(ii) If a partner, who is an actuary, provides valuation services to an audit client, can we continue with the audit?(3 marks)Required:For each of the three questions, explain the threats to objectivity that may arise and the safeguards thatshould be avai

题目

(ii) If a partner, who is an actuary, provides valuation services to an audit client, can we continue with the audit?

(3 marks)

Required:

For each of the three questions, explain the threats to objectivity that may arise and the safeguards that

should be available to manage them to an acceptable level.

NOTE: The mark allocation is shown against each of the three questions above.

相似考题

更多“(ii) If a partner, who is an actuary, provides valuation services to an audit client, can we continue with the audit?(3 marks)Required:For each of the three questions, explain the threats to objectivity that may arise and the safeguards thatshould be avai”相关问题

-

第1题:

(b) On 1 April 2004 Volcan introduced a ‘reward scheme’ for its customers. The main elements of the reward

scheme include the awarding of a ‘store point’ to customers’ loyalty cards for every $1 spent, with extra points

being given for the purchase of each week’s special offers. Customers who hold a loyalty card can convert their

points into cash discounts against future purchases on the basis of $1 per 100 points. (6 marks)

Required:

For each of the above issues:

(i) comment on the matters that you should consider; and

(ii) state the audit evidence that you should expect to find,

in undertaking your review of the audit working papers and financial statements of Volcan for the year ended

31 March 2005.

NOTE: The mark allocation is shown against each of the three issues.

正确答案:

(b) Reward scheme

(i) Matters

■ If the entire year’s revenue ($303m) attracted store points then the cost of the reward scheme in the year is at

most $3·03m. This represents 1% of revenue, which is material to the income statement and very material

(31·9%) to profit before tax (PBT).

■ The proportion of customers who register for loyalty cards and the percentage of revenue (and profit) which they

represent (which may vary from store to store depending on customer profile).

■ In accordance with the assumption of accruals, which underlies the preparation and presentation of financial

statements (The Framework/IAS 1 ‘Presentation of Financial Statements’), the expense and liability should be

recognised as revenue is earned. (It is of the nature of a discount.)

■ Any restrictions on the terms for converting points (e.g. whether they expire if not used within a specified time).

■ To the extent that points have been awarded but not redeemed at 31 March 2005, Volcan will have a liability at

the balance sheet date.

■ Agree the total balance due to customers at the year end under the reward scheme to the sum of the points on

individual customer reward cards.

■ The proportion of reward points awarded which are not expected to be claimed (e.g. the ‘take up’ of points awarded

may be only 80%, say).

■ Whether reward points are valued at selling price or cost. For example, if the average gross profit margin is 20%,

one point is equivalent to 0·8 cents of goods at cost.

(ii) Audit evidence

■ New/updated systems documentation explaining how:

– loyalty cards (and numbers) are issued to customers;

– points earned are recorded at the point of sale; and

– points are later redeemed on subsequent purchases.

■ Walk-through tests (e.g. on registering customer applications and issuing loyalty cards, awarding of points on

special offer items).

■ Tests of controls supporting the extent to which audit reliance is placed on the accounting and internal control

system. In particular, how points are extracted from the electronic tills (cash registers) and summarised into the

weekly/monthly financial data for each store which underlies the financial statements.

■ Analytical procedures on the value of points awarded by store per month with explanations of variations (‘variation

analysis’). For example, similar proportions (not exceeding 1% of revenue) of points in each month might be

expected by store – possibly increasing following any promotion of the ‘loyalty’ scheme.

Tutorial note: Within a close community, for example, a high proportion of customers might be expected to sign

up for the reward scheme. However, in big cities, where a large proportion of the customers might be transitory

(e.g. tourists or other visitors) the proportion may be much lower.

■ Tests of detail on a sample of transactions with customers undertaken at store visits. For example, for a sample of

copy till receipts:

– check the arithmetic accuracy of points awarded (1 per $1 spent + special offers);

– agree points awarded for special offers to that week’s special offers;

– for cash discounts taken confirm the conversion of points is against the opening balance of points awarded

(not against purchases just made). -

第2题:

(b) Identify and explain the financial statement risks to be taken into account in planning the final audit.

(12 marks)

正确答案:

(b) Financial statement risks

Tutorial note: Note the timeframe. Financial statements for the year to 30 June 2006 are draft. Certain misstatements

may therefore exist due to year-end procedures not yet having taken place.

Revenue/(Receivables)

■ Revenue has increased by 11·8% ((161·5 – 144·4)/144·4 × 100). Overstatement could arise if rebates due to customers

have not yet been accounted for in full (as they are calculated in arrears). If rebates have still to be accounted for trade

receivables will be similarly overstated.

Materials expense

■ Materials expense has increased by 17·8% ((88.0 – 74·7)/74·7 × 100). This is more than the increase in revenue. This

could be legitimate (e.g. if fuel costs have increased significantly). However, the increase could indicate misclassification

of:

– revenue expenditure (see fall in other expenses below);

– capital expenditure (e.g. on overhauls or major refurbishment) as revenue;

– finance lease payments as operating lease.

Depreciation/amortisation

■ This has fallen by 10·5% ((8·5 – 9·5)/9·5 × 100). This could be valid (e.g. if Yates has significant assets already fully

depreciated or the asset base is lower since last year’s restructuring). However, there is a risk of understatement if, for

example:

– not all assets have been depreciated (or depreciated at the wrong rates, or only for 11 months of the year);

– cost of non-current assets is understated (e.g. due to failure to recognise capital expenditure)1;

– impairment losses have not been recognised (as compared with the prior year).

Tutorial note: Depreciation on vehicles and transport equipment represents only 7% of cost. If all items were being

depreciated on a straight-line basis over eight years this should be 12·5%. The depreciation on other equipment looks more

reasonable as it amounts to 14% which would be consistent with an average age of vehicles of seven years (i.e. in the middle

of the range 3 – 13 years).

Other expenses

■ These have fallen by 15·5% ((19·6 – 23·2)/23·2 × 100). They may have fallen (e.g. following the restructuring) or may be

understated due to:

– expenses being misclassified as materials expense;

– underestimation of accrued expenses (especially as the financial reporting period has not yet expired).

Intangibles

■ Intangible assets have increased by $1m (16% on the prior year). Although this may only just be material to the

financial statements as a whole (see (a)) this is the net movement, therefore additions could be material.

■ Internally-generated intangibles will be overstated if:

– any of the IAS 38 recognition criteria cannot be demonstrated;

– any impairment in the year has not yet been written off in accordance with IAS 36 ‘Impairment of Assets’.

Tangible assets

■ The net book value of property (at cost) has fallen by 5%, vehicles are virtually unchanged (increased by just 2·5%)

and other equipment (though the least material category) has fallen by 20·4%.

■ Vehicles and equipment may be overstated if:

– disposals have not been recorded;

– depreciation has been undercharged (e.g. not for a whole year);

– impairments have not yet been accounted for.

■ Understatement will arise if finance leases are treated as operating leases.

Receivables

■ Trade receivables have increased by just 2·2% (although sales increased by 11·8%) and may be understated due to a

cutoff error resulting in overstatement of cash receipts.

■ There is a risk of overstatement if sufficient allowances have not been made for the impairment of individually significant

balances and for the remainder assessed on a portfolio or group basis.

Restructuring provision

■ The restructuring provision that was made last year has fallen/been utilised by 10·2%. There is a risk of overstatement

if the provision is underutilised/not needed for the purpose for which it was established.

Finance lease liabilities

■ Although finance lease liabilities have increased (by $1m) there is a greater risk of understatement than overstatement

if leased assets are not recognised on the balance sheet (i.e. capitalised).

■ Disclosure risk arises if the requirements of IAS 17 ‘Leases’ (e.g. in respect of minimum lease payments) are not met.

