(b) The chief executive of Xalam Co, an exporter of specialist equipment, has asked for advice on the accountingtreatment and disclosure of payments made for security consultancy services. The payments, which aim toensure that consignments are not impound

题目

(b) The chief executive of Xalam Co, an exporter of specialist equipment, has asked for advice on the accounting

treatment and disclosure of payments made for security consultancy services. The payments, which aim to

ensure that consignments are not impounded in the destination country of a major customer, may be material to

the financial statements for the year ending 30 June 2006. Xalam does not treat these payments as tax

deductible. (4 marks)

Required:

Identify and comment on the ethical and other professional issues raised by each of these matters and state what

action, if any, Dedza should now take.

NOTE: The mark allocation is shown against each of the three situations.

相似考题

更多“(b) The chief executive of Xalam Co, an exporter of specialist equipment, has asked for advice on the accountingtreatment and disclosure of payments made for security consultancy services. The payments, which aim toensure that consignments are not impound”相关问题

-

第1题:

Payments should be made ( )sight draft.

A、at

B、upon

C、by

D、after

参考答案:C

-

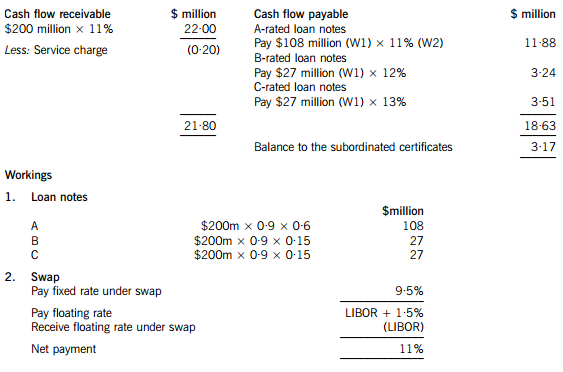

第2题:

Moonstar Co is a property development company which is planning to undertake a $200 million commercial property development. Moonstar Co has had some difficulties over the last few years, with some developments not generating the expected returns and the company has at times struggled to pay its finance costs. As a result Moonstar Co’s credit rating has been lowered, affecting the terms it can obtain for bank finance. Although Moonstar Co is listed on its local stock exchange, 75% of the share capital is held by members of the family who founded the company. The family members who are shareholders do not wish to subscribe for a rights issue and are unwilling to dilute their control over the company by authorising a new issue of equity shares. Moonstar Co’s board is therefore considering other methods of financing the development, which the directors believe will generate higher returns than other recent investments, as the country where Moonstar Co is based appears to be emerging from recession.

Securitisation proposals

One of the non-executive directors of Moonstar Co has proposed that it should raise funds by means of a securitisation process, transferring the rights to the rental income from the commercial property development to a special purpose vehicle. Her proposals assume that the leases will generate an income of 11% per annum to Moonstar Co over a ten-year period. She proposes that Moonstar Co should use 90% of the value of the investment for a collateralised loan obligation which should be structured as follows:

– 60% of the collateral value to support a tranche of A-rated floating rate loan notes offering investors LIBOR plus 150 basis points

– 15% of the collateral value to support a tranche of B-rated fixed rate loan notes offering investors 12%

– 15% of the collateral value to support a tranche of C-rated fixed rate loan notes offering investors 13%

– 10% of the collateral value to support a tranche as subordinated certificates, with the return being the excess of receipts over payments from the securitisation process

The non-executive director believes that there will be sufficient demand for all tranches of the loan notes from investors. Investors will expect that the income stream from the development to be low risk, as they will expect the property market to improve with the recession coming to an end and enough potential lessees to be attracted by the new development.

The non-executive director predicts that there would be annual costs of $200,000 in administering the loan. She acknowledges that there would be interest rate risks associated with the proposal, and proposes a fixed for variable interest rate swap on the A-rated floating rate notes, exchanging LIBOR for 9·5%.

However the finance director believes that the prediction of the income from the development that the non-executive director has made is over-optimistic. He believes that it is most likely that the total value of the rental income will be 5% lower than the non-executive director has forecast. He believes that there is some risk that the returns could be so low as to jeopardise the income for the C-rated fixed rate loan note holders.

Islamic finance

Moonstar Co’s chief executive has wondered whether Sukuk finance would be a better way of funding the development than the securitisation.

