(b) A sale of industrial equipment to Deakin Co in May 2005 resulted in a loss on disposal of $0·3 million that hasbeen separately disclosed on the face of the income statement. The equipment cost $1·2 million when it waspurchased in April 1996 and was be

题目

(b) A sale of industrial equipment to Deakin Co in May 2005 resulted in a loss on disposal of $0·3 million that has

been separately disclosed on the face of the income statement. The equipment cost $1·2 million when it was

purchased in April 1996 and was being depreciated on a straight-line basis over 20 years. (6 marks)

Required:

For each of the above issues:

(i) comment on the matters that you should consider; and

(ii) state the audit evidence that you should expect to find,

in undertaking your review of the audit working papers and financial statements of Keffler Co for the year ended

31 March 2006.

NOTE: The mark allocation is shown against each of the three issues.

相似考题

更多“(b) A sale of industrial equipment to Deakin Co in May 2005 resulted in a loss on disposal of $0·3 million that hasbeen separately disclosed on the face of the income statement. The equipment cost $1·2 million when it waspurchased in April 1996 and was be”相关问题

-

第1题:

4 (a) Router, a public limited company operates in the entertainment industry. It recently agreed with a television

company to make a film which will be broadcast on the television company’s network. The fee agreed for the

film was $5 million with a further $100,000 to be paid every time the film is shown on the television company’s

channels. It is hoped that it will be shown on four occasions. The film was completed at a cost of $4 million and

delivered to the television company on 1 April 2007. The television company paid the fee of $5 million on

30 April 2007 but indicated that the film needed substantial editing before they were prepared to broadcast it,

the costs of which would be deducted from any future payments to Router. The directors of Router wish to

recognise the anticipated future income of $400,000 in the financial statements for the year ended 31 May

2007. (5 marks)

Required:

Discuss how the above items should be dealt with in the group financial statements of Router for the year ended

31 May 2007.

正确答案:

(a) Under IAS18 ‘Revenue’, revenue on a service contract is recognised when the outcome of the transaction can be measured

reliably. For revenue arising from the rendering of services, provided that all of the following criteria are met, revenue should

be recognised by reference to the stage of completion of the transaction at the balance sheet date (the percentage-ofcompletion

method) (IAS18 para 20):

(a) the amount of revenue can be measured reliably;

(b) it is probable that the economic benefits will flow to the seller;

(c) the stage of completion at the balance sheet date can be measured reliably; and

(d) the costs incurred, or to be incurred, in respect of the transaction can be measured reliably.

When the above criteria are not met, revenue arising from the rendering of services should be recognised only to the extent

of the expenses recognised that are recoverable. Because the only revenue which can be measured reliably is the fee for

making the film ($5 million), this should therefore be recognised as revenue in the year to 31 May 2007 and matched against

the cost of the film of $4 million. Only when the television company shows the film should any further amounts of $100,000

be recognised as there is an outstanding ‘performance’ condition in the form. of the editing that needs to take place before the

television company will broadcast the film. The costs of the film should not be carried forward and matched against

anticipated future income unless they can be deemed to be an intangible asset under IAS 38 ‘Intangible Assets’. Additionally,

when assessing revenue to be recognised in future years, the costs of the editing and Router’s liability for these costs should

be assessed.

-

第2题:

(b) One of the hotels owned by Norman is a hotel complex which includes a theme park, a casino and a golf course,

as well as a hotel. The theme park, casino, and hotel were sold in the year ended 31 May 2008 to Conquest, a

public limited company, for $200 million but the sale agreement stated that Norman would continue to operate

and manage the three businesses for their remaining useful life of 15 years. The residual interest in the business

reverts back to Norman after the 15 year period. Norman would receive 75% of the net profit of the businesses

as operator fees and Conquest would receive the remaining 25%. Norman has guaranteed to Conquest that the

net minimum profit paid to Conquest would not be less than $15 million. (4 marks)

Norman has recently started issuing vouchers to customers when they stay in its hotels. The vouchers entitle the

customers to a $30 discount on a subsequent room booking within three months of their stay. Historical

experience has shown that only one in five vouchers are redeemed by the customer. At the company’s year end

of 31 May 2008, it is estimated that there are vouchers worth $20 million which are eligible for discount. The

income from room sales for the year is $300 million and Norman is unsure how to report the income from room

sales in the financial statements. (4 marks)

Norman has obtained a significant amount of grant income for the development of hotels in Europe. The grants

have been received from government bodies and relate to the size of the hotel which has been built by the grant

assistance. The intention of the grant income was to create jobs in areas where there was significant

unemployment. The grants received of $70 million will have to be repaid if the cost of building the hotels is less

than $500 million. (4 marks)

Appropriateness and quality of discussion (2 marks)

Required:

Discuss how the above income would be treated in the financial statements of Norman for the year ended

31 May 2008.

正确答案:

(b) Property is sometimes sold with a degree of continuing involvement by the seller so that the risks and rewards of ownership

have not been transferred. The nature and extent of the buyer’s involvement will determine how the transaction is accounted

for. The substance of the transaction is determined by looking at the transaction as a whole and IAS18 ‘Revenue’ requires

this by stating that where two or more transactions are linked, they should be treated as a single transaction in order to

understand the commercial effect (IAS18 paragraph 13). In the case of the sale of the hotel, theme park and casino, Norman

should not recognise a sale as the company continues to enjoy substantially all of the risks and rewards of the businesses,

and still operates and manages them. Additionally the residual interest in the business reverts back to Norman. Also Norman

has guaranteed the income level for the purchaser as the minimum payment to Conquest will be $15 million a year. The

transaction is in substance a financing arrangement and the proceeds should be treated as a loan and the payment of profits

as interest.

The principles of IAS18 and IFRIC13 ‘Customer Loyalty Programmes’ require that revenue in respect of each separate

component of a transaction is measured at its fair value. Where vouchers are issued as part of a sales transaction and are

redeemable against future purchases, revenue should be reported at the amount of the consideration received/receivable less

the voucher’s fair value. In substance, the customer is purchasing both goods or services and a voucher. The fair value of the

voucher is determined by reference to the value to the holder and not the cost to the issuer. Factors to be taken into account

when estimating the fair value, would be the discount the customer obtains, the percentage of vouchers that would be

redeemed, and the time value of money. As only one in five vouchers are redeemed, then effectively the hotel has sold goods

worth ($300 + $4) million, i.e. $304 million for a consideration of $300 million. Thus allocating the discount between the

two elements would mean that (300 ÷ 304 x $300m) i.e. $296·1 million will be allocated to the room sales and the balance

of $3·9 million to the vouchers. The deferred portion of the proceeds is only recognised when the obligations are fulfilled.

The recognition of government grants is covered by IAS20 ‘Accounting for government grants and disclosure of government

assistance’. The accruals concept is used by the standard to match the grant received with the related costs. The relationship

between the grant and the related expenditure is the key to establishing the accounting treatment. Grants should not be

recognised until there is reasonable assurance that the company can comply with the conditions relating to their receipt and

the grant will be received. Provision should be made if it appears that the grant may have to be repaid.

There may be difficulties of matching costs and revenues when the terms of the grant do not specify precisely the expense

towards which the grant contributes. In this case the grant appears to relate to both the building of hotels and the creation of

employment. However, if the grant was related to revenue expenditure, then the terms would have been related to payroll or

a fixed amount per job created. Hence it would appear that the grant is capital based and should be matched against the

depreciation of the hotels by using a deferred income approach or deducting the grant from the carrying value of the asset

(IAS20). Additionally the grant is only to be repaid if the cost of the hotel is less than $500 million which itself would seem

to indicate that the grant is capital based. If the company feels that the cost will not reach $500 million, a provision should

be made for the estimated liability if the grant has been recognised. -

第3题:

3 You are the manager responsible for the audit of Albreda Co, a limited liability company, and its subsidiaries. The

group mainly operates a chain of national restaurants and provides vending and other catering services to corporate

clients. All restaurants offer ‘eat-in’, ‘take-away’ and ‘home delivery’ services. The draft consolidated financial

statements for the year ended 30 September 2005 show revenue of $42·2 million (2004 – $41·8 million), profit

before taxation of $1·8 million (2004 – $2·2 million) and total assets of $30·7 million (2004 – $23·4 million).

