an IBM System Storage DS8000. Which of the following indicates a requirement for the Business Partner to perform a TDA?()Acapacity above 500 TB

Bfirst in customer location

Ca new model has been released

Dsold without implementation service

正确答案: B解析: 暂无解析 -

第13题:

(c) Outline the ways in which Arthur and Cindy can reduce their income tax liability by investing in unquoted

shares and recommend, with reasons, which form. of investment best suits their circumstances. You are not

required to discuss the qualifying conditions applicable to the investment vehicle recommended. (5 marks)

You should assume that the income tax rates and allowances for the tax year 2005/06 apply throughout this

question

正确答案:

(c) Reduction of income tax liability by investing in unquoted shares

The two forms of investment

Income tax relief is available for investments in venture capital trusts (VCTs) and enterprise investment scheme (EIS) shares.

A VCT is a quoted company that invests in shares in a number of unquoted trading companies. EIS shares are shares in

qualifying unquoted trading companies.

Recommendation

The most suitable investment for Arthur and Cindy is a VCT for the following reasons.

– An investment in a VCT is likely to be less risky than investing directly in EIS companies as the risk will be spread over

a greater number of companies.

– The tax deduction is 40% of the amount invested as opposed to 20% for EIS shares.

– Dividends from a VCT are not taxable whereas dividends on EIS shares are taxed in the normal way. -

第14题:

2 Clifford and Amanda, currently aged 54 and 45 respectively, were married on 1 February 1998. Clifford is a higher

rate taxpayer who has realised taxable capital gains in 2007/08 in excess of his capital gains tax annual exemption.

Clifford moved into Amanda’s house in London on the day they were married. Clifford’s own house in Oxford, where

he had lived since acquiring it for £129,400 on 1 August 1996, has been empty since that date although he and

Amanda have used it when visiting friends. Clifford has been offered £284,950 for the Oxford house and has decided

that it is time to sell it. The house has a large garden such that Clifford is also considering an offer for the house and

a part only of the garden. He would then sell the remainder of the garden at a later date as a building plot. His total

sales proceeds will be higher if he sells the property in this way.

Amanda received the following income from quoted investments in 2006/07:

£

Dividends in respect of quoted trading company shares 1,395

Dividends paid by a Real Estate Investment Trust out of tax exempt property income 485

On 1 May 2006, Amanda was granted a 22 year lease of a commercial investment property. She paid the landlord

a premium of £6,900 and also pays rent of £2,100 per month. On 1 June 2006 Amanda granted a nine year

sub-lease of the property. She received a premium of £14,700 and receives rent of £2,100 per month.

On 1 September 2006 Amanda gave quoted shares with a value of £2,200 to a registered charity. She paid broker’s

fees of £115 in respect of the gift.

Amanda began working for Shearer plc, a quoted company, on 1 June 2006 having had a two year break from her

career. She earns an annual salary of £38,600 and was paid a bonus of £5,750 in August 2006 for agreeing to

come and work for the company. On 1 August 2006 Amanda was provided with a fully expensed company car,

including the provision of private petrol, which had a list price when new of £23,400 and a CO2 emissions rate of

187 grams per kilometre. Amanda is required to pay Shearer plc £22 per month in respect of the private use of the

car. In June and July 2006 Amanda used her own car whilst on company business. She drove 720 business miles

during this two month period and was paid 34 pence per mile. Amanda had PAYE of £6,785 deducted from her gross

salary in the tax year 2006/07.

After working for Shearer plc for a full year, Amanda becomes entitled to the following additional benefits:

– The opportunity to purchase a large number of shares in Shearer plc on 1 July 2007 for £3·30 per share. It is

anticipated that the share price on that day will be at least £7·50 per share. The company will make an interestfree

loan to Amanda equal to the cost of the shares to be repaid in two years.

– Exclusive free use of the company sailing boat for one week in August 2007. The sailing boat was purchased by

Shearer plc in January 2005 for use by its senior employees and costs the company £1,400 a week in respect

of its crew and other running expenses.