Trade payables

■ These have increased by only 5·3% compared with the 17·8% increase in materials expense. There is a risk of

understatement as notifications (e.g. suppliers’ invoices) of liabilities outstanding at 30 June 2006 may have still to be

received (the month of June being an unexpired period).

Other (employee) liabilities

■ These may be understated as they have increased by only 7·5% although staff costs have increased by 14%. For

example, balances owing in respect of outstanding holiday entitlements at the year end may not yet be accurately

estimated.

Tutorial note: Credit will be given to other financial statements risks specific to the scenario. For example, ‘time-sensitive

delivery schedules’ might give rise to penalties or claims, that could result in understated provisions or undisclosed

contingent liabilities. Also, given that this is a new audit and the result has changed significantly (from loss to profit) might

suggest a risk of misstatement in the opening balances (and hence comparative information).

1 Tutorial note: This may be unlikely as other expenses have fallen also. -

第3题:

(b) A sale of industrial equipment to Deakin Co in May 2005 resulted in a loss on disposal of $0·3 million that has

been separately disclosed on the face of the income statement. The equipment cost $1·2 million when it was

purchased in April 1996 and was being depreciated on a straight-line basis over 20 years. (6 marks)

Required:

For each of the above issues:

(i) comment on the matters that you should consider; and

(ii) state the audit evidence that you should expect to find,

in undertaking your review of the audit working papers and financial statements of Keffler Co for the year ended

31 March 2006.

NOTE: The mark allocation is shown against each of the three issues.

正确答案:

(b) Sale of industrial equipment

(i) Matters

■ The industrial equipment was in use for nine years (from April 1996) and would have had a carrying value of

$660,000 at 31 March 2005 (11/20 × $1·2m – assuming nil residual value and a full year’s depreciation charge

in the year of acquisition and none in the year of disposal). Disposal proceeds were therefore only $360,000.

■ The $0·3m loss represents 15% of PBT (for the year to 31 March 2006) and is therefore material. The equipment

was material to the balance sheet at 31 March 2005 representing 2·6% of total assets ($0·66/$25·7 × 100).

■ Separate disclosure, of a material loss on disposal, on the face of the income statement is in accordance with

IAS 16 ‘Property, Plant and Equipment’. However, in accordance with IAS 1 ‘Presentation of Financial Statements’,

it should not be captioned in any way that might suggest that it is not part of normal operating activities (i.e. not

‘extraordinary’, ‘exceptional’, etc).

Tutorial note: However, note that if there is a prior period error to be accounted for (see later), there would be

no impact on the current period income statement requiring consideration of any disclosure.

■ The reason for the sale. For example, whether the equipment was:

– surplus to operating requirements (i.e. not being replaced); or

– being replaced with newer equipment (thereby contributing to the $8·1m increase (33·8 – 25·7) in total

assets).

■ The reason for the loss on sale. For example, whether:

– the sale was at an under-value (e.g. to a related party);

– the equipment had a bad maintenance history (or was otherwise impaired);

– the useful life of the equipment is less than 20 years;

– there is any deferred consideration not yet recorded;

– any non-cash disposal proceeds have been overlooked (e.g. if another asset was acquired in a part-exchange).

■ If the useful life was less than 20 years, tangible non-current assets may be materially overstated in respect of other

items of equipment that are still in use and being depreciated on the same basis.

■ If the sale was to a related party then additional disclosure should be required in a note to the financial statements

for the year to 31 March 2006 (IAS 24 ‘Related Party Disclosures’).

Tutorial note: Since there are no specific pointers to a related party transaction (RPT), this point is not expanded

on.

■ Whether the sale was identified in the prior year audit’s post balance sheet event review. If so:

– the disclosure made in the prior year’s financial statements (IAS 10 ‘Events After the Balance Sheet Date’);

– whether an impairment loss was recognised at 31 March 2005.

■ If not, and the equipment was impaired at 31 March 2005, a prior period error should be accounted for (IAS 8

‘Accounting Policies, Changes in Accounting Estimates and Errors’). An impairment loss of $0·3m would have

been material to prior year profit (12·5%).

Tutorial note: Unless this was a RPT or the impairment arose after 31 March 2005 a prior period adjustment

should be made.

■ Failure to account for a prior period error (if any) would result in modification of the audit opinion ‘except for’ noncompliance

with IAS 8 (in the current year) and IAS 36 (in the prior period).

(ii) Audit evidence

■ Carrying amount ($0·66m as above) agreed to the non-current asset register balances at 31 March 2005 and

recalculation of the loss on disposal.

■ Cost and accumulated depreciation removed from the asset register in the year to 31 March 2006.

■ Receipt of proceeds per cash book agreed to bank statement.

■ Sales invoice transferring title to Deakin.

■ A review of maintenance expenses and records (e.g. to confirm reason for loss on sale).

■ Post balance sheet event review on prior year audit working papers file.

■ Management representation confirming that Deakin is not a related party (provided that there is no evidence to

suggest otherwise). -

第4题:

5 You are an audit manager in Fox & Steeple, a firm of Chartered Certified Accountants, responsible for allocating staff

to the following three audits of financial statements for the year ending 31 December 2006:

(a) Blythe Co is a new audit client. This private company is a local manufacturer and distributor of sportswear. The

company’s finance director, Peter, sees little value in the audit and put it out to tender last year as a cost-cutting

exercise. In accordance with the requirements of the invitation to tender your firm indicated that there would not

be an interim audit.

(b) Huggins Co, a long-standing client, operates a national supermarket chain. Your firm provided Huggins Co with

corporate financial advice on obtaining a listing on a recognised stock exchange in 2005. Senior management

expects a thorough examination of the company’s computerised systems, and are also seeking assurance that

the annual report will not attract adverse criticism.

(c) Gray Co has been an audit client since 1999 after your firm advised management on a successful buyout. Gray

provides communication services and software solutions. Your firm provides Gray with technical advice on

financial reporting and tax services. Most recently you have been asked to conduct due diligence reviews on

potential acquisitions.

Required:

For these assignments, compare and contrast:

(i) the threats to independence;

(ii) the other professional and practical matters that arise; and

(iii) the implications for allocating staff.

(15 marks)

正确答案:

5 FOX & STEEPLE – THREE AUDIT ASSIGNMENTS

(i) Threats to independence

Self-interest

Tutorial note: This threat arises when a firm or a member of the audit team could benefit from a financial interest in, or

other self-interest conflict with, an assurance client.

■ A self-interest threat could potentially arise in respect of any (or all) of these assignments as, regardless of any fee

restrictions (e.g. per IFAC’s ‘Code of Ethics for Professional Accountants’), the auditor is remunerated by clients for

services provided.

■ This threat is likely to be greater for Huggins Co (larger/listed) and Gray Co (requires other services) than for Blythe Co

(audit a statutory necessity).

■ The self-interest threat may be greatest for Huggins Co. As a company listed on a recognised stock exchange it may

give prestige and credibility to Fox & Steeple (though this may be reciprocated). Fox & Steeple could be pressurised into

taking evasive action to avoid the loss of a listed client (e.g. concurring with an inappropriate accounting treatment).

Self-review

Tutorial note: This arises when, for example, any product or judgment of a previous engagement needs to be re-evaluated

in reaching conclusions on the audit engagement.

■ This threat is also likely to be greater for Huggins and Gray where Fox & Steeple is providing other (non-audit) services.

■ A self-review threat may be created by Fox & Steeple providing Huggins with a ‘thorough examination’ of its computerised

systems if it involves an extension of the procedures required to conduct an audit in accordance with International

Standards on Auditing (ISAs).

■ Appropriate safeguards must be put in place if Fox & Steeple assists Huggins in the performance of internal audit

activities. In particular, Fox & Steeple’s personnel must not act (or appear to act) in a capacity equivalent to a member

of Huggins’ management (e.g. reporting, in a management role, to those charged with governance).