The following issues arising during the final audit have been noted on a schedule of points for your attention:

(a) In September 2005 the management board announced plans to cease offering ‘home delivery’ services from the

end of the month. These sales amounted to $0·6 million for the year to 30 September 2005 (2004 – $0·8

million). A provision of $0·2 million has been made as at 30 September 2005 for the compensation of redundant

employees (mainly drivers). Delivery vehicles have been classified as non-current assets held for sale as at 30

September 2005 and measured at fair value less costs to sell, $0·8 million (carrying amount,

$0·5 million). (8 marks)

Required:

For each of the above issues:

(i) comment on the matters that you should consider; and

(ii) state the audit evidence that you should expect to find,

in undertaking your review of the audit working papers and financial statements of Albreda Co for the year ended

30 September 2005.

NOTE: The mark allocation is shown against each of the three issues.

正确答案:3 ALBREDA CO

(a) Cessation of ‘home delivery’ service

(i) Matters

■ $0·6 million represents 1·4% of reported revenue (prior year 1·9%) and is therefore material.

Tutorial note: However, it is clearly not of such significance that it should raise any doubts whatsoever regarding

the going concern assumption. (On the contrary, as revenue from this service has declined since last year.)

■ The home delivery service is not a component of Albreda and its cessation does not classify as a discontinued

operation (IFRS 5 ‘Non-current Assets Held for Sale and Discontinued Operations’).

? It is not a cash-generating unit because home delivery revenues are not independent of other revenues

generated by the restaurant kitchens.

? 1·4% of revenue is not a ‘major line of business’.

? Home delivery does not cover a separate geographical area (but many areas around the numerous

restaurants).

■ The redundancy provision of $0·2 million represents 11·1% of profit before tax (10% before allowing for the

provision) and is therefore material. However, it represents only 0·6% of total assets and is therefore immaterial

to the balance sheet.

■ As the provision is a liability it should have been tested primarily for understatement (completeness).

■ The delivery vehicles should be classified as held for sale if their carrying amount will be recovered principally

through a sale transaction rather than through continuing use. For this to be the case the following IFRS 5 criteria

must be met:

? the vehicles must be available for immediate sale in their present condition; and

? their sale must be highly probable.

Tutorial note: Highly probable = management commitment to a plan + initiation of plan to locate buyer(s) +

active marketing + completion expected in a year.

■ However, even if the classification as held for sale is appropriate the measurement basis is incorrect.

■ Non-current assets classified as held for sale should be carried at the lower of carrying amount and fair value less

costs to sell.

■ It is incorrect that the vehicles are being measured at fair value less costs to sell which is $0·3 million in excess

of the carrying amount. This amounts to a revaluation. Wherever the credit entry is (equity or income statement)

it should be reversed. $0·3 million represents just less than 1% of assets (16·7% of profit if the credit is to the

income statement).

■ Comparison of fair value less costs to sell against carrying amount should have been made on an item by item

basis (and not on their totals).

(ii) Audit evidence

■ Copy of board minute documenting management’s decision to cease home deliveries (and any press

releases/internal memoranda to staff).

■ An analysis of revenue (e.g. extracted from management accounts) showing the amount attributed to home delivery

sales.

■ Redundancy terms for drivers as set out in their contracts of employment.

■ A ‘proof in total’ for the reasonableness/completeness of the redundancy provision (e.g. number of drivers × sum

of years employed × payment per year of service).

■ A schedule of depreciated cost of delivery vehicles extracted from the non-current asset register.

■ Checking of fair values on a sample basis to second hand market prices (as published/advertised in used vehicle

guides).

■ After-date net sale proceeds from sale of vehicles and comparison of proceeds against estimated fair values.

■ Physical inspection of condition of unsold vehicles.

■ Separate disclosure of the held for sale assets on the face of the balance sheet or in the notes.

■ Assets classified as held for sale (and other disposals) shown in the reconciliation of carrying amount at the

beginning and end of the period.

■ Additional descriptions in the notes of:

? the non-current assets; and

? the facts and circumstances leading to the sale/disposal (i.e. cessation of home delivery service). -

第4题:

(c) In October 2004, Volcan commenced the development of a site in a valley of ‘outstanding natural beauty’ on

which to build a retail ‘megastore’ and warehouse in late 2005. Local government planning permission for the

development, which was received in April 2005, requires that three 100-year-old trees within the valley be

preserved and the surrounding valley be restored in 2006. Additions to property, plant and equipment during

the year include $4·4 million for the estimated cost of site restoration. This estimate includes a provision of

$0·4 million for the relocation of the 100-year-old trees.

In March 2005 the trees were chopped down to make way for a car park. A fine of $20,000 per tree was paid

to the local government in May 2005. (7 marks)

Required:

For each of the above issues:

(i) comment on the matters that you should consider; and

(ii) state the audit evidence that you should expect to find,

in undertaking your review of the audit working papers and financial statements of Volcan for the year ended

31 March 2005.

NOTE: The mark allocation is shown against each of the three issues.

正确答案:

(c) Site restoration

(i) Matters

■ The provision for site restoration represents nearly 2·5% of total assets and is therefore material if it is not

warranted.

■ The estimated cost of restoring the site is a cost directly attributable to the initial measurement of the tangible fixed

asset to the extent that it is recognised as a provision under IAS 37 ‘Provisions, Contingent Liabilities and

Contingent Assets’ (IAS 16 ‘Property, Plant and Equipment’).

■ A provision should not be recognised for site restoration unless it meets the definition of a liability, i.e:

– a present obligation;

– arising from past events;

– the settlement of which is expected to result in an outflow of resources embodying economic benefits.

■ The provision is overstated by nearly $0·34m since Volcan is not obliged to relocate the trees and de facto has

only an obligation of $60,000 as at 31 March 2005 (being the penalty for having felled them). When considered

in isolation, this overstatement is immaterial (representing only 0·2% of total assets and 3·6% of PBT).

■ It seems that even if there are local government regulations calling for site restoration there is no obligation unless

the penalties for non-compliance are prohibitive (unlike the fines for the trees).

■ It is unlikely that commencement of site development has given rise to a constructive obligation, since past actions

(disregarding the preservation of the trees) must dispel any expectation that Volcan will honour any pledge to

restore the valley.

■ Whether commencing development of the site, and destroying the trees, conflicts with any statement of socioenvironmental

responsibility in the annual report.

(ii) Audit evidence

■ A copy of the planning application and permission granted setting out the penalties for non-compliance.

■ Payment of $60,000 to local government in May 2005 agreed to the bank statement.

■ The present value calculation of the future cash expenditure making up the $4·0m provision.

Tutorial note: Evidence supporting the calculation of $0·4m is irrelevant as there is no liability to be provided for.

■ Agreement that the pre-tax discount rate used reflects current market assessments of the time value of money (as

for (a)).

■ Asset inspection at the site as at 31 March 2005.

■ Any contracts entered into which might confirm or dispute management’s intentions to restore the site. For

example, whether plant hire (bulldozers, etc) covers only the period over which the warehouse will be constructed

– or whether it extends to the period in which the valley would be ‘made good’. -

第5题:

(b) You are the audit manager of Johnston Co, a private company. The draft consolidated financial statements for

the year ended 31 March 2006 show profit before taxation of $10·5 million (2005 – $9·4 million) and total

assets of $55·2 million (2005 – $50·7 million).

Your firm was appointed auditor of Tiltman Co when Johnston Co acquired all the shares of Tiltman Co in March

2006. Tiltman’s draft financial statements for the year ended 31 March 2006 show profit before taxation of

$0·7 million (2005 – $1·7 million) and total assets of $16·1 million (2005 – $16·6 million). The auditor’s

report on the financial statements for the year ended 31 March 2005 was unmodified.

You are currently reviewing two matters that have been left for your attention on the audit working paper files for

the year ended 31 March 2006:

(i) In December 2004 Tiltman installed a new computer system that properly quantified an overvaluation of

inventory amounting to $2·7 million. This is being written off over three years.

(ii) In May 2006, Tiltman’s head office was relocated to Johnston’s premises as part of a restructuring.