Moonstar Co’s chairman has pointed out that a major bank in the country where Moonstar Co is located has begun to offer a range of Islamic financial products. The chairman has suggested that a Mudaraba contract would be the most appropriate method of providing the funds required for the investment.

Required:

(a) Calculate the amounts in $ which each of the tranches can expect to receive from the securitisation arrangement proposed by the non-executive director and discuss how the variability in rental income affects the returns from the securitisation. (11 marks)

(b) Discuss the benefits and risks for Moonstar Co associated with the securitisation arrangement that the non-executive director has proposed. (6 marks)

(c) (i) Discuss the suitability of Sukuk finance to fund the investment, including an assessment of its appeal to potential investors. (4 marks)

(ii) Discuss whether a Mudaraba contract would be an appropriate method of financing the investment and discuss why the bank may have concerns about providing finance by this method. (4 marks)

正确答案:(a) An annual cash flow account compares the estimated cash flows receivable from the property against the liabilities within the securitisation process. The swap introduces leverage into the arrangement.

The holders of the certificates are expected to receive $3·17million on $18 million, giving them a return of 17·6%. If the cash flows are 5% lower than the non-executive director has predicted, annual revenue received will fall to $20·90 million, reducing the balance available for the subordinated certificates to $2·07 million, giving a return of 11·5% on the subordinated certificates, which is below the returns offered on the B and C-rated loan notes. The point at which the holders of the certificates will receive nothing and below which the holders of the C-rated loan notes will not receive their full income will be an annual income of $18·83 million (a return of 9·4%), which is 14·4% less than the income that the non-executive director has forecast.

(b) Benefits

The finance costs of the securitisation may be lower than the finance costs of ordinary loan capital. The cash flows from the commercial property development may be regarded as lower risk than Moonstar Co’s other revenue streams. This will impact upon the rates that Moonstar Co is able to offer borrowers.

The securitisation matches the assets of the future cash flows to the liabilities to loan note holders. The non-executive director is assuming a steady stream of lease income over the next 10 years, with the development probably being close to being fully occupied over that period.

The securitisation means that Moonstar Co is no longer concerned with the risk that the level of earnings from the properties will be insufficient to pay the finance costs. Risks have effectively been transferred to the loan note holders.

Risks

Not all of the tranches may appeal to investors. The risk-return relationship on the subordinated certificates does not look very appealing, with the return quite likely to be below what is received on the C-rated loan notes. Even the C-rated loan note holders may question the relationship between the risk and return if there is continued uncertainty in the property sector.

If Moonstar Co seeks funding from other sources for other developments, transferring out a lower risk income stream means that the residual risks associated with the rest of Moonstar Co’s portfolio will be higher. This may affect the availability and terms of other borrowing.

It appears that the size of the securitisation should be large enough for the costs to be bearable. However Moonstar Co may face unforeseen costs, possibly unexpected management or legal expenses.

(c) (i) Sukuk finance could be appropriate for the securitisation of the leasing portfolio. An asset-backed Sukuk would be the same kind of arrangement as the securitisation, where assets are transferred to a special purpose vehicle and the returns and repayments are directly financed by the income from the assets. The Sukuk holders would bear the risks and returns of the relationship.

The other type of Sukuk would be more like a sale and leaseback of the development. Here the Sukuk holders would be guaranteed a rental, so it would seem less appropriate for Moonstar Co if there is significant uncertainty about the returns from the development.

The main issue with the asset-backed Sukuk finance is whether it would be as appealing as certainly the A-tranche of the securitisation arrangement which the non-executive director has proposed. The safer income that the securitisation offers A-tranche investors may be more appealing to investors than a marginally better return from the Sukuk. There will also be costs involved in establishing and gaining approval for the Sukuk, although these costs may be less than for the securitisation arrangement described above.

(ii) A Mudaraba contract would involve the bank providing capital for Moonstar Co to invest in the development. Moonstar Co would manage the investment which the capital funded. Profits from the investment would be shared with the bank, but losses would be solely borne by the bank. A Mudaraba contract is essentially an equity partnership, so Moonstar Co might not face the threat to its credit rating which it would if it obtained ordinary loan finance for the development. A Mudaraba contract would also represent a diversification of sources of finance. It would not require the commitment to pay interest that loan finance would involve.