■ Fox & Steeple may provide Gray with accounting and bookkeeping services, as Gray is not a listed entity, provided that

any self-review threat created is reduced to an acceptable level. In particular, in giving technical advice on financial

reporting, Fox & Steeple must take care not to make managerial decisions such as determining or changing journal

entries without obtaining Gray’s approval.

■ Taxation services comprise a broad range of services, including compliance, planning, provision of formal taxation

opinions and assistance in the resolution of tax disputes. Such assignments are generally not seen to create threats to

independence.

Tutorial note: It is assumed that the provision of tax services is permitted in the jurisdiction (i.e. that Fox and Steeple

are not providing such services if prohibited).

■ The due diligence reviews for Gray may create a self-review threat (e.g. on the fair valuation of net assets acquired).

However, safeguards may be available to reduce these threats to an acceptable level.

■ If staff involved in providing other services are also assigned to the audit, their work should be reviewed by more senior

staff not involved in the provision of the other services (to the extent that the other service is relevant to the audit).

■ The reporting lines of any staff involved in the audit of Huggins and the provision of other services for Huggins should

be different. (Similarly for Gray.)

Familiarity

Tutorial note: This arises when, by virtue of a close relationship with an audit client (or its management or employees) an

audit firm (or a member of the audit team) becomes too sympathetic to the client’s interests.

■ Long association of a senior member of an audit team with an audit client may create a familiarity threat. This threat

is likely to be greatest for Huggins, a long-standing client. It may also be significant for Gray as Fox & Steeple have had

dealings with this client for seven years now.

■ As Blythe is a new audit client this particular threat does not appear to be relevant.

■ Senior personnel should be rotated off the Huggins and Gray audit teams. If this is not possible (for either client), an

additional professional accountant who was not a member of the audit team should be required to independently review

the work done by the senior personnel.

■ The familiarity threat of using the same lead engagement partner on an audit over a prolonged period is particularly

relevant to Huggins, which is now a listed entity. IFAC’s ‘Code of Ethics for Professional Accountants’ requires that the

lead engagement partner should be rotated after a pre-defined period, normally no more than seven years. Although it

might be time for the lead engagement partner of Huggins to be changed, the current lead engagement partner may

continue to serve for the 2006 audit.

Tutorial note: Two additional years are permitted when an existing client becomes listed, since it may not be in the

client’s best interests to have an immediate rotation of engagement partner.

Intimidation

Tutorial note: This arises when a member of the audit team may be deterred from acting objectively and exercising

professional skepticism by threat (actual or perceived), from the audit client.

■ This threat is most likely to come from Blythe as auditors are threatened with a tendering process to keep fees down.

■ Peter may have already applied pressure to reduce inappropriately the extent of audit work performed in order to reduce

fees, by stipulating that there should not be an interim audit.

■ The audit senior allocated to Blythe will need to be experienced in standing up to client management personnel such as

Peter.

Tutorial note: ‘Correct’ classification under ‘ethical’, ‘other professional’, ‘practical’ or ‘staff implications’ is not as important

as identifying the matters.

(ii) Other professional and practical matters

Tutorial note: ‘Other professional’ includes quality control.

■ The experience of staff allocated to each assignment should be commensurate with the assessment of associated risk.

For example, there may be a risk that insufficient audit evidence is obtained within the budget for the audit of Blythe.

Huggins, as a listed client, carries a high reputational risk.

■ Sufficient appropriate staff should be allocated to each audit to ensure adequate quality control (in particular in the

direction, supervision, review of each assignment). It may be appropriate for a second partner to be assigned to carry

out a ‘hot review’ (before the auditor’s report is signed) of:

– Blythe, because it is the first audit of a new client; and

– Huggins, as it is listed.

■ Existing clients (Huggins and Gray) may already have some expectation regarding who should be assigned to their

audits. There is no reason why there should not be some continuity of staff providing appropriate safeguards are put in

place (e.g. to overcome any familiarity threat).

■ Senior staff assigned to Blythe should be alerted to the need to exercise a high degree of professional skepticism (in the

light of Peter’s attitude towards the audit).

■ New staff assigned to Huggins and Gray would perhaps be less likely to assume unquestioned honesty than staff

previously involved with these audits.

Logistics (practical)

■ All three assignments have the same financial year end, therefore there will be an element of ‘competition’ for the staff

to be assigned to the year-end visits and final audit assignments. As a listed company, Huggins is likely to have the

tightest reporting deadline and so have a ‘priority’ for staff.

■ Blythe is a local and private company. Staff involved in the year-end visit (e.g. to attend the physical inventory count)

should also be involved in the final audit. As this is a new client, staff assigned to this audit should get involved at every

stage to increase their knowledge and understanding of the business.

■ Huggins is a national operation and may require numerous staff to attend year-end procedures. It would not be expected

that all staff assigned to year-end visits should all be involved in the final audit.

Time/fee/staff budgets

■ Time budgets will need to be prepared for each assignment to determine manpower requirements (and to schedule audit

work).

(iii) Implications for allocating staff

■ Fox & Steeple should allocate staff so that those providing other services to Huggins and Gray (that may create a selfreview

threat) do not participate in the audit engagement.

Competence and due care (Qualifications/Specialisation)

■ All audit assignments will require competent staff.

■ Huggins will require staff with an in-depth knowledge of their computerised system.

■ Gray will require senior audit staff to be experienced in financial reporting matters specific to communications and

software solutions (e.g. in revenue recognition issues and accounting for internally-generated intangible assets).

■ Specialists providing tax services and undertaking the due diligence reviews for Gray may not be required to have any

involvement in the audit assignment. -

第5题:

(ii) Briefly explain the implications of Parr & Co’s audit opinion for your audit opinion on the consolidated

financial statements of Cleeves Co for the year ended 30 September 2006. (3 marks)

正确答案:

(ii) Implications for audit opinion on consolidated financial statements of Cleeves

■ If the potential adjustments to non-current asset carrying amounts and loss are not material to the consolidated

financial statements there will be no implication. However, as Howard is material to Cleeves and the modification

appears to be ‘so material’ (giving rise to adverse opinion) this seems unlikely.

Tutorial note: The question clearly states that Howard is material to Cleeves, thus there is no call for speculation

on this.

■ As Howard is wholly-owned the management of Cleeves must be able to request that Howard’s financial statements

are adjusted to reflect the impairment of the assets. The auditor’s report on Cleeves will then be unmodified

(assuming that any impairment of the investment in Howard is properly accounted for in the separate financial

statements of Cleeves).

■ If the impairment losses are not recognised in Howard’s financial statements they can nevertheless be adjusted on

consolidation of Cleeves and its subsidiaries (by writing down assets to recoverable amounts). The audit opinion

on Cleeves should then be unmodified in this respect.

■ If there is no adjustment of Howard’s asset values (either in Howard’s financial statements or on consolidation) it

is most likely that the audit opinion on Cleeves’s consolidated financial statements would be ‘except for’. (It should

not be adverse as it is doubtful whether even the opinion on Howard’s financial statements should be adverse.)

Tutorial note: There is currently no requirement in ISA 600 to disclose that components have been audited by another

auditor unless the principal auditor is permitted to base their opinion solely upon the report of another auditor. -

第6题:

(ii) Can we entertain our clients as a gesture of goodwill or is corporate hospitality ruled out? (3 marks)

Required:

For EACH of the three FAQs, explain the threats to objectivity that may arise and the safeguards that should

be available to manage them to an acceptable level.

NOTE: The mark allocation is shown against each of the three questions.

正确答案:

(ii) Corporate hospitality

A partner in an audit firm is obviously in a position to influence the conduct and outcome of an audit. Therefore a

partner being on ‘too friendly’ terms with an audit client creates a familiarity threat. Other members of the audit team

may not exert as much influence on the audit.