Provisions for the resulting redundancies and non-cancellable lease payments amounting to $2·3 million

have been made in the financial statements of Tiltman for the year ended 31 March 2006.

Required:

Identify and comment on the implications of these two matters for your auditor’s reports on the financial

statements of Johnston Co and Tiltman Co for the year ended 31 March 2006. (10 marks)

正确答案:

(b) Tiltman Co

Tiltman’s total assets at 31 March 2006 represent 29% (16·1/55·2 × 100) of Johnston’s total assets. The subsidiary is

therefore material to Johnston’s consolidated financial statements.

Tutorial note: Tiltman’s profit for the year is not relevant as the acquisition took place just before the year end and will

therefore have no impact on the consolidated income statement. Calculations of the effect on consolidated profit before

taxation are therefore inappropriate and will not be awarded marks.

(i) Inventory overvaluation

This should have been written off to the income statement in the year to 31 March 2005 and not spread over three

years (contrary to IAS 2 ‘Inventories’).

At 31 March 2006 inventory is overvalued by $0·9m. This represents all Tiltmans’s profit for the year and 5·6% of

total assets and is material. At 31 March 2005 inventory was materially overvalued by $1·8m ($1·7m reported profit

should have been a $0·1m loss).

Tutorial note: 1/3 of the overvaluation was written off in the prior period (i.e. year to 31 March 2005) instead of $2·7m.

That the prior period’s auditor’s report was unmodified means that the previous auditor concurred with an incorrect

accounting treatment (or otherwise gave an inappropriate audit opinion).

As the matter is material a prior period adjustment is required (IAS 8 ‘Accounting Policies, Changes in Accounting

Estimates and Errors’). $1·8m should be written off against opening reserves (i.e. restated as at 1 April 2005).

(ii) Restructuring provision

$2·3m expense has been charged to Tiltman’s profit and loss in arriving at a draft profit of $0·7m. This is very material.

(The provision represents 14·3% of Tiltman’s total assets and is material to the balance sheet date also.)

The provision for redundancies and onerous contracts should not have been made for the year ended 31 March 2006

unless there was a constructive obligation at the balance sheet date (IAS 37 ‘Provisions, Contingent Liabilities and

Contingent Assets’). So, unless the main features of the restructuring plan had been announced to those affected (i.e.

redundancy notifications issued to employees), the provision should be reversed. However, it should then be disclosed

as a non-adjusting post balance sheet event (IAS 10 ‘Events After the Balance Sheet Date’).

Given the short time (less than one month) between acquisition and the balance sheet it is very possible that a

constructive obligation does not arise at the balance sheet date. The relocation in May was only part of a restructuring

(and could be the first evidence that Johnston’s management has started to implement a restructuring plan).

There is a risk that goodwill on consolidation of Tiltman may be overstated in Johnston’s consolidated financial

statements. To avoid the $2·3 expense having a significant effect on post-acquisition profit (which may be negligible

due to the short time between acquisition and year end), Johnston may have recognised it as a liability in the

determination of goodwill on acquisition.

However, the execution of Tiltman’s restructuring plan, though made for the year ended 31 March 2006, was conditional

upon its acquisition by Johnston. It does not therefore represent, immediately before the business combination, a

present obligation of Johnston. Nor is it a contingent liability of Johnston immediately before the combination. Therefore

Johnston cannot recognise a liability for Tiltman’s restructuring plans as part of allocating the cost of the combination

(IFRS 3 ‘Business Combinations’).

Tiltman’s auditor’s report

The following adjustments are required to the financial statements:

■ restructuring provision, $2·3m, eliminated;

■ adequate disclosure of relocation as a non-adjusting post balance sheet event;

■ current period inventory written down by $0·9m;

■ prior period inventory (and reserves) written down by $1·8m.

Profit for the year to 31 March 2006 should be $3·9m ($0·7 + $0·9 + $2·3).

If all these adjustments are made the auditor’s report should be unmodified. Otherwise, the auditor’s report should be

qualified ‘except for’ on grounds of disagreement. If none of the adjustments are made, the qualification should still be

‘except for’ as the matters are not pervasive.

Johnston’s auditor’s report

If Tiltman’s auditor’s report is unmodified (because the required adjustments are made) the auditor’s report of Johnston

should be similarly unmodified. As Tiltman is wholly-owned by Johnston there should be no problem getting the

adjustments made.

If no adjustments were made in Tiltman’s financial statements, adjustments could be made on consolidation, if

necessary, to avoid modification of the auditor’s report on Johnston’s financial statements.

The effect of these adjustments on Tiltman’s net assets is an increase of $1·4m. Goodwill arising on consolidation (if

any) would be reduced by $1·4m. The reduction in consolidated total assets required ($0·9m + $1·4m) is therefore

the same as the reduction in consolidated total liabilities (i.e. $2·3m). $2·3m is material (4·2% consolidated total

assets). If Tiltman’s financial statements are not adjusted and no adjustments are made on consolidation, the

consolidated financial position (balance sheet) should be qualified ‘except for’. The results of operations (i.e. profit for

the period) should be unqualified (if permitted in the jurisdiction in which Johnston reports).

Adjustment in respect of the inventory valuation may not be required as Johnston should have consolidated inventory

at fair value on acquisition. In this case, consolidated total liabilities should be reduced by $2·3m and goodwill arising

on consolidation (if any) reduced by $2·3m.

Tutorial note: The effect of any possible goodwill impairment has been ignored as the subsidiary has only just been

acquired and the balance sheet date is very close to the date of acquisition. -

第6题:

(b) Seymour offers health-related information services through a wholly-owned subsidiary, Aragon Co. Goodwill of

$1·8 million recognised on the purchase of Aragon in October 2004 is not amortised but included at cost in the

consolidated balance sheet. At 30 September 2006 Seymour’s investment in Aragon is shown at cost,

$4·5 million, in its separate financial statements.

Aragon’s draft financial statements for the year ended 30 September 2006 show a loss before taxation of

$0·6 million (2005 – $0·5 million loss) and total assets of $4·9 million (2005 – $5·7 million). The notes to

Aragon’s financial statements disclose that they have been prepared on a going concern basis that assumes that

Seymour will continue to provide financial support. (7 marks)

Required:

For each of the above issues:

(i) comment on the matters that you should consider; and

(ii) state the audit evidence that you should expect to find,

in undertaking your review of the audit working papers and financial statements of Seymour Co for the year ended

30 September 2006.

NOTE: The mark allocation is shown against each of the three issues.

正确答案:

(b) Goodwill

(i) Matters

■ Cost of goodwill, $1·8 million, represents 3·4% consolidated total assets and is therefore material.

Tutorial note: Any assessments of materiality of goodwill against amounts in Aragon’s financial statements are

meaningless since goodwill only exists in the consolidated financial statements of Seymour.

■ It is correct that the goodwill is not being amortised (IFRS 3 Business Combinations). However, it should be tested

at least annually for impairment, by management.

■ Aragon has incurred losses amounting to $1·1 million since it was acquired (two years ago). The write-off of this

amount against goodwill in the consolidated financial statements would be material (being 61% cost of goodwill,

8·3% PBT and 2·1% total assets).

■ The cost of the investment ($4·5 million) in Seymour’s separate financial statements will also be material and

should be tested for impairment.

■ The fair value of net assets acquired was only $2·7 million ($4·5 million less $1·8 million). Therefore the fair

value less costs to sell of Aragon on other than a going concern basis will be less than the carrying amount of the

investment (i.e. the investment is impaired by at least the amount of goodwill recognised on acquisition).

■ In assessing recoverable amount, value in use (rather than fair value less costs to sell) is only relevant if the going

concern assumption is appropriate for Aragon.

■ Supporting Aragon financially may result in Seymour being exposed to actual and/or contingent liabilities that

should be provided for/disclosed in Seymour’s financial statements in accordance with IAS 37 Provisions,

Contingent Liabilities and Contingent Assets.

(ii) Audit evidence

■ Carrying values of cost of investment and goodwill arising on acquisition to prior year audit working papers and

financial statements.

■ A copy of Aragon’s draft financial statements for the year ended 30 September 2006 showing loss for year.