Required:

(a) (i) Calculate Clifford’s capital gains tax liability for the tax year 2007/08 on the assumption that the Oxford

house together with its entire garden is sold on 31 July 2007 for £284,950. Comment on the relevance

to your calculations of the size of the garden; (5 marks)

正确答案:

-

第15题:

5 Gagarin wishes to persuade a number of wealthy individuals who are business contacts to invest in his company,

Vostok Ltd. He also requires advice on the recoverability of input tax relating to the purchase of new premises.

The following information has been obtained from a meeting with Gagarin.

Vostok Ltd:

– An unquoted UK resident company.

– Gagarin owns 100% of the company’s ordinary share capital.

– Has 18 employees.

– Provides computer based services to commercial companies.

– Requires additional funds to finance its expansion.

Funds required by Vostok Ltd:

– Vostok Ltd needs to raise £420,000.

– Vostok Ltd will issue 20,000 shares at £21 per share on 31 August 2008.

– The new shareholder(s) will own 40% of the company.

– Part of the money raised will contribute towards the purchase of new premises for use by Vostok Ltd.

Gagarin’s initial thoughts:

– The minimum investment will be 5,000 shares and payment will be made in full on subscription.

– Gagarin has a number of wealthy business contacts who may be interested in investing.

– Gagarin has heard that it may be possible to obtain tax relief for up to 60% of the investment via the enterprise

investment scheme.

Wealthy business contacts:

– Are all UK resident higher rate taxpayers.

– May wish to borrow the funds to invest in Vostok Ltd if there is a tax incentive to do so.

New premises:

– Will cost £446,500 including value added tax (VAT).

– Will be used in connection with all aspects of Vostok Ltd’s business.

– Will be sold for £600,000 plus VAT in six years time.

– Vostok Ltd will waive the VAT exemption on the sale of the building.

The VAT position of Vostok Ltd:

– In the year ending 31 March 2009, 28% of Vostok Ltd’s supplies will be exempt for the purposes of VAT.

– This percentage is expected to reduce over the next few years.

– Irrecoverable input tax due to the company’s partially exempt status exceeds the de minimis limits.

Required:

(a) Prepare notes for Gagarin to use when speaking to potential investors. The notes should include:

(i) The tax incentives immediately available in respect of the amount invested in shares issued in

accordance with the enterprise investment scheme; (5 marks)

正确答案:

(a) (i) The tax incentives immediately available

Income tax

– The investor’s income tax liability for 2008/09 will be reduced by 20% of the amount subscribed for the shares.

– Up to half of the amount invested can be treated as if paid in 2007/08 rather than 2008/09. This is subject to a

maximum carryback of £50,000.

This ability to carryback relief to the previous year is useful where the investor’s income in 2008/09 is insufficient

to absorb all of the relief available.

Tutorial note

There would be no change to the income tax liability of 2007/08 where an amount is treated as if paid in that year.

This ensures that such a claim does not affect payments on account under the self assessment system. Instead, the

tax refund due is calculated by reference to 2007/08 but is deducted from the next payment of tax due from the

taxpayer or is repaid to the taxpayer.

Capital gains tax deferral

– For every £1 invested in Vostok Ltd, an investor can defer £1 of capital gain and thus, potentially, 40 pence of

capital gains tax.

– The gain deferred can be in respect of the disposal of any asset.

– The shares must be subscribed for within the four year period starting one year prior to the date on which the

disposal giving rise to the gain took place. -

第16题:

(ii) Write a letter to Donald advising him on the most tax efficient manner in which he can relieve the loss

incurred in the year to 31 March 2007. Your letter should briefly outline the types of loss relief available

and explain their relative merits in Donald’s situation. Assume that Donald will have no source of income

other than the business in the year of assessment 2006/07 and that any income he earned on a parttime

basis while at university was always less than his annual personal allowance. (9 marks)

Assume that the corporation tax rates and allowances for the financial year 2004 and the income tax rates

and allowances for 2004/05 apply throughout this question.