A self-interest threat may also be perceived (e.g. if corporate hospitality is provided to keep a prestigious client).

There is no absolute prohibition against corporate hospitality provided:

■ the value attached to such hospitality is ‘insignificant’; and

■ the ‘frequency, nature and cost’ of the hospitality is reasonable.

Thus, flying the directors of an audit client for weekends away could be seen as significant. Similarly, entertaining an

audit client on a regular basis could be seen as unacceptable.

Partners and staff of Boleyn will need to be objective in their assessments of the significance or reasonableness of the

hospitality offered. (Would ‘a reasonable and informed third party’ conclude that the hospitality will or is likely to be

seen to impair your objectivity?)

If they have any doubts they should discuss the matter in the first instance with the audit engagement partner, who

should refer the matter to the ethics partner if in doubt. -

第7题:

(c) Lamont owns a residential apartment above its head office. Until 31 December 2006 it was let for $3,000 a

month. Since 1 January 2007 it has been occupied rent-free by the senior sales executive. (6 marks)

Required:

For each of the above issues:

(i) comment on the matters that you should consider; and

(ii) state the audit evidence that you should expect to find,

in undertaking your review of the audit working papers and financial statements of Lamont Co for the year ended

31 March 2007.

NOTE: The mark allocation is shown against each of the three issues.

正确答案:

(c) Rent-free accommodation

(i) Matters

■ The senior sales executive is a member of Lamont’s key management personnel and is therefore a related party.

■ The occupation of Lamont’s residential apartment by the senior sales executive is therefore a related party

transaction, even though no price is charged (IAS 24 Related Party Disclosures).

■ Related party transactions are material by nature and information about them should be disclosed so that users of

financial statements understand the potential effect of related party relationships on the financial statements.

■ The provision of ‘housing’ is a non-monetary benefit that should be included in the disclosure of key management

personnel compensation (within the category of short-term employee benefits).

■ The financial statements for the year ended 31 March 2007 should disclose the arrangement for providing the

senior sales executive with rent-free accommodation and its fair value (i.e. $3,000 per month).

Tutorial note: Since no price is charged for the transaction, rote-learned disclosures such as ‘the amount of outstanding

balances’ and ‘expense recognised in respect of bad debts’ are irrelevant.

(ii) Audit evidence

■ Physical inspection of the apartment to confirm that it is occupied.

■ Written representation from the senior sales executive that he is occupying the apartment free of charge.

■ Written representation from the management board confirming that there are no related party transactions requiring

disclosure other than those that have been disclosed.

■ Inspection of the lease agreement with (or payments received from) the previous tenant to confirm the $3,000

monthly rental value. -

第8题:

(iii) Can internal audit services be undertaken for an audit client? (4 marks)

Required:

For each of the three questions, explain the threats to objectivity that may arise and the safeguards that

should be available to manage them to an acceptable level.

NOTE: The mark allocation is shown against each of the three questions above.

正确答案:(iii) Internal audit services

A self-review threat may be created when a firm, or network firm, provides internal audit services to a financial statement

audit client. Internal audit services may comprise:

■ an extension of the firm’s audit service beyond requirements of International Standards on Auditing (ISAs);

■ assistance in the performance of a client’s internal audit activities; or

■ outsourcing of the activities.

The nature of the service must be considered in evaluating any threats to independence. (For this purpose, internal audit

services do not include operational internal audit services unrelated to the internal accounting controls, financial systems

or financial statements.)

Services involving an extension of the procedures required to conduct a financial statement audit in accordance with

ISAs would not be considered to impair independence with respect to the audit client provided that the firm’s or network

firm’s personnel do not act or appear to act in a capacity equivalent to a member of audit client management.When the firm, or a network firm, provides an audit client with assistance in the performance of internal audit activities

or undertakes the outsourcing, any self-review threat created may be reduced to an acceptable level by a clear separation

of:

■ the management and control of the internal audit by client management;

■ the internal audit activities.

Performing a significant portion of an audit client’s internal audit activities may create a self-review threat. Appropriate

safeguards should include the audit client’s acknowledgement of its responsibilities for establishing, maintaining and

monitoring the system of internal controls.

Other safeguards include:

■ the audit client designating a competent employee, preferably within senior management, to be responsible for

internal audit activities;

■ the audit client, audit committee or supervisory body approving the scope, risk and frequency of internal audit

work;

■ the audit client being responsible for evaluating and determining which recommendations of the firm should be

implemented;

■ the audit client evaluating the adequacy of the internal audit procedures performed and the resultant findings by

obtaining and acting on reports from the firm; and

■ appropriate reporting of findings and recommendations resulting from the internal audit activities to the audit

committee or supervisory body.

Consideration should also be given to whether such non-assurance services should be provided only by personnel not

involved in the financial statement audit engagement and with different reporting lines within the firm. -

第9题:

4 You are an audit manager in Nate & Co, a firm of Chartered Certified Accountants. You are reviewing three situations,

which were recently discussed at the monthly audit managers’ meeting:

(1) Nate & Co has recently been approached by a potential new audit client, Fisher Co. Your firm is keen to take the

appointment and is currently carrying out client acceptance procedures. Fisher Co was recently incorporated by

Marcellus Fisher, with its main trade being the retailing of wooden storage boxes.

(2) Nate & Co provides the audit service to CF Co, a national financial services organisation. Due to a number of

errors in the recording of cash deposits from new customers that have been discovered by CF Co’s internal audit

team, the directors of CF Co have requested that your firm carry out a review of the financial information

technology systems. It has come to your attention that while working on the audit planning of CF Co, Jin Sayed,

one of the juniors on the audit team, who is a recent information technology graduate, spent three hours

providing advice to the internal audit team about how to improve the system. As far as you know, this advice has

not been used by the internal audit team.

(3) LA Shots Co is a manufacturer of bottled drinks, and has been an audit client of Nate & Co for five years. Two

audit juniors attended the annual inventory count last Monday. They reported that Brenda Mangle, the new

production manager of LA Shots Co, wanted the inventory count and audit procedures performed as quickly as

possible. As an incentive she offered the two juniors ten free bottles of ‘Super Juice’ from the end of the

production line. Brenda also invited them to join the LA Shots Co office party, which commenced at the end of

the inventory count. The inventory count and audit procedures were completed within two hours (the previous

year’s procedures lasted a full day), and the juniors then spent four hours at the office party.

Required:

(a) Define ‘money laundering’ and state the procedures specific to money laundering that should be considered

before, and on the acceptance of, the audit appointment of Fisher Co. (5 marks)

正确答案:

4 NATE & CO

(a) – Money laundering is the process by which criminals attempt to conceal the true origin and ownership of the proceeds

of criminal activity, allowing them to maintain control over the proceeds, and ultimately providing a legitimate cover for

their sources of income. The objective of money laundering is to break the connection between the money, and the crime

that it resulted from.

– It is widely defined, to include possession of, or concealment of, the proceeds of any crime.

– Examples include proceeds of fraud, tax evasion and benefits of bribery and corruption.

Client procedures should include the following:

– Client identification:

? Establish the identity of the entity and its business activity e.g. by obtaining a certificate of incorporation

? If the client is an individual, obtain official documentation including a name and address, e.g. by looking at

photographic identification such as passports and driving licences

? Consider whether the commercial activity makes business sense (i.e. it is not just a ‘front’ for illegal activities)

? Obtain evidence of the company’s registered address e.g. by obtaining headed letter paper

? Establish the current list of principal shareholders and directors.

– Client understanding:

? Pre-engagement communication may be considered, to explain to Marcellus Fisher and the other directors the

nature and reason for client acceptance procedures.