■ Management’s impairment test of Seymour’s investment in Aragon and of the goodwill arising on consolidation at

30 September 2006. That is a comparison of the present value of the future cash flows expected to be generated

by Aragon (a cash-generating unit) compared with the cost of the investment (in Seymour’s separate financial

statements).

■ Results of any impairment tests on Aragon’s assets extracted from Aragon’s working paper files.

■ Analytical procedures on future cash flows to confirm their reasonableness (e.g. by comparison with cash flows for

the last two years).

■ Bank report for audit purposes for any guarantees supporting Aragon’s loan facilities.

■ A copy of Seymour’s ‘comfort letter’ confirming continuing financial support of Aragon for the foreseeable future. -

第7题:

3 You are the manager responsible for the audit of Lamont Co. The company’s principal activity is wholesaling frozen

fish. The draft consolidated financial statements for the year ended 31 March 2007 show revenue of $67·0 million

(2006 – $62·3 million), profit before taxation of $11·9 million (2006 – $14·2 million) and total assets of

$48·0 million (2006 – $36·4 million).

The following issues arising during the final audit have been noted on a schedule of points for your attention:

(a) In early 2007 a chemical leakage from refrigeration units owned by Lamont caused contamination of some of its

property. Lamont has incurred $0·3 million in clean up costs, $0·6 million in modernisation of the units to

prevent future leakage and a $30,000 fine to a regulatory agency. Apart from the fine, which has been expensed,

these costs have been capitalised as improvements. (7 marks)

Required:

For each of the above issues:

(i) comment on the matters that you should consider; and

(ii) state the audit evidence that you should expect to find,

in undertaking your review of the audit working papers and financial statements of Lamont Co for the year ended

31 March 2007.

NOTE: The mark allocation is shown against each of the three issues.

正确答案:

3 LAMONT CO

(a) Chemical leakage

(i) Matters

■ $30,000 fine is very immaterial (just 1/4% profit before tax). This is revenue expenditure and it is correct that it

has been expensed to the income statement.

■ $0·3 million represents 0·6% total assets and 2·5% profit before tax and is not material on its own. $0·6 million

represents 1·2% total assets and 5% profit before tax and is therefore material to the financial statements.

■ The $0·3 million clean-up costs should not have been capitalised as the condition of the property is not improved

as compared with its condition before the leakage occurred. Although not material in isolation this amount should

be adjusted for and expensed, thereby reducing the aggregate of uncorrected misstatements.

■ It may be correct that $0·6 million incurred in modernising the refrigeration units should be capitalised as a major

overhaul (IAS 16 Property, Plant and Equipment). However, any parts scrapped as a result of the modernisation

should be treated as disposals (i.e. written off to the income statement).

■ The carrying amount of the refrigeration units at 31 March 2007, including the $0·6 million for modernisation,

should not exceed recoverable amount (i.e. the higher of value in use and fair value less costs to sell). If it does,

an allowance for the impairment loss arising must be recognised in accordance with IAS 36 Impairment of Assets.

(ii) Audit evidence

■ A breakdown/analysis of costs incurred on the clean-up and modernisation amounting to $0·3 million and

$0·6 million respectively.

■ Agreement of largest amounts to invoices from suppliers/consultants/sub-contractors, etc and settlement thereof

traced from the cash book to the bank statement.

■ Physical inspection of the refrigeration units to confirm their modernisation and that they are in working order. (Do

they contain frozen fish?)

■ Sample of components selected from the non-current asset register traced to the refrigeration units and inspected

to ensure continuing existence.

■ $30,000 penalty notice from the regulatory agency and corresponding cash book payment/payment per the bank

statement.

■ Written management representation that there are no further penalties that should be provided for or disclosed other

than the $30,000 that has been accounted for. -

第8题:

5 You are the manager responsible for the audit of Blod Co, a listed company, for the year ended 31 March 2008. Your

firm was appointed as auditors of Blod Co in September 2007. The audit work has been completed, and you are

reviewing the working papers in order to draft a report to those charged with governance. The statement of financial

position (balance sheet) shows total assets of $78 million (2007 – $66 million). The main business activity of Blod

Co is the manufacture of farm machinery.

During the audit of property, plant and equipment it was discovered that controls over capital expenditure transactions

had deteriorated during the year. Authorisation had not been gained for the purchase of office equipment with a cost

of $225,000. No material errors in the financial statements were revealed by audit procedures performed on property,

plant and equipment.

An internally generated brand name has been included in the statement of financial position (balance sheet) at a fair

value of $10 million. Audit working papers show that the matter was discussed with the financial controller, who

stated that the $10 million represents the present value of future cash flows estimated to be generated by the brand

name. The member of the audit team who completed the work programme on intangible assets has noted that this

treatment appears to be in breach of IAS 38 Intangible Assets, and that the management refuses to derecognise the

asset.

Problems were experienced in the audit of inventories. Due to an oversight by the internal auditors of Blod Co, the

external audit team did not receive a copy of inventory counting procedures prior to attending the count. This caused

a delay at the beginning of the inventory count, when the audit team had to quickly familiarise themselves with the

procedures. In addition, on the final audit, when the audit senior requested documentation to support the final

inventory valuation, it took two weeks for the information to be received because the accountant who had prepared

the schedules had mislaid them.

Required:

(a) (i) Identify the main purpose of including ‘findings from the audit’ (management letter points) in a report

to those charged with governance. (2 marks)

正确答案:

5 Blod Co

(a) (i) A report to those charged with governance is produced to communicate matters relating to the external audit to those

who are ultimately responsible for the financial statements. ISA 260 Communication of Audit Matters With Those

Charged With Governance requires the auditor to communicate many matters, including independence and other ethical

issues, the audit approach and scope, the details of management representations, and the findings of the audit. The

findings of the audit are commonly referred to as management letter points. By communicating these matters, the auditor

is confident that there is written documentation outlining all significant matters raised during the audit process, and that

such matters have been formally notified to the highest level of management of the client. For the management, the

report should ensure that they fully understand the scope and results of the audit service which has been provided, and

is likely to provide constructive comments to help them to fulfil their duties in relation to the financial statements and

accounting systems and controls more effectively. The report should also include, where relevant, any actions that

management has indicated they will take in relation to recommendations made by the auditors. -

第9题:

(a) The following information relates to Crosswire a publicly listed company.

Summarised statements of financial position as at:

The following information is available:

(i) During the year to 30 September 2009, Crosswire embarked on a replacement and expansion programme for its non-current assets. The details of this programme are:

On 1 October 2008 Crosswire acquired a platinum mine at a cost of $5 million. A condition of mining the

platinum is a requirement to landscape the mining site at the end of its estimated life of ten years. The

present value of this cost at the date of the purchase was calculated at $3 million (in addition to the

purchase price of the mine of $5 million).

Also on 1 October 2008 Crosswire revalued its freehold land for the first time. The credit in the revaluation

reserve is the net amount of the revaluation after a transfer to deferred tax on the gain. The tax rate applicable to Crosswire for deferred tax is 20% per annum.

On 1 April 2009 Crosswire took out a finance lease for some new plant. The fair value of the plant was

$10 million. The lease agreement provided for an initial payment on 1 April 2009 of $2·4 million followed

by eight six-monthly payments of $1·2 million commencing 30 September 2009.

Plant disposed of during the year had a carrying amount of $500,000 and was sold for $1·2 million. The

remaining movement on the property, plant and equipment, after charging depreciation of $3 million, was

the cost of replacing plant.

(ii) From 1 October 2008 to 31 March 2009 a further $500,000 was spent completing the development

project at which date marketing and production started. The sales of the new product proved disappointing

and on 30 September 2009 the development costs were written down to $1 million via an impairment

charge.

(iii) During the year ended 30 September 2009, $4 million of the 10% convertible loan notes matured. The

loan note holders had the option of redemption at par in cash or to exchange them for equity shares on the

basis of 20 new shares for each $100 of loan notes. 75% of the loan-note holders chose the equity option.

Ignore any effect of this on the other equity reserve.

All the above items have been treated correctly according to International Financial Reporting Standards.