Relevant retail price index figures are:

January 1998 159·5

April 1998 162·6

正确答案:(ii) [Donald’s address] [Firm’s address]

Dear Donald [Date]

I understand that you have incurred a tax loss in your first year of trading. The following options are available in respect

of this loss.

1. The first option is to use the trading loss against other forms of income in the same year. If such a claim is made,

losses are offset against income before personal allowances.

Any excess loss can still be offset against capital gains of the year. However, any offset against capital gains is

before both taper relief and annual exemptions.

-

第17题:

The above chart shows individual income tax in China. The tax free threshold is 3,500 RMB per month. The tax rates are divided into 7 brackets. The lowest rate is 3% for income between 3,501 and 5,000, while the highest rate is 45% for income over 80,000. Therefore, the higher our income is, the more tax we should pay. Tax, which can be used in public services such as education, road construction, public health and so on, is very important to our country. As we all know, tax makes up a great part of our country’s revenue, and the development of our country depends on it. From what has been discussed above, we can see that it is everyone’s legal duty to pay tax because taxes contribute to the country and create benefits for everyone. Those who try to evade taxation are sure to be punished. In short, paying tax is our responsibility to society.Decide if each of the following statements is TRUE (T) or FALSE (F).

1. The purpose of the passage is to help people know the tips how to pay less tax.()

2. According to the chart, if a person’s monthly is 3600 yuan, he doesn’t need to pay tax.()

3. How much income tax a person pays each month depends on how much his/her income is.()

4. The underlined word “evade” in the last paragraph means increase.()

5. Personal income taxes are included in a government’s revenue.()

参考答案:FFTFT

-

第18题:

The exporter has gotten the funds before he ships the goods in foreign collection.

A.Right

B.Wrong

C.Doesn't say

正确答案:B

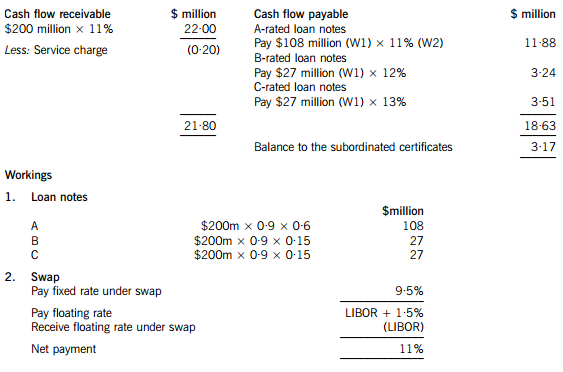

解析:倒数第二句是说Before the goods it has bought can be shipped, the importer must place funds with its bank,而不像题中所说的“出口商在发出货物之前,就已经拿到了托收款”。 -

第19题:

Moonstar Co is a property development company which is planning to undertake a $200 million commercial property development. Moonstar Co has had some difficulties over the last few years, with some developments not generating the expected returns and the company has at times struggled to pay its finance costs. As a result Moonstar Co’s credit rating has been lowered, affecting the terms it can obtain for bank finance. Although Moonstar Co is listed on its local stock exchange, 75% of the share capital is held by members of the family who founded the company. The family members who are shareholders do not wish to subscribe for a rights issue and are unwilling to dilute their control over the company by authorising a new issue of equity shares. Moonstar Co’s board is therefore considering other methods of financing the development, which the directors believe will generate higher returns than other recent investments, as the country where Moonstar Co is based appears to be emerging from recession.

Securitisation proposals

One of the non-executive directors of Moonstar Co has proposed that it should raise funds by means of a securitisation process, transferring the rights to the rental income from the commercial property development to a special purpose vehicle. Her proposals assume that the leases will generate an income of 11% per annum to Moonstar Co over a ten-year period. She proposes that Moonstar Co should use 90% of the value of the investment for a collateralised loan obligation which should be structured as follows:

– 60% of the collateral value to support a tranche of A-rated floating rate loan notes offering investors LIBOR plus 150 basis points

– 15% of the collateral value to support a tranche of B-rated fixed rate loan notes offering investors 12%

– 15% of the collateral value to support a tranche of C-rated fixed rate loan notes offering investors 13%

– 10% of the collateral value to support a tranche as subordinated certificates, with the return being the excess of receipts over payments from the securitisation process

The non-executive director believes that there will be sufficient demand for all tranches of the loan notes from investors. Investors will expect that the income stream from the development to be low risk, as they will expect the property market to improve with the recession coming to an end and enough potential lessees to be attracted by the new development.

The non-executive director predicts that there would be annual costs of $200,000 in administering the loan. She acknowledges that there would be interest rate risks associated with the proposal, and proposes a fixed for variable interest rate swap on the A-rated floating rate notes, exchanging LIBOR for 9·5%.

However the finance director believes that the prediction of the income from the development that the non-executive director has made is over-optimistic. He believes that it is most likely that the total value of the rental income will be 5% lower than the non-executive director has forecast. He believes that there is some risk that the returns could be so low as to jeopardise the income for the C-rated fixed rate loan note holders.

Islamic finance

Moonstar Co’s chief executive has wondered whether Sukuk finance would be a better way of funding the development than the securitisation.

Moonstar Co’s chairman has pointed out that a major bank in the country where Moonstar Co is located has begun to offer a range of Islamic financial products. The chairman has suggested that a Mudaraba contract would be the most appropriate method of providing the funds required for the investment.

Required:

(a) Calculate the amounts in $ which each of the tranches can expect to receive from the securitisation arrangement proposed by the non-executive director and discuss how the variability in rental income affects the returns from the securitisation. (11 marks)

(b) Discuss the benefits and risks for Moonstar Co associated with the securitisation arrangement that the non-executive director has proposed. (6 marks)

(c) (i) Discuss the suitability of Sukuk finance to fund the investment, including an assessment of its appeal to potential investors. (4 marks)

(ii) Discuss whether a Mudaraba contract would be an appropriate method of financing the investment and discuss why the bank may have concerns about providing finance by this method. (4 marks)

正确答案:(a) An annual cash flow account compares the estimated cash flows receivable from the property against the liabilities within the securitisation process. The swap introduces leverage into the arrangement.

The holders of the certificates are expected to receive $3·17million on $18 million, giving them a return of 17·6%. If the cash flows are 5% lower than the non-executive director has predicted, annual revenue received will fall to $20·90 million, reducing the balance available for the subordinated certificates to $2·07 million, giving a return of 11·5% on the subordinated certificates, which is below the returns offered on the B and C-rated loan notes. The point at which the holders of the certificates will receive nothing and below which the holders of the C-rated loan notes will not receive their full income will be an annual income of $18·83 million (a return of 9·4%), which is 14·4% less than the income that the non-executive director has forecast.

(b) Benefits

The finance costs of the securitisation may be lower than the finance costs of ordinary loan capital. The cash flows from the commercial property development may be regarded as lower risk than Moonstar Co’s other revenue streams. This will impact upon the rates that Moonstar Co is able to offer borrowers.

The securitisation matches the assets of the future cash flows to the liabilities to loan note holders. The non-executive director is assuming a steady stream of lease income over the next 10 years, with the development probably being close to being fully occupied over that period.

The securitisation means that Moonstar Co is no longer concerned with the risk that the level of earnings from the properties will be insufficient to pay the finance costs. Risks have effectively been transferred to the loan note holders.

Risks

Not all of the tranches may appeal to investors. The risk-return relationship on the subordinated certificates does not look very appealing, with the return quite likely to be below what is received on the C-rated loan notes. Even the C-rated loan note holders may question the relationship between the risk and return if there is continued uncertainty in the property sector.

If Moonstar Co seeks funding from other sources for other developments, transferring out a lower risk income stream means that the residual risks associated with the rest of Moonstar Co’s portfolio will be higher. This may affect the availability and terms of other borrowing.

It appears that the size of the securitisation should be large enough for the costs to be bearable. However Moonstar Co may face unforeseen costs, possibly unexpected management or legal expenses.

(c) (i) Sukuk finance could be appropriate for the securitisation of the leasing portfolio. An asset-backed Sukuk would be the same kind of arrangement as the securitisation, where assets are transferred to a special purpose vehicle and the returns and repayments are directly financed by the income from the assets. The Sukuk holders would bear the risks and returns of the relationship.

The other type of Sukuk would be more like a sale and leaseback of the development. Here the Sukuk holders would be guaranteed a rental, so it would seem less appropriate for Moonstar Co if there is significant uncertainty about the returns from the development.

The main issue with the asset-backed Sukuk finance is whether it would be as appealing as certainly the A-tranche of the securitisation arrangement which the non-executive director has proposed. The safer income that the securitisation offers A-tranche investors may be more appealing to investors than a marginally better return from the Sukuk. There will also be costs involved in establishing and gaining approval for the Sukuk, although these costs may be less than for the securitisation arrangement described above.

(ii) A Mudaraba contract would involve the bank providing capital for Moonstar Co to invest in the development. Moonstar Co would manage the investment which the capital funded. Profits from the investment would be shared with the bank, but losses would be solely borne by the bank. A Mudaraba contract is essentially an equity partnership, so Moonstar Co might not face the threat to its credit rating which it would if it obtained ordinary loan finance for the development. A Mudaraba contract would also represent a diversification of sources of finance. It would not require the commitment to pay interest that loan finance would involve.

Moonstar Co would maintain control over the running of the project. A Mudaraba contract would offer a method of obtaining equity funding without the dilution of control which an issue of shares to external shareholders would bring. This is likely to make it appealing to Moonstar Co’s directors, given their desire to maintain a dominant influence over the business.

The bank would be concerned about the uncertainties regarding the rental income from the development. Although the lack of involvement by the bank might appeal to Moonstar Co's directors, the bank might not find it so attractive. The bank might be concerned about information asymmetry – that Moonstar Co’s management might be reluctant to supply the bank with the information it needs to judge how well its investment is performing.

-

第20题:

—David has made great progress recently. —_______, and _______. A. So he has;so you have B. So he has;so have you C. So he has;so do you D. So has he;so you have

正确答案:B

-

第21题:

Which indefinite article "a" should be read emphatically in the following sentences

A.He is a handsome boy, but not smart.

B.He is not a suspect, he is the suspect.

C.He bought a cartoon book for his son.

D.He is talking with a middle-aged man.答案:B解析:考查虚词重读。本题要求找出不定冠词“a”在句中重读的情况。不定冠词属于虚词,通常情况下,虚词是不需要重读的,如果想表达一些强调的含义时,可以将所强调的虚词重读。A项强调的是形容词handsome.从第二个分句中的smart可以得知;B项的不定冠词“a”与后面的“the”形成对比,强调“他就是那个犯罪嫌疑人.而不是别人”,所以需要重读。C项和D项中的虚词没有表达任何特殊含义,所以不需要重读。故选B。 -

第22题:

The customer is considering an IBM System Storage DS8000. Which of the following indicates a requirement for the Business Partner to perform a TDA?()

- A、capacity above 500 TB

- B、first in customer location

- C、a new model has been released

- D、sold without implementation service

正确答案:B -

第23题:

单选题—Is that man Mr. Smith?—It ______ be him. He has gone to New York on business.Amay not

Bneedn’t

Ccan’t

Dmustn’t

正确答案: B解析:

本题考查情态动词辨析。句意:“—那个人是史密斯先生吗?—不可能是他。他去纽约出差了。”根据空格后这句“He has gone to New York on business.”可知,前面是肯定判断。may not可能不是;needn’t没必要;can’t不可能;mustn’t禁止。故选C项。