? Best practice recommends that the engagement letter should also include a paragraph outlining the auditor’s

responsibilities in relation to money laundering. -

第10题:

(ii) Recommend further audit procedures that should be carried out. (4 marks)

正确答案:

(ii) Further audit procedures:

Request from Peter Sheffield a written representation detailing:

– the exact nature of his control over Jarvis Co, i.e. if he is a shareholder then state his percentage shareholding, if

he is a member of senior management then state his exact position within the entity,

– a comment on whether in his opinion the balance is recoverable,

– a specific date by which the amount should be expected to be repaid, and

– a confirmation that there are no further balances outstanding from Jarvis Co, or any further transactions between

Jarvis Co and Pulp Co.

Tutorial note: Reference to the Exposure Draft ISA 550 Related Parties (Revised and Redrafted) requirement for both

general and specific management representations will be awarded credit.

Review the terms of any written confirmation of the amount, such as a signed agreement or invoice, checking whether

any interest is due to Pulp Co. The terms should be reviewed for details of any security offered, and the nature of the

consideration to be provided in settlement.

From discussion with Peter Sheffield, develop an understanding of the business purpose of the transaction, particularly

to understand whether the balance is a trade receivable or an investment.

Review the board minutes for evidence of any discussion of the transaction and the recoverability of the balance

outstanding.

Obtain the most recent audited financial statements of Jarvis Co and:

– ascertain whether Peter Sheffield is disclosed as the ultimate controlling party or disclosed as a member of key

management personnel,

– scrutinise the disclosure notes to find any disclosure of the transaction, where it should be described as a related

party liability, and

– perform. a liquidity analysis to establish whether the amount can be repaid from liquid assets. -

第11题:

(a) List and explain FOUR methods of selecting a sample of items to test from a population in accordance with ISA 530 (Redrafted) Audit Sampling and Other Means of Testing. (4 marks)

(b) List and explain FOUR assertions from ISA 500 Audit Evidence that relate to the recording of classes of

transactions. (4 marks)

(c) In terms of audit reports, explain the term ‘modified’. (2 marks)

正确答案:

(a)SamplingmethodsMethodsofsamplinginaccordancewithISA530AuditSamplingandOtherMeansofTesting:Randomselection.Ensureseachiteminapopulationhasanequalchanceofselection,forexamplebyusingrandomnumbertables.Systematicselection.Inwhichanumberofsamplingunitsinthepopulationisdividedbythesamplesizetogiveasamplinginterval.Haphazardselection.Theauditorselectsthesamplewithoutfollowingastructuredtechnique–theauditorwouldavoidanyconsciousbiasorpredictability.Sequenceorblock.Involvesselectingablock(s)ofcontinguousitemsfromwithinapopulation.Tutorialnote:Othermethodsofsamplingareasfollows:MonetaryUnitSampling.Thisselectionmethodensuresthateachindividual$1inthepopulationhasanequalchanceofbeingselected.Judgementalsampling.Selectingitemsbasedontheskillandjudgementoftheauditor.(b)Assertions–classesoftransactionsOccurrence.Thetransactionsandeventsthathavebeenrecordedhaveactuallyoccurredandpertaintotheentity.Completeness.Alltransactionsandeventsthatshouldhavebeenrecordedhavebeenrecorded.Accuracy.Theamountsandotherdatarelatingtorecordedtransactionsandeventshavebeenrecordedappropriately.Cut-off.Transactionsandeventshavebeenrecordedinthecorrectaccountingperiod.Classification.Transactionsandeventshavebeenrecordedintheproperaccounts.(c)AuditreporttermModified.Anauditormodifiesanauditreportinanysituationwhereitisinappropriatetoprovideanunmodifiedreport.Forexample,theauditormayprovideadditionalinformationinanemphasisofmatter(whichdoesnotaffecttheauditor’sopinion)orqualifytheauditreportforlimitationofscopeordisagreement. -

第12题:

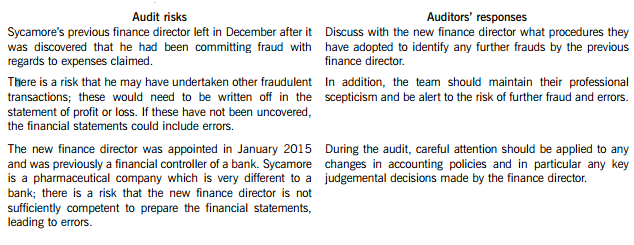

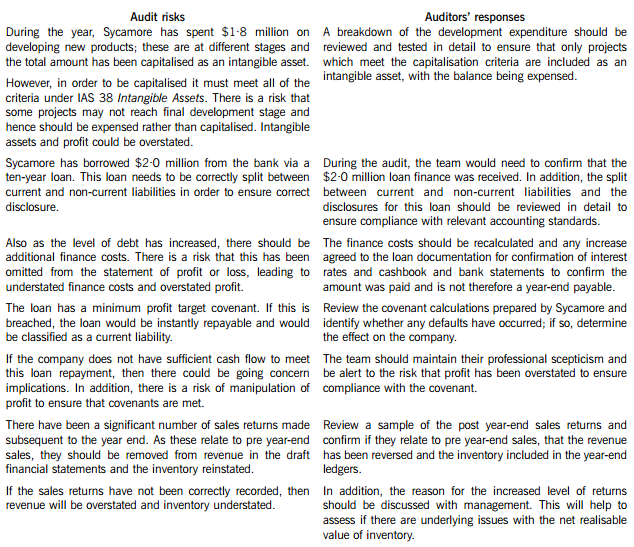

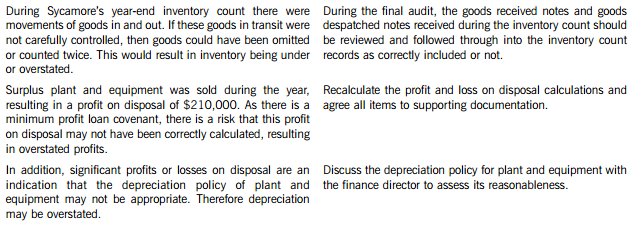

You are the audit supervisor of Maple & Co and are currently planning the audit of an existing client, Sycamore Science Co (Sycamore), whose year end was 30 April 2015. Sycamore is a pharmaceutical company, which manufactures and supplies a wide range of medical supplies. The draft financial statements show revenue of $35·6 million and profit before tax of $5·9 million.

Sycamore’s previous finance director left the company in December 2014 after it was discovered that he had been claiming fraudulent expenses from the company for a significant period of time. A new finance director was appointed in January 2015 who was previously a financial controller of a bank, and she has expressed surprise that Maple & Co had not uncovered the fraud during last year’s audit.

During the year Sycamore has spent $1·8 million on developing several new products. These projects are at different stages of development and the draft financial statements show the full amount of $1·8 million within intangible assets. In order to fund this development, $2·0 million was borrowed from the bank and is due for repayment over a ten-year period. The bank has attached minimum profit targets as part of the loan covenants.

The new finance director has informed the audit partner that since the year end there has been an increased number of sales returns and that in the month of May over $0·5 million of goods sold in April were returned.

Maple & Co attended the year-end inventory count at Sycamore’s warehouse. The auditor present raised concerns that during the count there were movements of goods in and out the warehouse and this process did not seem well controlled.

During the year, a review of plant and equipment in the factory was undertaken and surplus plant was sold, resulting in a profit on disposal of $210,000.

Required:

(a) State Maples & Co’s responsibilities in relation to the prevention and detection of fraud and error. (4 marks)

(b) Describe SIX audit risks, and explain the auditor’s response to each risk, in planning the audit of Sycamore Science Co. (12 marks)

(c) Sycamore’s new finance director has read about review engagements and is interested in the possibility of Maple & Co undertaking these in the future. However, she is unsure how these engagements differ from an external audit and how much assurance would be gained from this type of engagement.