(iv) The finance costs are made up of:

Required:

(i) Prepare a statement of the movements in the carrying amount of Crosswire’s non-current assets for the

year ended 30 September 2009; (9 marks)

(ii) Calculate the amounts that would appear under the headings of ‘cash flows from investing activities’

and ‘cash flows from financing activities’ in the statement of cash flows for Crosswire for the year ended

30 September 2009.

Note: Crosswire includes finance costs paid as a financing activity. (8 marks)

(b) A substantial shareholder has written to the directors of Crosswire expressing particular concern over the

deterioration of the company’s return on capital employed (ROCE)

Required:

Calculate Crosswire’s ROCE for the two years ended 30 September 2008 and 2009 and comment on the

apparent cause of its deterioration.

Note: ROCE should be taken as profit before interest on long-term borrowings and tax as a percentage of equity plus loan notes and finance lease obligations (at the year end). (8 marks)

正确答案:

(i)Thecashelementsoftheincreaseinproperty,plantandequipmentare$5millionforthemine(thecapitalisedenvironmentalprovisionisnotacashflow)and$2·4millionforthereplacementplantmakingatotalof$7·4million.(ii)Ofthe$4millionconvertibleloannotes(5,000–1,000)thatwereredeemedduringtheyear,75%($3million)ofthesewereexchangedforequitysharesonthebasisof20newsharesforeach$100inloannotes.Thiswouldcreate600,000(3,000/100x20)newsharesof$1eachandsharepremiumof$2·4million(3,000–600).As1million(5,000–4,000)newshareswereissuedintotal,400,000musthavebeenforcash.Theremainingincrease(aftertheeffectoftheconversion)inthesharepremiumof$1·6million(6,000–2,000b/f–2,400conversion)mustrelatetothecashissueofshares,thuscashproceedsfromtheissueofsharesis$2million(400nominalvalue+1,600premium).(iii)Theinitialleaseobligationis$10million(thefairvalueoftheplant).At30September2009totalleaseobligationsare$6·8million(5,040+1,760),thusrepaymentsintheyearwere$3·2million(10,000–6,800).(b)TakingthedefinitionofROCEfromthequestion:Fromtheaboveitcanbeclearlyseenthatthe2009operatingmarginhasimprovedbynearly1%point,despitethe$2millionimpairmentchargeonthewritedownofthedevelopmentproject.ThismeansthedeteriorationintheROCEisduetopoorerassetturnover.Thisimpliestherehasbeenadecreaseintheefficiencyintheuseofthecompany’sassetsthisyearcomparedtolastyear.Lookingatthemovementinthenon-currentassetsduringtheyearrevealssomemitigatingpoints:Thelandrevaluationhasincreasedthecarryingamountofproperty,plantandequipmentwithoutanyphysicalincreaseincapacity.Thisunfavourablydistortsthecurrentyear’sassetturnoverandROCEfigures.TheacquisitionoftheplatinummineappearstobeanewareaofoperationforCrosswirewhichmayhaveadifferent(perhapslower)ROCEtootherpreviousactivitiesoritmaybethatitwilltakesometimefortheminetocometofullproductioncapacity.Thesubstantialacquisitionoftheleasedplantwashalf-waythroughtheyearandcanonlyhavecontributedtotheyear’sresultsforsixmonthsatbest.Infutureperiodsafullyear’scontributioncanbeexpectedfromthisnewinvestmentinplantandthisshouldimprovebothassetturnoverandROCE.Insummary,thefallintheROCEmaybeduelargelytotheabovefactors(effectivelythereplacementandexpansionprogramme),ratherthantopooroperatingperformance,andinfutureperiodsthismaybereversed.ItshouldalsobenotedthathadtheROCEbeencalculatedontheaveragecapitalemployedduringtheyear(ratherthantheyearendcapitalemployed),whichisarguablymorecorrect,thenthedeteriorationintheROCEwouldnothavebeenaspronounced. -

第10题:

R1 has 5 working interfaces, with EIGRP neighbors existing off each interface. R1 has routes for subnets 10.1.1.0/24, 10.1.2.0/24, and 10.1.3.0/24, with EIGRP integer metrics of roughly 1 million, 2 million, a nd 3 million, respectively. An engineer then adds the ip summary - address eigrp 1 10.1.0.0 255.255.0.0 command to interface Fa0/0.Which of the following is true?()

A. R1 loses and then reestablishes neighborships with all neighbors.

B. R1 no longer advert ises 10.1.1.0/24 to neighbors connected to Fa0/0.

C. 1 advertises a 10.1.0.0/16 route out Fa0/0, with metric of around 3 million (largest metric of component subnets).

D. R1 advertises a 10.1.0.0/16 route out Fa0/0,with metric of around 2 million (med ian metric of component subnets).

参考答案:B

-

第11题:

单选题Mortgage and other financing income decreased $8.8 million to $18.8 for the year ended December 31, 2006.The income in 2006 was reducedAto $ 8.8 million.

Bto $18.8 million.

Cfrom $18.8 million to $8.8 million.

正确答案: A解析:

正确理解“decrease…”和“decrease to…”是本题解题的关键。前者的意思是“减少了…”,后者的意思是“减少到…”。根据原文可以知道“截止到2006年12月31日,抵押借款和其他融资收益减少了880万美元,是1880万美元”。所以,选项B正确。 -

第12题:

单选题How much loss will the shutdown cause the government in royalties and taxes in a week?AAbout $44.8 million.

BAbout $2.8 million.

CAbout $28 million.

DAbout $4.48 million.

正确答案: C解析:

数字信息的找寻和判断。录音中指出油田的关闭导致每天损失40万桶油,以目前的油价来计算,也就意味着“the state is losing about $6.4 million a day in royalties and taxes”,即“该州每天损失大概$6. 4 million(640万美元),那么一周下来就会损失44. 8 million。因此选项A为正确答案。 -

第13题:

(c) At 1 June 2006, Router held a 25% shareholding in a film distribution company, Wireless, a public limited

company. On 1 January 2007, Router sold a 15% holding in Wireless thus reducing its investment to a 10%

holding. Router no longer exercises significant influence over Wireless. Before the sale of the shares the net asset

value of Wireless on 1 January 2007 was $200 million and goodwill relating to the acquisition of Wireless was

$5 million. Router received $40 million for its sale of the 15% holding in Wireless. At 1 January 2007, the fair

value of the remaining investment in Wireless was $23 million and at 31 May 2007 the fair value was

$26 million. (6 marks)

Required:

Discuss how the above items should be dealt with in the group financial statements of Router for the year ended

31 May 2007.Required:

Discuss how the above items should be dealt with in the group financial statements of Router for the year ended

31 May 2007.

正确答案:

(c) The investment in Wireless is currently accounted for using the equity method of accounting under IAS28 ‘Investments in

Associates’. On the sale of a 15% holding, the investment in Wireless will be accounted for in accordance with IAS39. Router

should recognise a gain on the sale of the holding in Wireless of $7 million (Working 1). The gain comprises the following:

(i) the difference between the sale proceeds and the proportion of the net assets sold and

(ii) the goodwill disposed of.

The total gain is shown in the income statement.

The remaining 10 per cent investment will be classified as an ‘available for sale’ financial asset or at ‘fair value through profit

or loss’ financial asset. Changes in fair value for these categories are reported in equity or in the income statement respectively.

At 1 January 2007, the investment will be recorded at fair value and a gain of $1 million $(23 – 22) recorded. At 31 May

2007 a further gain of $(26 – 23) million, i.e. $3 million will be recorded. In order for the investment to be categorised as

at fair value through profit or loss, certain conditions have to be fulfilled. An entity may use this designation when doing so

results in more relevant information by eliminating or significantly reducing a measurement or recognition inconsistency (an

‘accounting mismatch’) or where a group of financial assets and/or financial liabilities is managed and its performance is

evaluated on a fair value basis, in accordance with a documented risk management or investment strategy, and information

about the assets and/ or liabilities is provided internally to the entity’s key management personnel.

-

第14题:

(c) On 1 May 2007 Sirus acquired another company, Marne plc. The directors of Marne, who were the only

shareholders, were offered an increased profit share in the enlarged business for a period of two years after the

date of acquisition as an incentive to accept the purchase offer. After this period, normal remuneration levels will

be resumed. Sirus estimated that this would cost them $5 million at 30 April 2008, and a further $6 million at

30 April 2009. These amounts will be paid in cash shortly after the respective year ends. (5 marks)

Required:

Draft a report to the directors of Sirus which discusses the principles and nature of the accounting treatment of

the above elements under International Financial Reporting Standards in the financial statements for the year

ended 30 April 2008.

正确答案:

(c) Acquisition of Marne

All business combinations within the scope of IFRS 3 ‘Business Combinations’ must be accounted for using the purchase

method. (IFRS 3.14) The pooling of interests method is prohibited. Under IFRS 3, an acquirer must be identified for all

business combinations. (IFRS 3.17) Sirus will be identified as the acquirer of Marne and must measure the cost of a business

combination at the sum of the fair values, at the date of exchange, of assets given, liabilities incurred or assumed, in exchange

for control of Marne; plus any costs directly attributable to the combination. (IFRS 3.24) If the cost is subject to adjustment

contingent on future events, the acquirer includes the amount of that adjustment in the cost of the combination at the

acquisition date if the adjustment is probable and can be measured reliably. (IFRS 3.32) However, if the contingent payment

either is not probable or cannot be measured reliably, it is not measured as part of the initial cost of the business combination.

If that adjustment subsequently becomes probable and can be measured reliably, the additional consideration is treated as

an adjustment to the cost of the combination. (IAS 3.34) The issue with the increased profit share payable to the directors

of Marne is whether the payment constitutes remuneration or consideration for the business acquired. Because the directors

of Marne fall back to normal remuneration levels after the two year period, it appears that this additional payment will

constitute part of the purchase consideration with the resultant increase in goodwill. It seems as though these payments can

be measured reliably and therefore the cost of the acquisition should be increased by the net present value of $11 million at

1 May 2007 being $5 million discounted for 1 year and $6 million for 2 years. -

第15题:

(c) During the year Albreda paid $0·1 million (2004 – $0·3 million) in fines and penalties relating to breaches of

health and safety regulations. These amounts have not been separately disclosed but included in cost of sales.

(5 marks)

Required:

For each of the above issues:

(i) comment on the matters that you should consider; and

(ii) state the audit evidence that you should expect to find,

in undertaking your review of the audit working papers and financial statements of Albreda Co for the year ended

30 September 2005.

NOTE: The mark allocation is shown against each of the three issues.

正确答案:

(c) Fines and penalties

(i) Matters

■ $0·1 million represents 5·6% of profit before tax and is therefore material. However, profit has fallen, and

compared with prior year profit it is less than 5%. So ‘borderline’ material in quantitative terms.

■ Prior year amount was three times as much and represented 13·6% of profit before tax.

■ Even though the payments may be regarded as material ‘by nature’ separate disclosure may not be necessary if,

for example, there are no external shareholders.

■ Treatment (inclusion in cost of sales) should be consistent with prior year (‘The Framework’/IAS 1 ‘Presentation of

Financial Statements’).

■ The reason for the fall in expense. For example, whether due to an improvement in meeting health and safety

regulations and/or incomplete recording of liabilities (understatement).

■ The reason(s) for the breaches. For example, Albreda may have had difficulty implementing new guidelines in

response to stricter regulations.

■ Whether expenditure has been adjusted for in the income tax computation (as disallowed for tax purposes).

■ Management’s attitude to health and safety issues (e.g. if it regards breaches as an acceptable operational practice

or cheaper than compliance).

■ Any references to health and safety issues in other information in documents containing audited financial

statements that might conflict with Albreda incurring these costs.

■ Any cost savings resulting from breaches of health and safety regulations would result in Albreda possessing

proceeds of its own crime which may be a money laundering offence.

(ii) Audit evidence

■ A schedule of amounts paid totalling $0·1 million with larger amounts being agreed to the cash book/bank

statements.

■ Review/comparison of current year schedule against prior year for any apparent omissions.

■ Review of after-date cash book payments and correspondence with relevant health and safety regulators (e.g. local

authorities) for liabilities incurred before 30 September 2005.

■ Notes in the prior year financial statements confirming consistency, or otherwise, of the lack of separate disclosure.

■ A ‘signed off’ review of ‘other information’ (i.e. directors’ report, chairman’s statement, etc).

■ Written management representation that there are no fines/penalties other than those which have been reflected in

the financial statements. -

第16题:

3 You are the manager responsible for the audit of Keffler Co, a private limited company engaged in the manufacture of

plastic products. The draft financial statements for the year ended 31 March 2006 show revenue of $47·4 million

(2005 – $43·9 million), profit before taxation of $2 million (2005 – $2·4 million) and total assets of $33·8 million

(2005 – $25·7 million).

The following issues arising during the final audit have been noted on a schedule of points for your attention:

(a) In April 2005, Keffler bought the right to use a landfill site for a period of 15 years for $1·1 million. Keffler

expects that the amount of waste that it will need to dump will increase annually and that the site will be

completely filled after just ten years. Keffler has charged the following amounts to the income statement for the

year to 31 March 2006:

– $20,000 licence amortisation calculated on a sum-of-digits basis to increase the charge over the useful life

of the site; and

– $100,000 annual provision for restoring the land in 15 years’ time. (9 marks)

Required:

For each of the above issues:

(i) comment on the matters that you should consider; and

(ii) state the audit evidence that you should expect to find,

in undertaking your review of the audit working papers and financial statements of Keffler Co for the year ended

31 March 2006.

NOTE: The mark allocation is shown against each of the three issues.

正确答案:

3 KEFFLER CO

Tutorial note: None of the issues have any bearing on revenue. Therefore any materiality calculations assessed on revenue are

inappropriate and will not be awarded marks.

(a) Landfill site

(i) Matters

■ $1·1m cost of the right represents 3·3% of total assets and is therefore material.

■ The right should be amortised over its useful life, that is just 10 years, rather than the 15-year period for which

the right has been granted.

Tutorial note: Recalculation on the stated basis (see audit evidence) shows that a 10-year amortisation has been

correctly used.

■ The amortisation charge represents 1% of profit before tax (PBT) and is not material.

■ The amortisation method used should reflect the pattern in which the future economic benefits of the right are

expected to be consumed by Keffler. If that pattern cannot be determined reliably, the straight-line method must

be used (IAS 38 ‘Intangible Assets’).

■ Using an increasing sum-of-digits will ‘end-load’ the amortisation charge (i.e. least charge in the first year, highest

charge in the last year). However, according to IAS 38 there is rarely, if ever, persuasive evidence to support an

amortisation method that results in accumulated amortisation lower than that under the straight-line method.

Tutorial note: Over the first half of the asset’s life, depreciation will be lower than under the straight-line basis

(and higher over the second half of the asset’s life).

■ On a straight line basis the annual amortisation charge would be $0·11m, an increase of $90,000. Although this

difference is just below materiality (4·5% PBT) the cumulative effect (of undercharging amortisation) will become

material.

■ Also, when account is taken of the understatement of cost (see below), the undercharging of amortisation will be

material.

■ The sum-of-digits method might be suitable as an approximation to the unit-of-production method if Keffler has

evidence to show that use of the landfill site will increase annually.

■ However, in the absence of such evidence, the audit opinion should be qualified ‘except for’ disagreement with the

amortisation method (resulting in intangible asset overstatement/amortisation expense understatement).

■ The annual restoration provision represents 5% of PBT and 0·3% of total assets. Although this is only borderline

material (in terms of profit), there will be a cumulative impact.

■ Annual provisioning is contrary to IAS 37 ‘Provisions, Contingent Liabilities and Contingent Assets’.

■ The estimate of the future restoration cost is (presumably) $1·5m (i.e. $0·1 × 15). The present value of this

amount should have been provided in full in the current year and included in the cost of the right.

■ Thus the amortisation being charged on the cost of the right (including the restoration cost) is currently understated

(on any basis).

Tutorial note: A 15-year discount factor at 10% (say) is 0·239. $1·5m × 0·239 is approximately $0·36m. The

resulting present value (of the future cost) would be added to the cost of the right. Amortisation over 10 years

on a straight-line basis would then be increased by $36,000, increasing the difference between amortisation

charged and that which should be charged. The lower the discount rate, the greater the understatement of

amortisation expense.

Total amount expensed ($120k) is less than what should have been expensed (say $146k amortisation + $36k

unwinding of discount). However, this is not material.

■ Whether Keffler will wait until the right is about to expire before restoring the land or might restore earlier (if the

site is completely filled in 10 years).

(ii) Audit evidence

■ Written agreement for purchase of right and contractual terms therein (e.g. to make restoration in 15 years’ time).

■ Cash book/bank statement entries in April 2005 for $1·1m payment.

■ Physical inspection of the landfill site to confirm Keffler’s use of it.

■ Annual dump budget/projection over next 10 years and comparison with sum-of-digits proportions.

■ Amount actually dumped in the year (per dump records) compared with budget and as a percentage/proportion of

the total available.

■ Recalculation of current year’s amortisation based on sum-of-digits. That is, $1·1m ÷ 55 = $20,000.

Tutorial note: The sum-of-digits from 1 to 10 may be calculated long-hand or using the formula n(n+1)/2 i.e.

(10 × 11)/2 = 55.

■ The basis of the calculation of the estimated restoration costs and principal assumptions made.

■ If estimated by a quantity surveyor/other expert then a copy of the expert’s report.

■ Written management representation confirming the planned timing of the restoration in 15 years (or sooner). -

第17题:

3 You are the manager responsible for the audit of Seymour Co. The company offers information, proprietary foods and

medical innovations designed to improve the quality of life. (Proprietary foods are marketed under and protected by

registered names.) The draft consolidated financial statements for the year ended 30 September 2006 show revenue

of $74·4 million (2005 – $69·2 million), profit before taxation of $13·2 million (2005 – $15·8 million) and total

assets of $53·3 million (2005 – $40·5 million).

The following issues arising during the final audit have been noted on a schedule of points for your attention:

(a) In 2001, Seymour had been awarded a 20-year patent on a new drug, Tournose, that was also approved for

food use. The drug had been developed at a cost of $4 million which is being amortised over the life of the

patent. The patent cost $11,600. In September 2006 a competitor announced the successful completion of

preliminary trials on an alternative drug with the same beneficial properties as Tournose. The alternative drug is

expected to be readily available in two years time. (7 marks)

Required:

For each of the above issues:

(i) comment on the matters that you should consider; and

(ii) state the audit evidence that you should expect to find,

in undertaking your review of the audit working papers and financial statements of Seymour Co for the year ended

30 September 2006.

NOTE: The mark allocation is shown against each of the three issues.

正确答案:

■ A change in the estimated useful life should be accounted for as a change in accounting estimate in accordance

with IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors. For example, if the development

costs have little, if any, useful life after the introduction of the alternative drug (‘worst case’ scenario), the carrying

value ($3 million) should be written off over the current and remaining years, i.e. $1 million p.a. The increase in

amortisation/decrease in carrying value ($800,000) is material to PBT (6%) and total assets (1·5%).

■ Similarly a change in the expected pattern of consumption of the future economic benefits should be accounted for

as a change in accounting estimate (IAS 8). For example, it may be that the useful life is still to 2020 but that

the economic benefits may reduce significantly in two years time.

■ After adjusting the carrying amount to take account of the change in accounting estimate(s) management should

have tested it for impairment and any impairment loss recognised in profit or loss.

(ii) Audit evidence

■ $3 million carrying amount of development costs brought forward agreed to prior year working papers and financial

statements.

■ A copy of the press release announcing the competitor’s alternative drug.

■ Management’s projections of future cashflows from Tournose-related sales as evidence of the useful life of the

development costs and pattern of consumption.

■ Reperformance of management’s impairment test on the development costs: Recalculation of management’s

calculation of the carrying amount after revising estimates of useful life and/or consumption of benefits compared

with management’s calculation of value in use.

■ Sensitivity analysis on management’s key assumptions (e.g. estimates of useful life, discount rate).

■ Written management representation on the key assumptions concerning the future that have a significant risk of

causing material adjustment to the carrying amount of the development costs. (These assumptions should be

disclosed in accordance with IAS 1 Presentation of Financial Statements.) -

第18题:

(c) In November 2006 Seymour announced the recall and discontinuation of a range of petcare products. The

product recall was prompted by the high level of customer returns due to claims of poor quality. For the year to

30 September 2006, the product range represented $8·9 million of consolidated revenue (2005 – $9·6 million)

and $1·3 million loss before tax (2005 – $0·4 million profit before tax). The results of the ‘petcare’ operations

are disclosed separately on the face of the income statement. (6 marks)

Required:

For each of the above issues:

(i) comment on the matters that you should consider; and

(ii) state the audit evidence that you should expect to find,

in undertaking your review of the audit working papers and financial statements of Seymour Co for the year ended

30 September 2006.

NOTE: The mark allocation is shown against each of the three issues.

正确答案:

■ The discontinuation of the product line after the balance sheet date provides additional evidence that, as at the

balance sheet date, it was of poor quality. Therefore, as at the balance sheet date:

– an allowance (‘provision’) may be required for credit notes for returns of products after the year end that were

sold before the year end;

– goods returned to inventory should be written down to net realisable value (may be nil);

– any plant and equipment used exclusively in the production of the petcare range of products should be tested

for impairment;

– any material contingent liabilities arising from legal claims should be disclosed.

(ii) Audit evidence

■ A copy of Seymour’s announcement (external ‘press release’ and any internal memorandum).

■ Credit notes raised/refunds paid after the year end for faulty products returned.

■ Condition of products returned as inspected during physical attendance of inventory count.

■ Correspondence from customers claiming reimbursement/compensation for poor quality.

■ Direct confirmation from legal adviser (solicitor) regarding any claims for customers including estimates of possible

payouts. -

第19题:

(b) You are the audit manager of Petrie Co, a private company, that retails kitchen utensils. The draft financial

statements for the year ended 31 March 2007 show revenue $42·2 million (2006 – $41·8 million), profit before

taxation of $1·8 million (2006 – $2·2 million) and total assets of $30·7 million (2006 – $23·4 million).

You are currently reviewing two matters that have been left for your attention on Petrie’s audit working paper file

for the year ended 31 March 2007:

(i) Petrie’s management board decided to revalue properties for the year ended 31 March 2007 that had

previously all been measured at depreciated cost. At the balance sheet date three properties had been

revalued by a total of $1·7 million. Another nine properties have since been revalued by $5·4 million. The

remaining three properties are expected to be revalued later in 2007. (5 marks)

Required:

Identify and comment on the implications of these two matters for your auditor’s report on the financial

statements of Petrie Co for the year ended 31 March 2007.

NOTE: The mark allocation is shown against each of the matters above.

正确答案:

(b) Implications for auditor’s report

(i) Selective revaluation of premises

The revaluations are clearly material to the balance sheet as $1·7 million and $5·4 million represent 5·5% and 17·6%

of total assets, respectively (and 23·1% in total). As the effects of the revaluation on line items in the financial statements

are clearly identified (e.g. revalued amount, depreciation, surplus in statement of changes in equity) the matter is not

pervasive.

The valuations of the nine properties after the year end provide additional evidence of conditions existing at the year end

and are therefore adjusting events per IAS 10 Events After the Balance Sheet Date.

Tutorial note: It is ‘now’ still less than three months after the year end so these valuations can reasonably be expected

to reflect year end values.

However, IAS 16 Property, Plant and Equipment does not permit the selective revaluation of assets thus the whole class

of premises would need to have been revalued for the year to 31 March 2007 to change the measurement basis for this

reporting period.

The revaluation exercise is incomplete. Unless the remaining three properties are revalued before the auditor’s report on

the financial statements for the year ended 31 March 2007 is signed off:

(1) the $7·1 revaluation made so far must be reversed to show all premises at depreciated cost as in previous years;

OR

(2) the auditor’s report would be qualified ‘except for’ disagreement regarding non-compliance with IAS 16.

When it is appropriate to adopt the revaluation model (e.g. next year) the change in accounting policy (from a cost model

to a revaluation model) should be accounted for in accordance with IAS 16 (i.e. as a revaluation).

Tutorial note: IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors does not apply to the initial

application of a policy to revalue assets in accordance with IAS 16.