Moonstar Co would maintain control over the running of the project. A Mudaraba contract would offer a method of obtaining equity funding without the dilution of control which an issue of shares to external shareholders would bring. This is likely to make it appealing to Moonstar Co’s directors, given their desire to maintain a dominant influence over the business.

The bank would be concerned about the uncertainties regarding the rental income from the development. Although the lack of involvement by the bank might appeal to Moonstar Co's directors, the bank might not find it so attractive. The bank might be concerned about information asymmetry – that Moonstar Co’s management might be reluctant to supply the bank with the information it needs to judge how well its investment is performing.

-

第3题:

Given the advantages of electronic money,you might think that we would move quickly to the cashless society in which all payments are made electronically.1 a true cashless society is probably not around the corner.Indeed,predictions have been 2 for two decades but have not yet come to fruition.For example,Business Week predicted in 1975 that electronic means of payment would soon"revolutionize the very 3 of money itself,"only to 4itself several years later.Why has the movement to a cashless society been so 5 in coming?Although electronic means of payment may be more efficient than a payments system based on paper,several factors work 6 the disappearance of the paper system.First,it is very 7 to set up the computer,card reader,and telecornmunications networks necessary to make electronic money the 8 form of payment Second,paper checks have the advantage that they 9 receipts,something that many consumers are unwilling to 10.Third,the use of paper checks gives consumers several days of"float"-it takes several days 11 a check is cashed and funds are 12 from the issuer's account,which means that the writer of the check can cam interest on the funds in the meantime.13 electronic payments arc immediate,they eliminate the float for the consumer.Fourth,electronic means of payment may 14 security and privacy concerns.We often hear media reports that an unauthorized hacker has been able to access a computer database and to alter information 15 there.The fact that this is not an 16 occurrence means that dishonest persons might be able to access bank accounts in electronic payments systems and 17 from someone else's accounts.The 18 of this type of fraud is no easy task,and a new field of computer science is developing to 19 security issues.A further concern is that the use of electronic means of payment leaves an electronic 20 that contains a large amount of personal data.There are concerns that government,employers,and marketers might be able to access these data,thereby violating our privacy.19选?A.cope with

B.fight against

C.adapt to

D.call for答案:A解析:本题空格所在句为…and a new field of computer science is developing to__19 security issues.根据上下文应该选一个有“应对”安全问题含义的动词词组,A项cope with“处理,应对”,是最佳答案。【命题思路】本题考查考生对动词短语的掌握和应用。【干扰排除】本题根据上下文可排除C项和D项,B项“对抗,反抗”也不符合原文意思。 -

第4题:

In the Configuration Manager, under the WebSphere Commerce Instance Properties, what is the Payments panel used for? It allows an Administrator to:()

- A、drop and re-create the WebSphere Commerce Payments database.

- B、stop and start the Payment Engine.

- C、configure WebSphere Commerce Server communication with WebSphere Commerce Payments Server.

- D、specify what type of Database software will be used for the WebSphere Commerce Payments database.

正确答案:C -

第5题:

The carrier has to take care of the risk of freight payments by the individual shippers when handling LCL shipments.

正确答案:错误 -

第6题:

Which of the following are true about WebSphere Commerce Payments cassettes?()

- A、The site does not need a cassette, unless the site requires real-time credit card validation.

- B、A cassette is a piece of plug-in software that provides support for a specific payment system.

- C、The CyberCash cassette is installed by default, with the installation of WebSphere Commerce Payments.

- D、Third party companies can create custom cassettes that will work with WebSphere Commerce Payments.

- E、Cassettes convert the merchant payment request to the payment protocol of the local payment system.

正确答案:B,D,E -

第7题:

Which of the following would be true if an administrator tried to create a commerce instance with Commerce Payments configuration values, without having Commerce Payments installed?()

- A、The commerce instance would be created successfully.

- B、Attempting to configure payments instance after the commerce instance is already created will not be possible.

- C、The commerce instance creation will fail on the step that would normally configure the payments instance.

- D、After installing Commerce Payments, the administrator can enter the needed payment configuration values through the Administration Console.