Required:

(i) Explain the purpose of review engagements and how these differ from external audits; and (2 marks)

(ii) Describe the level of assurance provided by external audits and review engagements. (2 marks)

正确答案:(a) Fraud responsibility

Maple & Co must conduct an audit in accordance with ISA 240 The Auditor’s Responsibilities Relating to Fraud in an Audit of Financial Statements and are responsible for obtaining reasonable assurance that the financial statements taken as a whole are free from material misstatement, whether caused by fraud or error.

In order to fulfil this responsibility, Maple & Co is required to identify and assess the risks of material misstatement of the financial statements due to fraud.

They need to obtain sufficient appropriate audit evidence regarding the assessed risks of material misstatement due to fraud, through designing and implementing appropriate responses. In addition, Maple & Co must respond appropriately to fraud or suspected fraud identified during the audit.

When obtaining reasonable assurance, Maple & Co is responsible for maintaining professional scepticism throughout the audit, considering the potential for management override of controls and recognising the fact that audit procedures which are effective in detecting error may not be effective in detecting fraud.

To ensure that the whole engagement team is aware of the risks and responsibilities for fraud and error, ISAs require that a discussion is held within the team. For members not present at the meeting, Sycamore’s audit engagement partner should determine which matters are to be communicated to them.

(b) Audit risks and auditors’ responses

(c) (i) Review engagements

Review engagements are often undertaken as an alternative to an audit, and involve a practitioner reviewing financial data, such as six-monthly figures. This would involve the practitioner undertaking procedures to state whether anything has come to their attention which causes the practitioner to believe that the financial data is not in accordance with the financial reporting framework.

A review engagement differs to an external audit in that the procedures undertaken are not nearly as comprehensive as those in an audit, with procedures such as analytical review and enquiry used extensively. In addition, the practitioner does not need to comply with ISAs as these only relate to external audits.

(ii) Levels of assurance

The level of assurance provided by audit and review engagements is as follows:

External audit – A high but not absolute level of assurance is provided, this is known as reasonable assurance. This provides comfort that the financial statements present fairly in all material respects (or are true and fair) and are free of material misstatements.

Review engagements – where an opinion is being provided, the practitioner gathers sufficient evidence to be satisfied that the subject matter is plausible; in this case negative assurance is given whereby the practitioner confirms that nothing has come to their attention which indicates that the subject matter contains material misstatements.

-

第13题:

(c) Pinzon, a limited liability company and audit client, is threatening to sue your firm in respect of audit fees charged

for the year ended 31 December 2004. Pinzon is alleging that Bartolome billed the full rate on air fares for audit

staff when substantial discounts had been obtained by Bartolome. (4 marks)

Required:

Comment on the ethical and other professional issues raised by each of the above matters and their implications,

if any, for the continuation of each assignment.

NOTE: The mark allocation is shown against each of the three issues.

正确答案:

(c) Threatened legal action

Ethical and professional issues

■ An advocacy threat has arisen as Bartolome and Pinzon are in opposition concerning the fee note for the 2004 audit.

■ If Pinzon’s allegations are true this may cast serious doubt on the integrity of Bartolome. Pinzon should be advised to

take their claims first to ACCA’s Disciplinary Committee.

■ If Bartolome has indeed charged full air fares when substantial discounts had been obtained this could be due to:

– Bartolome incorrectly believing this to be an acceptable industry practice; or

– a billing error/oversight.

In either case Bartolome should issue a credit note, although this may be insufficient to make amends and salvage the

auditor-client relationship.

■ Bartolome may have legitimately claimed for full airfares if this was agreed in its contract (i.e. the terms of engagement)

with Pinzon.

Implications for continuation with assignment

Unless the threat of legal action is amicably resolved very quickly (which is perhaps unlikely) Pinzon and Bartolome are in

conflict. Bartolome cannot therefore be seen to be independent and so should tender their resignation as auditor for the year

ending 31 December 2005 (assuming they were re-appointed and have not already been removed from office). -

第14题:

(c) Explain the extent to which you should plan to place reliance on analytical procedures as audit evidence.

(6 marks)

正确答案:

(c) Extent of reliance on analytical procedures as audit evidence

Tutorial note: In the requirement ‘… reliance … as audit evidence’ is a direction to consider only substantive analytical

procedures. Answer points concerning planning and review stages were not asked for and earn no marks.

■ Although there is likely to be less reliance on analytical procedures than if this had been an existing audit client, the fact

that this is a new assignment does not preclude placing some reliance on such procedures.

■ Analytical procedures will not be relied on in respect of material items that require 100% testing. For example, additions

to property is likely to represent a very small number of transactions.

■ Analytical procedures alone may provide sufficient audit evidence on line items that are not individually material. For

example, inventory (less than 1/2% revenue and less than 1% total assets) may be shown to be materially correctly

stated through analytical procedures on consumable stores (i.e. fuel, lubricants, materials for servicing vehicles etc).

■ Substantive analytical procedures are best suited to large volume transactions (e.g. revenue, materials expense, staff

costs). If controls over the completeness, accuracy and validity of recording transactions in these areas are effective then

substantive analytical procedures showing that there are no unexpected fluctuations should reduce the need for

substantive detailed tests.

■ The extent of planned use will be dependent on the relationships expected between variables. (e.g. between items of

financial information and between items of financial and non-financial information). For example, if material costs rise

due to an increase in the level of business then a commensurate increase in revenue and staff costs might be expected

also.

■ ‘Proofs in total’ (or reasonableness tests) provide substantive evidence that income statement items are not materially

misstated. In the case of Yates these might be applied to staff costs (number of employees in each category ×

wage/salary rates, grossed up for social security, etc) and finance expense (interest rate × average monthly overdraft

balance).

■ However, such tests may have limited application, if any, if the population is not homogenous and cannot be subdivided.

For example, all the categories of non-current asset have a wide range of useful life. Therefore it would be

difficult/meaningless to apply an ‘average’ depreciation rate to all assets in the class to substantiate the total depreciation

expense for the year. (Although it might highlight a risk of potential over or understatement requiring further

investigation.)

■ Substantive analytical procedures are more likely to be used if there is relevant information available that is being used

by Yates. For example, as fuel costs will be significant, Yates may monitor consumption (e.g. miles per gallon (MPG)).

■ Analytical procedures may supplement alternative procedures that provide evidence regarding the same assertion. For

example, the review of after-date payments to confirm the completeness of trade payables may be supplemented by

calculations of average payment period on a monthly basis.

Tutorial note: Credit will be given for other relevant points drawn from the scenario. For example, the restructuring during

the previous year is likely to have caused fluctuations that may result in less reliance being placed on analytical procedures. -

第15题:

(c) In April 2006, Keffler was banned by the local government from emptying waste water into a river because the

water did not meet minimum standards of cleanliness. Keffler has made a provision of $0·9 million for the

technological upgrading of its water purifying process and included $45,000 for the penalties imposed in ‘other

provisions’. (5 marks)

Required:

For each of the above issues:

(i) comment on the matters that you should consider; and

(ii) state the audit evidence that you should expect to find,

in undertaking your review of the audit working papers and financial statements of Keffler Co for the year ended

31 March 2006.

NOTE: The mark allocation is shown against each of the three issues.

正确答案:

(c) Ban on emptying waste water

(i) Matter

■ $0·9m provision for upgrading the process represents 45% PBT and is very material. This provision is also

material to the balance sheet (2·7% of total assets).

■ The provision for penalties is immaterial (2·2% PBT and 0·1% total assets).

■ The ban is an adjusting post balance sheet event in respect of the penalties (IAS 10). It provides evidence that at

the balance sheet date Keffler was in contravention of local government standards. Therefore it is correct (in

accordance with IAS 37) that a provision has been made for the penalties. As the matter is not material inclusion

in ‘other provisions’ is appropriate.