Assuming the revaluation is written back, before giving an unmodified opinion, the auditor should consider why the three

properties were not revalued. In particular if there are any indicators of impairment (e.g. physical dilapidation) there

should be sufficient evidence on the working paper file to show that the carrying amount of these properties is not

materially greater than their recoverable amount (i.e. the higher of value in use and fair value less costs to sell).

If there is insufficient evidence to confirm that the three properties are not impaired (e.g. if the auditor was prevented

from inspecting the properties) the auditor’s report would be qualified ‘except for’ on grounds of limitation on scope.

If there is evidence of material impairment but management fail to write down the carrying amount to recoverable

amount the auditor’s report would be qualified ‘except for’ disagreement regarding non-compliance with IAS 36

Impairment of Assets.

-

第20题:

The following trial balance relates to Sandown at 30 September 2009:

The following notes are relevant:

(i) Sandown’s revenue includes $16 million for goods sold to Pending on 1 October 2008. The terms of the sale are that Sandown will incur ongoing service and support costs of $1·2 million per annum for three years after the sale. Sandown normally makes a gross profit of 40% on such servicing and support work. Ignore the time value of money.

(ii) Administrative expenses include an equity dividend of 4·8 cents per share paid during the year.

(iii) The 5% convertible loan note was issued for proceeds of $20 million on 1 October 2007. It has an effective interest rate of 8% due to the value of its conversion option.

(iv) During the year Sandown sold an available-for-sale investment for $11 million. At the date of sale it had a

carrying amount of $8·8 million and had originally cost $7 million. Sandown has recorded the disposal of the

investment. The remaining available-for-sale investments (the $26·5 million in the trial balance) have a fair value of $29 million at 30 September 2009. The other reserve in the trial balance represents the net increase in the value of the available-for-sale investments as at 1 October 2008. Ignore deferred tax on these transactions.

(v) The balance on current tax represents the under/over provision of the tax liability for the year ended 30 September 2008. The directors have estimated the provision for income tax for the year ended 30 September 2009 at $16·2 million. At 30 September 2009 the carrying amounts of Sandown’s net assets were $13 million in excess of their tax base. The income tax rate of Sandown is 30%.

(vi) Non-current assets:

The freehold property has a land element of $13 million. The building element is being depreciated on a

straight-line basis.

Plant and equipment is depreciated at 40% per annum using the reducing balance method.

Sandown’s brand in the trial balance relates to a product line that received bad publicity during the year which led to falling sales revenues. An impairment review was conducted on 1 April 2009 which concluded that, based on estimated future sales, the brand had a value in use of $12 million and a remaining life of only three years.

However, on the same date as the impairment review, Sandown received an offer to purchase the brand for

$15 million. Prior to the impairment review, it was being depreciated using the straight-line method over a

10-year life.

No depreciation/amortisation has yet been charged on any non-current asset for the year ended 30 September

2009. Depreciation, amortisation and impairment charges are all charged to cost of sales.

Required:

(a) Prepare the statement of comprehensive income for Sandown for the year ended 30 September 2009.

(13 marks)

(b) Prepare the statement of financial position of Sandown as at 30 September 2009. (12 marks)

Notes to the financial statements are not required.

A statement of changes in equity is not required.

正确答案:

(i)IAS18Revenuerequiresthatwheresalesrevenueincludesanamountforaftersalesservicingandsupportcoststhenaproportionoftherevenueshouldbedeferred.Theamountdeferredshouldcoverthecostandareasonableprofit(inthiscaseagrossprofitof40%)ontheservices.Astheservicingandsupportisforthreeyearsandthedateofthesalewas1October2008,revenuerelatingtotwoyears’servicingandsupportprovisionmustbedeferred:($1·2millionx2/0·6)=$4million.Thisisshownas$2millioninbothcurrentandnon-currentliabilities. -

第21题:

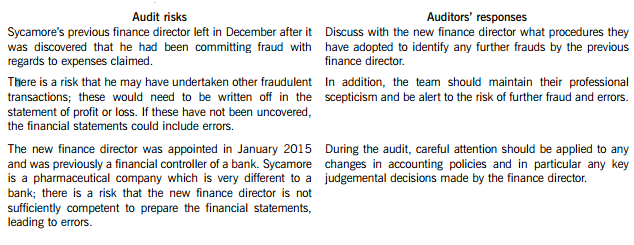

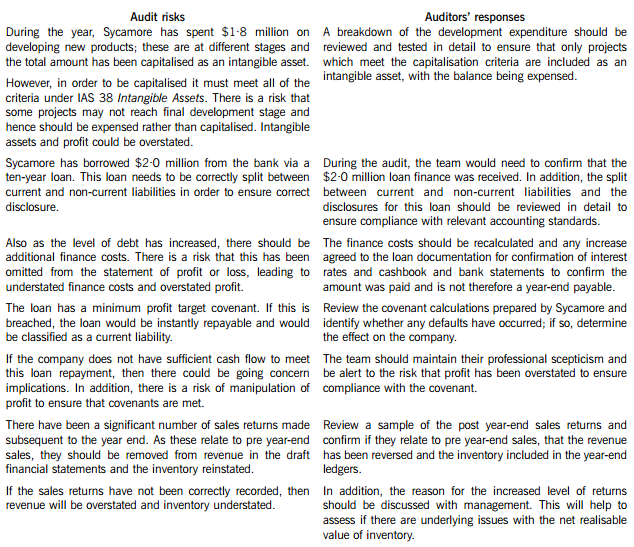

You are the audit supervisor of Maple & Co and are currently planning the audit of an existing client, Sycamore Science Co (Sycamore), whose year end was 30 April 2015. Sycamore is a pharmaceutical company, which manufactures and supplies a wide range of medical supplies. The draft financial statements show revenue of $35·6 million and profit before tax of $5·9 million.

Sycamore’s previous finance director left the company in December 2014 after it was discovered that he had been claiming fraudulent expenses from the company for a significant period of time. A new finance director was appointed in January 2015 who was previously a financial controller of a bank, and she has expressed surprise that Maple & Co had not uncovered the fraud during last year’s audit.

During the year Sycamore has spent $1·8 million on developing several new products. These projects are at different stages of development and the draft financial statements show the full amount of $1·8 million within intangible assets. In order to fund this development, $2·0 million was borrowed from the bank and is due for repayment over a ten-year period. The bank has attached minimum profit targets as part of the loan covenants.

The new finance director has informed the audit partner that since the year end there has been an increased number of sales returns and that in the month of May over $0·5 million of goods sold in April were returned.

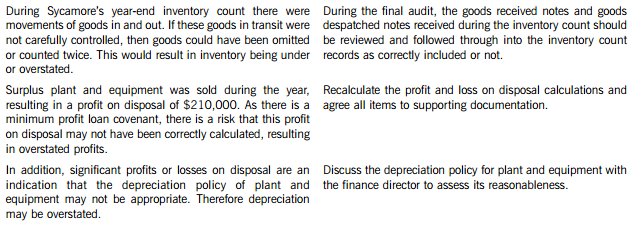

Maple & Co attended the year-end inventory count at Sycamore’s warehouse. The auditor present raised concerns that during the count there were movements of goods in and out the warehouse and this process did not seem well controlled.

During the year, a review of plant and equipment in the factory was undertaken and surplus plant was sold, resulting in a profit on disposal of $210,000.

Required:

(a) State Maples & Co’s responsibilities in relation to the prevention and detection of fraud and error. (4 marks)

(b) Describe SIX audit risks, and explain the auditor’s response to each risk, in planning the audit of Sycamore Science Co. (12 marks)

(c) Sycamore’s new finance director has read about review engagements and is interested in the possibility of Maple & Co undertaking these in the future. However, she is unsure how these engagements differ from an external audit and how much assurance would be gained from this type of engagement.

Required:

(i) Explain the purpose of review engagements and how these differ from external audits; and (2 marks)

(ii) Describe the level of assurance provided by external audits and review engagements. (2 marks)

正确答案:(a) Fraud responsibility

Maple & Co must conduct an audit in accordance with ISA 240 The Auditor’s Responsibilities Relating to Fraud in an Audit of Financial Statements and are responsible for obtaining reasonable assurance that the financial statements taken as a whole are free from material misstatement, whether caused by fraud or error.