正确答案:A -

第8题:

问答题Practice 5 ● Your company has decided to invest some of this year’s exceptionally high profits in one of the following areas: ● New company buses ● Culture comparative Courses ● Special bonus payments. ● You have been asked to write a report recommending how the profits should be invested and what benefits they would bring respectively. ● Write 200-250 words on your Answer Sheet.正确答案: 【参考范文】

Introduction

The purpose of this report is to analyze how the company should reinvest its profits this year. Options under consideration include purchasing new company buses, providing language training courses and paying special bonuses.

Findings

Options under consideration

New company buses

Despite that the motorcade of company buses are aged, they are still good enough to use. They are equipped with comfortable sofa seats, air-conditioning system and even karaoke. Therefore, their hardware is definitely not out of date. In addition, engines of these vehicles were only replaced last year, and they all came from Bolvo which run very smoothly. As a result, new company buses would be out of the question.

Culture comparative courses

Since the company is planning to increase its international market shares, especially in China and Japan, attending culture comparative courses would be very help for employees to deal with business partners and customers in those regions. Furthermore, courses would also increase cohesion, that is to say, staff members would get on with each other as classmates. They would certainly keep in memory this special period of happy time for many years to come. Therefore, the idea of investing in culture comparative courses is not bad.

Special bonus payments

As is known to all, special bonus payments would stimulate motivations. However, they would not have immediate improvement on the company’s overall performances. In addition, there’s also a potential hazard regarding the resentment of stall ineligible for the payments. If a precedent for future payments is set, think about what we shall do then to boost the morale in a rainy day. Therefore, it would be unwise to invest in bonus payments.

Recommendations

To conclude, investing in culture comparative courses will achieve a win-win situation for both the company and staff. It is recommended that the company arrange courses in Chinese and Japanese for employees who have contact with partners and customers in the above regions. As for other members of staff who are interested, they should also be encouraged to participate in.解析: 暂无解析 -

第9题:

单选题In the Configuration Manager, under the WebSphere Commerce Instance Properties, what is the Payments panel used for? It allows an Administrator to:()Adrop and re-create the WebSphere Commerce Payments database.

Bstop and start the Payment Engine.

Cconfigure WebSphere Commerce Server communication with WebSphere Commerce Payments Server.

Dspecify what type of Database software will be used for the WebSphere Commerce Payments database.

正确答案: B解析: 暂无解析 -

第10题:

单选题A financial industry customer will consolidate their Intel-based servers to a p5-550 running AIX, and needs experienced technical services. What information should the account executive provide to the customer to assure them that the technical specialist has the required experience?()AThe technical specialist has supported multiple Cluster 1350 environments. References will be provided.

BThe technical specialist is Linux-certified by two industry groups. Certificate copies will be provided.

CThe technical specialist has worked on multiple UNIX consolidation projects. References will be provided.

DThe technical specialist has worked on Linux consolidation efforts. References will be provided.

正确答案: A解析: 暂无解析 -

第11题:

判断题The carrier has to take care of the risk of freight payments by the individual shippers when handling LCL shipments.A对

B错

正确答案: 对解析: 暂无解析 -

第12题:

单选题Which of the following would be true if an administrator tried to create a commerce instance with Commerce Payments configuration values, without having Commerce Payments installed?()AThe commerce instance would be created successfully.

BAttempting to configure payments instance after the commerce instance is already created will not be possible.

CThe commerce instance creation will fail on the step that would normally configure the payments instance.

DAfter installing Commerce Payments, the administrator can enter the needed payment configuration values through the Administration Console.

正确答案: D解析: 暂无解析 -

第13题:

You are the network administrator for Ezonexam.com. The file server for the accounting department is a Windows 2000 Server computer named Ezonexam1. You have created a folder named Payments on the system partition of Ezonexam1. Payments is shared on the network as Payments with the default share permissions. The owner of the Payments folder is domain Admins. The NTFS permissions are shown in the following table.

NTFS Permissions

Domain Admins: Allow Read

Accounting: Allow Full Control

There is a file called review.doc in the Payment folder. The owner of review.doc is a user named Paul who is on a temporary leave of absence. The NTFS permissions for the file list only Paul on the access control list, with Full Control permission.

You want to remove Paul's access to review.doc and grant the Modify permission for a user named Lily Loo. You open the Security properties of review.doc and discover that you are unable to modify the permissions of the file.

You want to be able to remove Paul's access and grant Lily Loo the Modify permission on review.doc.

What should you do?

A.Take ownership of the file.

B.Take ownership of the Payments folder.

C.Grant Domain Admins Full control of the Payments shared folder.

D.Grant Domain Admins Change for the Payments shared folder.

正确答案:A

解析:Explanation: An administrator can take ownership of any file or folder. Then, as owner, the administrator can change permissions on the resource to grant Allow Take Ownership permission to the new owner, who then can take ownership of the resource.

Incorrect answers:

B: You should take ownership of the file and not the Payments Folder.

C: Granting the Domain Admins Full Control permission of the Payments shared folder is not the solution.

D: The Domain Admins should not be granted the Change permission on the shared folder.

-

第14题:

Given the advantages of electronic money,you might think that we would move quickly to the cashless society in which all payments are made electronically.1 a true cashless society is probably not around the corner.Indeed,predictions have been 2 for two decades but have not yet come to fruition.For example,Business Week predicted in 1975 that electronic means of payment would soon"revolutionize the very 3 of money itself,"only to 4itself several years later.Why has the movement to a cashless society been so 5 in coming?Although electronic means of payment may be more efficient than a payments system based on paper,several factors work 6 the disappearance of the paper system.First,it is very 7 to set up the computer,card reader,and telecornmunications networks necessary to make electronic money the 8 form of payment Second,paper checks have the advantage that they 9 receipts,something that many consumers are unwilling to 10.Third,the use of paper checks gives consumers several days of"float"-it takes several days 11 a check is cashed and funds are 12 from the issuer's account,which means that the writer of the check can cam interest on the funds in the meantime.13 electronic payments arc immediate,they eliminate the float for the consumer.Fourth,electronic means of payment may 14 security and privacy concerns.We often hear media reports that an unauthorized hacker has been able to access a computer database and to alter information 15 there.The fact that this is not an 16 occurrence means that dishonest persons might be able to access bank accounts in electronic payments systems and 17 from someone else's accounts.The 18 of this type of fraud is no easy task,and a new field of computer science is developing to 19 security issues.A further concern is that the use of electronic means of payment leaves an electronic 20 that contains a large amount of personal data.There are concerns that government,employers,and marketers might be able to access these data,thereby violating our privacy.6选?A.for

B.against

C.with

D.on答案:B解析:词义辨析【直击答案】本题空格所在句为several factors work__6 the disappearance of the paper system.本句前是由although“尽管…”引导的让步状语从句,故从句和主句含义是转折关系,意为“尽管电子支付方式可能比纸币支付方式更有效率,然而以下因素阻止了纸币系统的消失”,故答案为B项against。work against…“妨碍,对……产生消极影响”。【命题思路】本题考查考生对让步状语从句的理解,同时考查同一动词搭配不同介词动词短语意义的辨析。【干扰排除】本题四个选项是动词work搭配不同介词的动词短语,有一定干扰性。D项干扰性较强。如考生没有理解although引导的让步状语从句的含义,便会误选D。 -

第15题:

A customer SAN environment has undergone significant growth over the past two years. They havealso suffered a high turnover rate with administrative personnel. The customer has asked a storage specialist for help in documenting and understanding their changing SAN environment. The ability to make configuration changes to devices would be a plus. Which tool should the storage specialist suggest()

- A、Visio

- B、TPC Basic Edition

- C、IBM Tivoli NetView

- D、Fabric Manager

正确答案:B -

第16题:

How can WebSphere Commerce Payments be started?()

- A、By executing the payments ’startWCP’ command with the appropriate parameters.

- B、WebSphere Application Server provides a command to start it.

- C、The Configuration Manager provides a start option for it.

- D、From the WebSphere Commerce Payments User Interface.

- E、From the WebSphere Commerce Administration console.

正确答案:B,C -

第17题:

A financial industry customer will consolidate their Intel-based servers to a p5-550 running AIX, and needs experienced technical services. What information should the account executive provide to the customer to assure them that the technical specialist has the required experience?()

- A、The technical specialist has supported multiple Cluster 1350 environments. References will be provided.

- B、The technical specialist is Linux-certified by two industry groups. Certificate copies will be provided.

- C、The technical specialist has worked on multiple UNIX consolidation projects. References will be provided.

- D、The technical specialist has worked on Linux consolidation efforts. References will be provided.

正确答案:C -

第18题:

Which of the following methods can be used to enable/disable the Commerce Payments CustomOffline cassette?()

- A、From WebSphere Commerce Configuration Manager

- B、By updating the ENABLED column in the CASSETTES table

- C、By running the ’configureCassette’ command

- D、From WebSphere Commerce Administration Console

- E、From WebSphere Commerce Payments User Interface

正确答案:A,D,E -

第19题:

多选题How can WebSphere Commerce Payments be started?()ABy executing the payments ’startWCP’ command with the appropriate parameters.

BWebSphere Application Server provides a command to start it.

CThe Configuration Manager provides a start option for it.

DFrom the WebSphere Commerce Payments User Interface.

EFrom the WebSphere Commerce Administration console.

正确答案: A,C解析: 暂无解析 -

第20题:

问答题Practice 5 ● The company you work for has decided to join a scheme in which members of staff exchange places for six months with people from other companies overseas. ● The Chief Executive has asked you to suggest which members of staff should be the first to take part in this scheme and why. ● Write your proposal for the Chief Executive: ● suggesting which members of staff should be chosen and why they are suitable ● describing what their current responsibilities are ● explaining what these staff could learn from the exchange scheme ● outlining the benefits to the company as a whole of its participation in the scheme. ● Write 250~300 words on the separate answer paper provided.正确答案: 【参考范文】

Subject: Choosing employees for staff exchange scheme

As requested, I am submitting this report so as to give recommendations on selecting members of staff as the first to participate in a scheme in which members of staff exchange places for six months with people from other companies in England.

As for the ideal candidate, he or she will be a qualified accountant with no less than 3 years’ hands-on experience. He/she is expected to be confident and possesses excellent interpersonal and communication skills in English language. It will be an asset if he/she has a good understanding of American environment and culture.

I believe that most of the junior managers at the financial department are qualified for this scheme, for they can meet the requirements and obviously have an edge over staff of other departments. Their responsibility is about the financial control of the businesses, which includes accounting matters, cash flow management and negotiation with suppliers. Moreover, they can offer commercial support to the local managers and are heavily engaged in operational level, while managing overseas

With this scheme, staff will be more exposed to a different environment, which is bound to broaden their horizon, improve their English and sharpen their skills. I am certain that staff will have an indepth knowledge of and exposure to managing overseas businesses. Surely it would turn out to be a most rewarding experience to them as well. Exposed to different culture, the selected members will be able to share their knowledge with those never been out of China.

Providing staff with a unique experience of working overseas will boost their morale and make them valuable assets for the company. Their knowledge can also be used to expand operation home and abroad. Therefore, it will end up benefiting the company greatly.解析: 暂无解析 -

第21题:

多选题Which of the following are true about WebSphere Commerce Payments cassettes?()AThe site does not need a cassette, unless the site requires real-time credit card validation.

BA cassette is a piece of plug-in software that provides support for a specific payment system.

CThe CyberCash cassette is installed by default, with the installation of WebSphere Commerce Payments.

DThird party companies can create custom cassettes that will work with WebSphere Commerce Payments.

ECassettes convert the merchant payment request to the payment protocol of the local payment system.

正确答案: A,C解析: 暂无解析 -

第22题:

单选题The medical board, concerned by the drop in insurance payments and the failure of the accounting department to obtain the anticipated funds, resolved to pursue legal action against the insurance company.Aconcerned by the drop in insurance payments and the failure of the accounting department to obtain

Bconcerning the drop in payments by insurance and the failure of the accounting department to obtain

Cbecause of its concern for the dropping insurance payments and the accounting department’s failure at obtaining

Din its concern that the drop in insurance payments and the failure of the accounting department to obtain

Ebeing concerned about the drop in insurance payments and the accounting department falling to obtain

正确答案: D解析:

B项表意不明;C项“failure at obtaining”不符合习惯表达;D项结构不完整;E项中“being concerned about the drop”不符合习惯表达,故本题应选A项。 -

第23题:

多选题Which of the following methods can be used to enable/disable the Commerce Payments CustomOffline cassette?()AFrom WebSphere Commerce Configuration Manager

BBy updating the ENABLED column in the CASSETTES table

CBy running the ’configureCassette’ command

DFrom WebSphere Commerce Administration Console

EFrom WebSphere Commerce Payments User Interface

正确答案: E,D解析: 暂无解析