■ However, even if Keffler has a legal obligation to meet minimum standards, there is no obligation for upgrading the

purifying process at 31 March 2006 and the $0·9m provision should be written back.

■ If the provision for upgrading is not written back the audit opinion should be qualified ‘except for’ (disagreement).

■ Keffler does not even have a contingent liability for upgrading the process because there is no present obligation to

do so. The obligation is to stop emptying unclean water into the river. Nor is there a possible obligation whose

existence will be confirmed by an uncertain future event not wholly within Keffler’s control.

Tutorial note: Consider that Keffler has alternatives wholly within its control. For example, it could ignore the ban

and incur fines, or relocate/close this particular plant/operation or perhaps dispose of the water by alternative

means.

■ The need for a technological upgrade may be an indicator of impairment. Management should have carried out

an impairment test on the carrying value of the water purifying process and recognised any impairment loss in the

profit for the year to 31 March 2006.

■ Management’s intention to upgrade the process is more appropriate to an environmental responsibility report (if

any).

■ Whether there is any other information in documents containing financial statements.

(ii) Audit evidence

■ Penalty notices of fines received to confirm amounts and period/dates covered.

■ After-date payment of fines agreed to the cash book.

■ A copy of the ban and any supporting report on the local government’s findings.

■ Minutes of board meetings at which the ban was discussed confirming management’s intentions (e.g. to upgrade

the process).

Tutorial note: This may be disclosed in the directors’ report and/or as a non-adjusting post balance sheet event.

■ Any tenders received/costings for upgrading.

Tutorial note: This will be relevant if, for example, capital commitment authorised (by the board) but not

contracted for at the year end are disclosed in the notes to the financial statements.

■ Physical inspection of the emptying point at the river to confirm that Keffler is not still emptying waste water into

it (unless the upgrading has taken place).

Tutorial note: Thereby incurring further penalties. -

第16题:

(c) Explain the possible impact of RBG outsourcing its internal audit services on the audit of the financial

statements by Grey & Co. (4 marks)

正确答案:

(c) Impact on the audit of the financial statements

Tutorial note: The answer to this part should reflect that it is not the external auditor who is providing the internal audit

services. Thus comments regarding objectivity impairment are not relevant.

■ As Grey & Co is likely to be placing some reliance on RBG’s internal audit department in accordance with ISA 610

Considering the Work of Internal Auditing the degree of reliance should be reassessed.

■ The appointment will include an evaluation of organisational risk. The results of this will provide Grey with evidence,

for example:

– supporting the appropriateness of the going concern assumption;

– of indicators of obsolescence of goods or impairment of other assets.

■ As the quality of internal audit services should be higher than previously, providing a stronger control environment, the

extent to which Grey may rely on internal audit work could be increased. This would increase the efficiency of the

external audit of the financial statements as the need for substantive procedures should be reduced.

■ However, if internal audit services are performed on a part-time basis (e.g. fitting into the provider’s less busy months)

Grey must evaluate the impact of this on the prevention, detection and control of fraud and error.

■ The internal auditors will provide a body of expertise within RBG with whom Grey can consult on contentious matters.

Tutorial note: Appropriate credit will be given for arguing that less reliance may be placed on internal audit in this year of

change of provider. -

第17题:

(b) As a newly-qualified Chartered Certified Accountant in Boleyn & Co, you have been assigned to assist the ethics

partner in developing ethical guidance for the firm. In particular, you have been asked to draft guidance on the

following frequently asked questions (‘FAQs’) that will be circulated to all staff through Boleyn & Co’s intranet:

(i) What Information Technology services can we offer to audit clients? (5 marks)

Required:

For EACH of the three FAQs, explain the threats to objectivity that may arise and the safeguards that should

be available to manage them to an acceptable level.

NOTE: The mark allocation is shown against each of the three questions.

正确答案:

(b) FAQs

(i) Information Technology (IT) services

The greatest threats to independence arise from the provision of any service which involves auditors in:

■ auditing their own work;

■ the decision-making process;

■ undertaking management functions of the client.

IT services potentially pose all these threats:

■ self-interest threat – on-going services that provide a large proportion of Boleyn’s annual fees will contribute to a

threat to objectivity;

■ self-review threat – e.g. when IT services provided involve (i) the supervision of the audit client’s employees in the

performance of their normal duties; or (ii) the origination of electronic data evidencing the occurrence of

transactions;

■ management threat – e.g. when the IT services involve making judgments and taking decisions that are properly

the responsibility of management.

Thus, services that involve the design and implementation of financial IT systems that are used to generate information

forming a significant part of a client’s accounting system or financial statements is likely to create significant ethical

threats.

Possible safeguards include:

■ disclosing and discussing fees with the client’s audit committees (or others charged with corporate governance);

■ the audit client providing a written acknowledgment (e.g. in an engagement letter) of its responsibility for:

– establishing and monitoring a system of internal controls;

– the operation of the system (hardware or software); and

– the data used or generated by the system;

■ the designation by the audit client of a competent employee (preferably within senior management) with

responsibility to make all management decisions regarding the design and implementation of the hardware or

software system;

■ evaluation of the adequacy and results of the design and implementation of the system by the audit client;

■ suitable allocation of work within the firm (i.e. staff providing the IT services not being involved in the audit

engagement and having different reporting lines); and

■ review of the audit opinion by an audit partner who is not involved in the audit engagement.

Services in connection with the assessment, design and implementation of internal accounting controls and risk

management controls are not considered to create a threat to independence provided that the firm’s personnel do not

perform. management functions.

It would be acceptable to provide IT services to an audit client where the systems are not important to any significant

part of the accounting system or the production of financial statements and do not have significant reliance placed on

them by the auditors, provided that:

■ a member of the client’s management has been designated to receive and take responsibility for the results of the

IT work undertaken; and

■ appropriate safeguards are put in place (e.g. using separate partners and staff for each role and review by a partner

not involved in the audit engagement).

It would also generally be acceptable to provide and install off-the-shelf accounting packages to an audit client. -

第18题:

(iii) Can audit teams cross sell services to their clients? (4 marks)

Required:

For EACH of the three FAQs, explain the threats to objectivity that may arise and the safeguards that should

be available to manage them to an acceptable level.

NOTE: The mark allocation is shown against each of the three questions.

正确答案:

(iii) Cross selling services

The practice of cross selling is intended to give incentives to members of audit teams to concentrate their efforts on the

selling of non-audit services to audit clients.

It is not inappropriate for an audit firm to cross sell or for members of the audit team to recognise on an ongoing basis

the need of a client to have non audit services. However it should not be an aim of the audit team member to seek out

such opportunities.

Boleyn should have policies and procedures to ensure that, in relation to each audit client:

■ the objectives of the members of the audit team do not include selling of non-audit services to the audit client;

■ the criteria for evaluating the performance of members of the audit team do not include success in selling nonaudit

services to the audit client;

■ no specific element of remuneration of a member of the audit team and no decision concerning promotion within

the audit firm is based on his or her success in selling non-audit services to the audit client; and

■ the ethics partner being available for consultation when needed.

Therefore objectives such as the following are inappropriate:

■ to meet a quota of opportunities;

■ to specifically make time to discuss with clients which non-audit services they should consider;

■ to develop identified selling opportunities.

An audit engagement partner’s performance should be judged on the quality and integrity of the audit only. There are

no restrictions on normal partnership profit-sharing arrangements.

-

第19题:

(b) As a newly-qualified Chartered Certified Accountant, you have been asked to write an ‘ethics column’ for a trainee

accountant magazine. In particular, you have been asked to draft guidance on the following questions addressed

to the magazine’s helpline:

(i) What gifts or hospitality are acceptable and when do they become an inducement? (5 marks)

Required:

For each of the three questions, explain the threats to objectivity that may arise and the safeguards that

should be available to manage them to an acceptable level.

NOTE: The mark allocation is shown against each of the three questions above.

正确答案:

(b) Draft guidance

(i) Gifts and hospitality

Gifts and hospitality may be offered as an inducement i.e. to unduly influence actions or decisions, encourage illegal or

dishonest behaviour or to obtain confidential information. An offer of gifts and/or hospitality from a client ordinarily gives

rise to threats to compliance with the fundamental principles, for example:

■ self-interest threats to objectivity and/or confidentiality may be created if a gift from a client is accepted;

■ intimidation threats to objectivity and/or confidentiality may arise through the possibility of such offers being made

public and damaging the reputation of the professional accountant (or close family member).

The significance of such threats will depend on the nature, value and intent behind the offer. There may be no significant

threat to compliance with the fundamental principles if a reasonable and informed third party would consider gifts and

hospitality to be clearly insignificant. For example, if the offer of gifts or hospitality is made in the normal course of

business without the specific intent to influence decision making or to obtain information.

If evaluated threats are other than clearly insignificant, safeguards should be considered and applied as necessary to

eliminate them or reduce them to an acceptable level.

Offers of gifts and hospitality should not be accepted if the threats cannot be eliminated or reduced to an acceptable

level through the application of safeguards.

As the real or apparent threats to compliance with the fundamental principles do not merely arise from acceptance of

an inducement but, sometimes, merely from the fact of the offer having been made, additional safeguards should be

adopted. For example:

■ immediately informing higher levels of management or those charged with governance that an inducement has

been offered;

■ informing third parties (e.g. a professional body) of the offer (after seeking legal advice);

■ advising immediate or close family members of relevant threats and safeguards where they are potentially in

positions that might result in offers of inducements (e.g. as a result of their employment situation); and

■ informing higher levels of management or those charged with governance where immediate or close family

members are employed by competitors or potential suppliers of that organisation. -

第20题:

(b) Explain the principal audit procedures to be performed during the final audit in respect of the estimated

warranty provision in the balance sheet of Island Co as at 30 November 2007. (5 marks)

正确答案:

(b) ISA 540 Audit of Accounting Estimates requires that auditors should obtain sufficient audit evidence as to whether an

accounting estimate, such as a warranty provision, is reasonable given the entity’s circumstances, and that disclosure is

appropriate. One, or a combination of the following approaches should be used:

Review and test the process used by management to develop the estimate

– Review contracts or orders for the terms of the warranty to gain an understanding of the obligation of Island Co

– Review correspondence with customers during the year to gain an understanding of claims already in progress at the

year end

– Perform. analytical procedures to compare the level of warranty provision year on year, and compare actual to budgeted

provisions. If possible disaggregate the data, for example, compare provision for specific types of machinery or customer

by customer

– Re-calculate the warranty provision

– Agree the percentage applied in the calculation to the stated accounting policy of Island Co

– Review board minutes for discussion of on-going warranty claims, and for approval of the amount provided

– Use management accounts to ascertain normal level of warranty rectification costs during the year

– Discuss with Kate Shannon the assumptions she used to determine the percentage used in her calculations

– Consider whether assumptions used are consistent with the auditors’ understanding of the business

– Compare prior year provision with actual expenditure on warranty claims in the accounting period

– Compare the current year provision with prior year and discuss any fluctuation with Kate Shannon.

Review subsequent events which confirm the estimate made

– Review any work carried out post year end on specific faults that have been provided for. Agree that all costs are included

in the year end provision.

– Agree cash expended on rectification work in the post balance sheet period to the cash book

– Agree cash expended on rectification work post year end to suppliers’ invoices, or to internal cost ledgers if work carried

out by employees of Island Co

– Read customer correspondence received post year end for any claims received since the year end. -

第21题:

(ii) Identify and explain the principal audit procedures to be performed on the valuation of the investment

properties. (6 marks)

正确答案:

(ii) Additional audit procedures

Audit procedures should focus on the appraisal of the work of the expert valuer. Procedures could include the following:

– Inspection of the written instructions provided by Poppy Co to the valuer, which should include matters such as

the objective and scope of the valuer’s work, the extent of the valuer’s access to relevant records and files, and

clarification of the intended use by the auditor of their work.

– Evaluation, using the valuation report, that any assumptions used by the valuer are in line with the auditor’s

knowledge and understanding of Poppy Co. Any documentation supporting assumptions used by the valuer should

be reviewed for consistency with the auditor’s business understanding, and also for consistency with any other

audit evidence.

– Assessment of the methodology used to arrive at the fair value and confirmation that the method is consistent with

that required by IAS 40.

– The auditor should confirm, using the valuation report, that a consistent method has been used to value each

property.

– It should also be confirmed that the date of the valuation report is reasonably close to the year end of Poppy Co.

– Physical inspection of the investment properties to determine the physical condition of the properties supports the

valuation.

– Inspect the purchase documentation of each investment property to ascertain the cost of each building. As the

properties were acquired during this accounting period, it would be reasonable to expect that the fair value at the

year end is not substantially different to the purchase price. Any significant increase or decrease in value should

alert the auditor to possible misstatement, and lead to further audit procedures.

– Review of forecasts of rental income from the properties – supporting evidence of the valuation.

– Subsequent events should be monitored for any additional evidence provided on the valuation of the properties.

For example, the sale of an investment property shortly after the year end may provide additional evidence relating

to the fair value measurement.

– Obtain a management representation regarding the reasonableness of any significant assumptions, where relevant,

to fair value measurements or disclosures. -

第22题:

(ii) From the information provided above, recommend the matters which should be included as ‘findings

from the audit’ in your report to those charged with governance, and explain the reason for their

inclusion. (7 marks)

正确答案:

(ii) Control weakness

ISA 260 contains guidance on the type of issues that should be communicated. One of the matters identified is a control

weakness in the capital expenditure transaction cycle. The assets for which no authorisation was obtained amount to

0·3% of total assets (225,000/78 million x 100%), which is clearly immaterial. However, regardless of materiality, the

auditor should ensure that the weakness is brought to the attention of the management, with a clear indication of the

implication of the weakness, and recommendations as to how the control weakness should be eliminated.

The auditor is providing information to help those charged with governance improve the internal systems and controls

and ultimately reduce business risk. In this case there is a high risk of fraud, as the lack of authorisation for purchase

of office equipment could allow expenditure on assets not used for bona fide business purposes.

Disagreement with accounting treatment of brand

Audit procedures have revealed a breach of IAS 38 Intangible Assets, in which internally generated brand names are

specifically prohibited from being recognised. Blod Co has recognised an internally generated brand name which is

material to the statement of financial position (balance sheet) as it represents 12·8% of total assets (10/78 x 100%).

The statement of financial position (balance sheet) therefore contains a material misstatement.

The report to those charged with governance should clearly explain the rules on recognition of internally generated brand

names, to ensure that the management has all relevant technical facts available. In the report the auditors should

request that the financial statements be corrected, and clarify that if the brand is not derecognised, then the audit opinion

will be qualified on the grounds of a material disagreement – an ‘except for’ opinion would be provided. Once the breach

of IAS 38 is made clear to the management in the report, they then have the opportunity to discuss the matter and

decide whether to amend the financial statements, thereby avoiding a qualified audit opinion.

Audit inefficiencies

Documentation relating to inventories was not always made readily available to the auditors. This seems to be due to

poor administration by the client rather than a deliberate attempt to conceal information. The report should contain a

brief description of the problems encountered by the audit team. The management should be made aware that

significant delay to the receipt of necessary paperwork can cause inefficiencies in the audit process. This may seem a

relatively trivial issue, but it could lead to an increase in audit fee. Management should react to these comments by

ensuring as far as possible that all requested documentation is made available to the auditors in a timely fashion. -

第23题: