During the year the internal auditor of Mulligan Co discovered several discrepancies in the inventory records. In astatement made to the board of directors, the internal auditor said:‘I think that someone is taking items from the warehouse. A physical inv

题目

During the year the internal auditor of Mulligan Co discovered several discrepancies in the inventory records. In a

statement made to the board of directors, the internal auditor said:

‘I think that someone is taking items from the warehouse. A physical inventory count is performed every three months,

and it has become apparent that about 200 boxes of flat-packed chairs and tables are disappearing from the

warehouse every month. We should get someone to investigate what has happened and quantify the value of the

loss.’

Required:

(c) Define ‘forensic accounting’ and explain its relevance to the statement made by the internal auditor.

(5 marks)

相似考题

更多“During the year the internal auditor of Mulligan Co discovered several discrepancies in the inventory records. In astatement made to the board of directors, the internal auditor said:‘I think that someone is taking items from the warehouse. A physical inv”相关问题

-

第1题:

(b) You are the audit manager of Jinack Co, a private limited liability company. You are currently reviewing two

matters that have been left for your attention on the audit working paper file for the year ended 30 September

2005:

(i) Jinack holds an extensive range of inventory and keeps perpetual inventory records. There was no full

physical inventory count at 30 September 2005 as a system of continuous stock checking is operated by

warehouse personnel under the supervision of an internal audit department.

A major systems failure in October 2005 caused the perpetual inventory records to be corrupted before the

year-end inventory position was determined. As data recovery procedures were found to be inadequate,

Jinack is reconstructing the year-end quantities through a physical count and ‘rollback’. The reconstruction

exercise is expected to be completed in January 2006. (6 marks)

Required:

Identify and comment on the implications of the above matters for the auditor’s report on the financial

statements of Jinack Co for the year ended 30 September 2005 and, where appropriate, the year ending

30 September 2006.

NOTE: The mark allocation is shown against each of the matters.

正确答案:

(b) Implications for the auditor’s report

(i) Corruption of perpetual inventory records

■ The loss of data (of physical inventory quantities at the balance sheet date) gives rise to a limitation on scope.

Tutorial note: It is the records of the asset that have been destroyed – not the physical asset.

■ The systems failure in October 2005 is clearly a non-adjusting post balance sheet event (IAS 10). If it is material

(such that non-disclosure could influence the economic decisions of users) Jinack should disclose:

– the nature of the event (i.e. systems failure); and

– an estimate of its financial effect (i.e. the cost of disruption and reconstruction of data to the extent that it is

not covered by insurance).

Tutorial note: The event has no financial effect on the realisability of inventory, only on its measurement for the

purpose of reporting it in the financial statements.

■ If material this disclosure could be made in the context of explaining how inventory has been estimated at

30 September 2005 (see later). If such disclosure, that the auditor considers to be necessary, is not made, the

audit opinion should be qualified ‘except for’ disagreement (over lack of disclosure).

Tutorial note: Such qualifications are extremely rare since management should be persuaded to make necessary

disclosure in the notes to the financial statements rather than have users’ attention drawn to the matter through

a qualification of the audit opinion.

■ The limitation on scope of the auditor’s work has been imposed by circumstances. Jinack’s accounting records

(for inventory) are inadequate (non-existent) for the auditor to perform. tests on them.

■ An alternative procedure to obtain sufficient appropriate audit evidence of inventory quantities at a year end is

subsequent count and ‘rollback’. However, the extent of ‘roll back’ testing is limited as records are still under

reconstruction.

■ The auditor may be able to obtain sufficient evidence that there is no material misstatement through a combination

of procedures:

– testing management’s controls over counting inventory after the balance sheet date and recording inventory

movements (e.g. sales and goods received);

– reperforming the reconstruction for significant items on a sample basis;

– analytical procedures such as a review of profit margins by inventory category.

■ ‘An extensive range of inventory’ is clearly material. The matter (i.e. systems failure) is not however pervasive, as

only inventory is affected.

■ Unless the reconstruction is substantially completed (i.e. inventory items not accounted for are insignificant) the

auditor cannot determine what adjustment, if any, might be determined to be necessary. The auditor’s report

should then be modified, ‘except for’, limitation on scope.

■ However, if sufficient evidence is obtained the auditor’s report should be unmodified.

■ An ‘emphasis of matter’ paragraph would not be appropriate because this matter is not one of significant

uncertainty.

Tutorial note: An uncertainty in this context is a matter whose outcome depends on future actions or events not

under the direct control of Jinack.

2006

■ If the 2005 auditor’s report is qualified ‘except for’ on grounds of limitation on scope there are two possibilities for

the inventory figure as at 30 September 2005 determined on completion of the reconstruction exercise:

(1) it is not materially different from the inventory figure reported; or

(2) it is materially different.

■ In (1), with the limitation now removed, the need for qualification is removed and the 2006 auditor’s report would

be unmodified (in respect of this matter).

■ In (2) the opening position should be restated and the comparatives adjusted in accordance with IAS 8 ‘Accounting

Policies, Changes in Accounting Estimates and Errors’. The 2006 auditor’s report would again be unmodified.

Tutorial note: If the error was not corrected in accordance with IAS 8 it would be a different matter and the

auditor’s report would be modified (‘except for’ qualification) disagreement on accounting treatment. -

第2题:

(b) Chatam, a limited liability company, is a long-standing client. One of its subsidiaries, Ayora, has made losses

for several years. At your firm’s request, Chatam’s management has made a written representation that goodwill

arising on the acquisition of Ayora is not impaired. Your firm’s auditor’s report on the consolidated financial

statements of Chatam for the year ended 31 March 2005 is unmodified. Your firm’s auditor’s report on the

financial statements of Ayora is similarly unmodified. Chatam’s Chief Executive, Charles Barrington, is due to

retire in 2006 when his share options mature. (6 marks)

Required:

Comment on the ethical and other professional issues raised by each of the above matters and their implications,

if any, for the continuation of each assignment.

NOTE: The mark allocation is shown against each of the three issues.

正确答案:

(b) Unmodified auditor’s reports

Ethical and professional issues

■ An unmodified opinion means, inter alia, that:

– there are no material matters giving rise to disagreement with the auditor; and

– the auditor’s report does not include an emphasis of matter paragraph (e.g. regarding going concern).

■ By implication the auditor must have obtained sufficient appropriate evidence that notwithstanding the losses:

– the going concern basis is appropriate to Ayora’s financial statements and any related matters (e.g. parental

support) are adequately disclosed therein;

– goodwill in Chatam’s consolidated financial statements is not materially impaired.

■ Management’s written representation (that the goodwill is not impaired) must have been necessary (otherwise it should

not have been asked for). This means that Bartolome does not have sufficient other audit evidence. This seems dubious

as management should have carried out an impairment test to satisfy themselves that goodwill is not impaired. This

test should similarly have satisfied Bartolome.

■ If there is evidence that goodwill is impaired management’s refusal to write it down might be considered a fraud.

■ The matter may cast doubt on the quality of audit evidence obtained in other areas. All other matters on which

management representations have been obtained should be reviewed by another audit partner/manager.

■ Charles Barrington is retiring next year and his share options would presumably be worth less if goodwill were written

down. His position in this long-standing client suggests a familiarity threat.

■ Bartolome may be threatened by self-interest to accept the representation as sufficient in order to retain the client.

■ Bartolome may be unduly influenced by a combination of factors (familiarity and previous experience) and failing to

exercise the necessary degree of professional scepticism.

Implications for continuation with assignment

There is no reason why the audit should not be continued. However, a change in senior audit staff and audit manager may

be overdue. The unmodified auditor’s reports should be subject to a cold review and any quality control issues raised with

the staff who conducted the audit. -

第3题:

4 (a) The purpose of ISA 250 Consideration of Laws and Regulations in an Audit of Financial Statements is to

establish standards and provide guidance on the auditor’s responsibility to consider laws and regulations in an

audit of financial statements.

Explain the auditor’s responsibilities for reporting non-compliance that comes to the auditor’s attention

during the conduct of an audit. (5 marks)

正确答案:

4 CLEEVES CO

(a) Reporting non-compliance

Non-compliance refers to acts of omission or commission by the entity being audited, either intentional or unintentional, that

are contrary to the prevailing laws or regulations.

To management

Regarding non-compliance that comes to the auditor’s attention the auditor should, as soon as practicable, either:

■ communicate with those charged with governance; or

■ obtain audit evidence that they are appropriately informed.

However, the auditor need not do so for matters that are clearly inconsequential or trivial and may reach agreement1 in

advance on the nature of such matters to be communicated.

If in the auditor’s judgment the non-compliance is believed to be intentional and material, the auditor should communicate

the finding without delay.

If the auditor suspects that members of senior management are involved in non-compliance, the auditor should report the

matter to the next higher level of authority at the entity, if it exists (e.g. an audit committee or a supervisory board). Where

no higher authority exists, or if the auditor believes that the report may not be acted upon or is unsure as to the person to

whom to report, the auditor would consider seeking legal advice.

To the users of the auditor’s report on the financial statements

If the auditor concludes that the non-compliance has a material effect on the financial statements, and has not been properly

reflected in the financial statements, the auditor expresses a qualified (i.e. ‘except for disagreement’) or an adverse opinion.

If the auditor is precluded by the entity from obtaining sufficient appropriate audit evidence to evaluate whether or not noncompliance

that may be material to the financial statements has (or is likely to have) occurred, the auditor should express a

qualified opinion or a disclaimer of opinion on the financial statements on the basis of a limitation on the scope of the audit.

Tutorial note: For example, if management denies the auditor access to information from which he would be able to assess

whether or not illegal dumping had taken place (and, if so, the extent of it).

If the auditor is unable to determine whether non-compliance has occurred because of limitations imposed by circumstances

rather than by the entity, the auditor should consider the effect on the auditor’s report.

Tutorial note: For example, if new legal requirements have been announced as effective but the detailed regulations are not

yet published.

To regulatory and enforcement authorities

The auditor’s duty of confidentiality ordinarily precludes reporting non-compliance to a third party. However, in certain

circumstances, that duty of confidentiality is overridden by statute, law or by courts of law (e.g. in some countries the auditor

is required to report non-compliance by financial institutions to the supervisory authorities). The auditor may need to seek

legal advice in such circumstances, giving due consideration to the auditor’s responsibility to the public interest. -

第4题:

(ii) On 1 July 2006 Petrie introduced a 10-year warranty on all sales of its entire range of stainless steel

cookware. Sales of stainless steel cookware for the year ended 31 March 2007 totalled $18·2 million. The

notes to the financial statements disclose the following:

‘Since 1 July 2006, the company’s stainless steel cookware is guaranteed to be free from defects in

materials and workmanship under normal household use within a 10-year guarantee period. No provision

has been recognised as the amount of the obligation cannot be measured with sufficient reliability.’

(4 marks)

Your auditor’s report on the financial statements for the year ended 31 March 2006 was unmodified.

Required:

Identify and comment on the implications of these two matters for your auditor’s report on the financial

statements of Petrie Co for the year ended 31 March 2007.

NOTE: The mark allocation is shown against each of the matters above.

正确答案:

(ii) 10-year guarantee

$18·2 million stainless steel cookware sales amount to 43·1% of revenue and are therefore material. However, the

guarantee was only introduced three months into the year, say in respect of $13·6 million (3/4 × 18·2 million) i.e.

approximately 32% of revenue.

The draft note disclosure could indicate that Petrie’s management believes that Petrie has a legal obligation in respect

of the guarantee, that is not remote and likely to be material (otherwise no disclosure would have been required).

A best estimate of the obligation amounting to 5% profit before tax (or more) is likely to be considered material, i.e.

$90,000 (or more). Therefore, if it is probable that 0·66% of sales made under guarantee will be returned for refund,

this would require a warranty provision that would be material.

Tutorial note: The return of 2/3% of sales over a 10-year period may well be probable.

Clearly there is a present obligation as a result of a past obligating event for sales made during the nine months to

31 March 2007. Although the likelihood of outflow under the guarantee is likely to be insignificant (even remote) it is

probable that some outflow will be needed to settle the class of such obligations.

The note in the financial statements is disclosing this matter as a contingent liability. This term encompasses liabilities

that do not meet the recognition criteria (e.g. of reliable measurement in accordance with IAS 37 Provisions, Contingent

Liabilities and Contingent Assets).

However, it is extremely rare that no reliable estimate can be made (IAS 37) – the use of estimates being essential to

the preparation of financial statements. Petrie’s management must make a best estimate of the cost of refunds/repairs

under guarantee taking into account, for example:

■ the proportion of sales during the nine months to 31 March 2007 that have been returned under guarantee at the

balance sheet date (and in the post balance sheet event period);

■ the average age of cookware showing a defect;

■ the expected cost of a replacement item (as a refund of replacement is more likely than a repair, say).

If management do not make a provision for the best estimate of the obligation the audit opinion should be qualified

‘except for’ non-compliance with IAS 37 (no provision made). The disclosure made in the note to the financial

statements, however detailed, is not a substitute for making the provision.

Tutorial note: No marks will be awarded for suggesting that an emphasis of matter of paragraph would be appropriate

(drawing attention to the matter more fully explained in the note).

Management’s claim that the obligation cannot be measured with sufficient reliability does not give rise to a limitation

on scope on the audit. The auditor has sufficient evidence of the non-compliance with IAS 37 and disagrees with it. -

第5题:

4 You are an audit manager in Nate & Co, a firm of Chartered Certified Accountants. You are reviewing three situations,

which were recently discussed at the monthly audit managers’ meeting:

(1) Nate & Co has recently been approached by a potential new audit client, Fisher Co. Your firm is keen to take the

appointment and is currently carrying out client acceptance procedures. Fisher Co was recently incorporated by

Marcellus Fisher, with its main trade being the retailing of wooden storage boxes.

(2) Nate & Co provides the audit service to CF Co, a national financial services organisation. Due to a number of

errors in the recording of cash deposits from new customers that have been discovered by CF Co’s internal audit

team, the directors of CF Co have requested that your firm carry out a review of the financial information

technology systems. It has come to your attention that while working on the audit planning of CF Co, Jin Sayed,

one of the juniors on the audit team, who is a recent information technology graduate, spent three hours

providing advice to the internal audit team about how to improve the system. As far as you know, this advice has

not been used by the internal audit team.

(3) LA Shots Co is a manufacturer of bottled drinks, and has been an audit client of Nate & Co for five years. Two

audit juniors attended the annual inventory count last Monday. They reported that Brenda Mangle, the new

production manager of LA Shots Co, wanted the inventory count and audit procedures performed as quickly as

possible. As an incentive she offered the two juniors ten free bottles of ‘Super Juice’ from the end of the

production line. Brenda also invited them to join the LA Shots Co office party, which commenced at the end of

the inventory count. The inventory count and audit procedures were completed within two hours (the previous

year’s procedures lasted a full day), and the juniors then spent four hours at the office party.

Required:

(a) Define ‘money laundering’ and state the procedures specific to money laundering that should be considered

before, and on the acceptance of, the audit appointment of Fisher Co. (5 marks)

正确答案:

4 NATE & CO

(a) – Money laundering is the process by which criminals attempt to conceal the true origin and ownership of the proceeds

of criminal activity, allowing them to maintain control over the proceeds, and ultimately providing a legitimate cover for

their sources of income. The objective of money laundering is to break the connection between the money, and the crime

that it resulted from.

– It is widely defined, to include possession of, or concealment of, the proceeds of any crime.

– Examples include proceeds of fraud, tax evasion and benefits of bribery and corruption.

Client procedures should include the following:

– Client identification:

? Establish the identity of the entity and its business activity e.g. by obtaining a certificate of incorporation

? If the client is an individual, obtain official documentation including a name and address, e.g. by looking at

photographic identification such as passports and driving licences

? Consider whether the commercial activity makes business sense (i.e. it is not just a ‘front’ for illegal activities)

? Obtain evidence of the company’s registered address e.g. by obtaining headed letter paper

? Establish the current list of principal shareholders and directors.

– Client understanding:

? Pre-engagement communication may be considered, to explain to Marcellus Fisher and the other directors the

nature and reason for client acceptance procedures.

? Best practice recommends that the engagement letter should also include a paragraph outlining the auditor’s

responsibilities in relation to money laundering. -

第6题:

(a) Contrast the role of internal and external auditors. (8 marks)

(b) Conoy Co designs and manufactures luxury motor vehicles. The company employs 2,500 staff and consistently makes a net profit of between 10% and 15% of sales. Conoy Co is not listed; its shares are held by 15 individuals, most of them from the same family. The maximum shareholding is 15% of the share capital.

The executive directors are drawn mainly from the shareholders. There are no non-executive directors because the company legislation in Conoy Co’s jurisdiction does not require any. The executive directors are very successful in running Conoy Co, partly from their training in production and management techniques, and partly from their ‘hands-on’ approach providing motivation to employees.

The board are considering a significant expansion of the company. However, the company’s bankers are

concerned with the standard of financial reporting as the financial director (FD) has recently left Conoy Co. The board are delaying provision of additional financial information until a new FD is appointed.

Conoy Co does have an internal audit department, although the chief internal auditor frequently comments that the board of Conoy Co do not understand his reports or provide sufficient support for his department or the internal control systems within Conoy Co. The board of Conoy Co concur with this view. Anders & Co, the external auditors have also expressed concern in this area and the fact that the internal audit department focuses work on control systems, not financial reporting. Anders & Co are appointed by and report to the board of Conoy Co.

The board of Conoy Co are considering a proposal from the chief internal auditor to establish an audit committee.

The committee would consist of one executive director, the chief internal auditor as well as three new appointees.

One appointee would have a non-executive seat on the board of directors.

Required:

Discuss the benefits to Conoy Co of forming an audit committee. (12 marks)

正确答案:

(a)Roleofinternalandexternalauditors–differencesObjectivesThemainobjectiveofinternalauditistoimproveacompany’soperations,primarilyintermsofvalidatingtheefficiencyandeffectivenessoftheinternalcontrolsystemsofacompany.Themainobjectiveoftheexternalauditoristoexpressanopiniononthetruthandfairnessofthefinancialstatements,andotherjurisdictionspecificrequirementssuchasconfirmingthatthefinancialstatementscomplywiththereportingrequirementsincludedinlegislation.ReportingInternalauditreportsarenormallyaddressedtotheboardofdirectors,orotherpeoplechargedwithgovernancesuchastheauditcommittee.Thosereportsarenotpubliclyavailable,beingconfidentialbetweentheinternalauditorandtherecipient.Externalauditreportsareprovidedtotheshareholdersofacompany.Thereportisattachedtotheannualfinancialstatementsofthecompanyandisthereforepubliclyavailabletotheshareholdersandanyreaderofthefinancialstatements.ScopeofworkTheworkoftheinternalauditornormallyrelatestotheoperationsoftheorganisation,includingthetransactionprocessingsystemsandthesystemstoproducetheannualfinancialstatements.Theinternalauditormayalsoprovideotherreportstomanagement,suchasvalueformoneyauditswhichexternalauditorsrarelybecomeinvolvedwith.Theworkoftheexternalauditorrelatesonlytothefinancialstatementsoftheorganisation.However,theinternalcontrolsystemsoftheorganisationwillbetestedastheseprovideevidenceonthecompletenessandaccuracyofthefinancialstatements.RelationshipwithcompanyInmostorganisations,theinternalauditorisanemployeeoftheorganisation,whichmayhaveanimpactontheauditor’sindependence.However,insomeorganisationstheinternalauditfunctionisoutsourced.Theexternalauditorisappointedbytheshareholdersofanorganisation,providingsomedegreeofindependencefromthecompanyandmanagement.(b)BenefitsofauditcommitteeinConoyCoAssistancewithfinancialreporting(nofinanceexpertise)TheexecutivedirectorsofConoyCodonotappeartohaveanyspecificfinancialskills–asthefinancialdirectorhasrecentlyleftthecompanyandhasnotyetbeenreplaced.ThismaymeanthatfinancialreportinginConoyCoislimitedorthattheothernon-financialdirectorsspendasignificantamountoftimekeepinguptodateonfinancialreportingissues.AnauditcommitteewillassistConoyCobyprovidingspecialistknowledgeoffinancialreportingonatemporarybasis–atleastoneofthenewappointeesshouldhaverelevantandrecentfinancialreportingexperienceundercodesofcorporategovernance.ThiswillallowtheexecutivedirectorstofocusonrunningConoyCo.EnhanceinternalcontrolsystemsTheboardofConoyCodonotnecessarilyunderstandtheworkoftheinternalauditor,ortheneedforcontrolsystems.ThismeansthatinternalcontrolwithinConoyComaybeinadequateorthatemployeesmaynotrecognisetheimportanceofinternalcontrolsystemswithinanorganisation.TheauditcommitteecanraiseawarenessoftheneedforgoodinternalcontrolsystemssimplybybeingpresentinConoyCoandbyeducatingtheboardontheneedforsoundcontrols.Improvingtheinternalcontrol‘climate’willensuretheneedforinternalcontrolsisunderstoodandreducecontrolerrors.RelianceonexternalauditorsConoyCo’sinternalauditorscurrentlyreporttotheboardofConoyCo.Aspreviouslynoted,thelackoffinancialandcontrolexpertiseontheboardwillmeanthatexternalauditorreportsandadvicewillnotnecessarilybeunderstood–andtheboardmayrelytoomuchonexternalauditorsIfConoyCoreporttoanauditcommitteethiswilldecreasethedependenceoftheboardontheexternalauditors.Theauditcommitteecantaketimetounderstandtheexternalauditor’scomments,andthenviathenon-executivedirector,ensurethattheboardtakeactiononthosecomments.AppointmentofexternalauditorsAtpresent,theboardofConoyCoappointtheexternalauditors.Thisraisesissuesofindependenceastheboardmaybecometoofamiliarwiththeexternalauditorsandsoappointonthisfriendshipratherthanmerit.Ifanauditcommitteeisestablished,thenthiscommitteecanrecommendtheappointmentoftheexternalauditors.Thecommitteewillhavethetimeandexpertisetoreviewthequalityofserviceprovidedbytheexternalauditors,removingtheindependenceissue.Corporategovernancerequirements–bestpracticeConoyCodonotneedtofollowcorporategovernancerequirements(thecompanyisnotlisted).However,notfollowingthoserequirementsmaystarttohaveadverseeffectsonConoy.Forexample,ConoyCo’sbankisalreadyconcernedaboutthelackoftransparencyinreporting.EstablishinganauditcommitteewillshowthattheboardofConoyCoarecommittedtomaintainingappropriateinternalsystemsinthecompanyandprovidingthestandardofreportingexpectedbylargecompanies.Obtainingthenewbankloanshouldalsobeeasierasthebankwillbesatisfiedwithfinancialreportingstandards.Givennonon-executives–independentadvicetoboardCurrentlyConoyCodoesnothaveanynon-executivedirectors.Thismeansthatthedecisionsoftheexecutivedirectorsarenotbeingchallengedbyotherdirectorsindependentofthecompanyandwithlittleornofinancialinterestinthecompany.Theappointmentofanauditcommitteewithonenon-executivedirectorontheboardofConoyCowillstarttoprovidesomenon-executiveinputtoboardmeetings.Whilenotsufficientintermsofcorporategovernancerequirements(aboutequalnumbersofexecutiveandnon-executivedirectorsareexpected)itdoesshowtheboardofConoyCoareattemptingtoestablishappropriategovernancesystems.AdviceonriskmanagementFinally,thereareothergeneralareaswhereConoyCowouldbenefitfromanauditcommittee.Forexample,lackofcorporategovernancestructuresprobablymeansConoyCodoesnothaveariskmanagementcommittee.Theauditcommitteecanalsoprovideadviceonriskmanagement,helpingtodecreasetheriskexposureofthecompany. -

第7题:

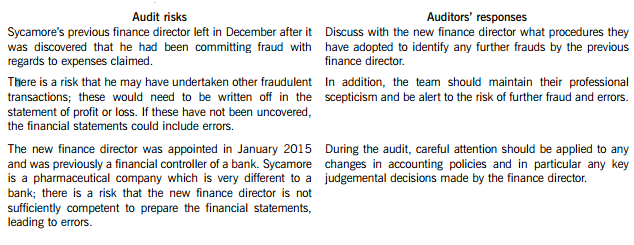

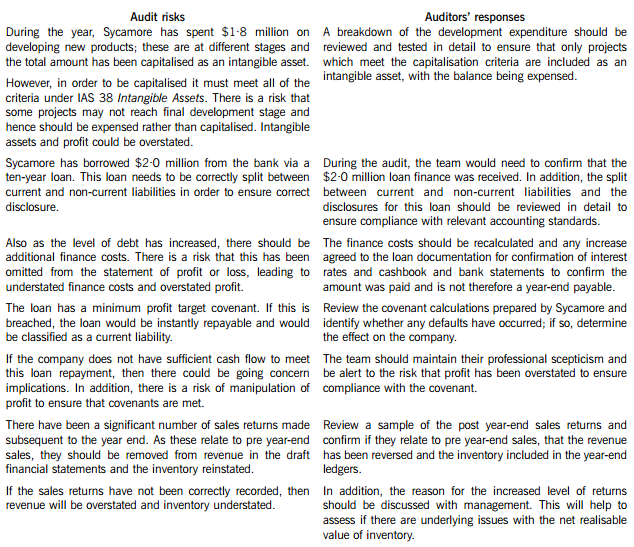

You are the audit supervisor of Maple & Co and are currently planning the audit of an existing client, Sycamore Science Co (Sycamore), whose year end was 30 April 2015. Sycamore is a pharmaceutical company, which manufactures and supplies a wide range of medical supplies. The draft financial statements show revenue of $35·6 million and profit before tax of $5·9 million.

Sycamore’s previous finance director left the company in December 2014 after it was discovered that he had been claiming fraudulent expenses from the company for a significant period of time. A new finance director was appointed in January 2015 who was previously a financial controller of a bank, and she has expressed surprise that Maple & Co had not uncovered the fraud during last year’s audit.

During the year Sycamore has spent $1·8 million on developing several new products. These projects are at different stages of development and the draft financial statements show the full amount of $1·8 million within intangible assets. In order to fund this development, $2·0 million was borrowed from the bank and is due for repayment over a ten-year period. The bank has attached minimum profit targets as part of the loan covenants.

The new finance director has informed the audit partner that since the year end there has been an increased number of sales returns and that in the month of May over $0·5 million of goods sold in April were returned.

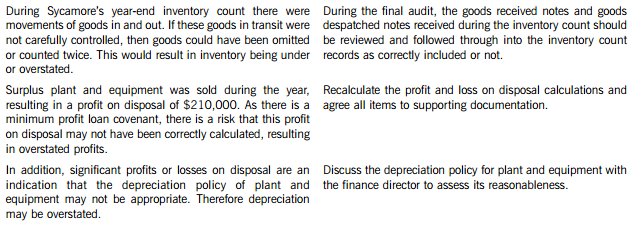

Maple & Co attended the year-end inventory count at Sycamore’s warehouse. The auditor present raised concerns that during the count there were movements of goods in and out the warehouse and this process did not seem well controlled.

During the year, a review of plant and equipment in the factory was undertaken and surplus plant was sold, resulting in a profit on disposal of $210,000.

Required:

(a) State Maples & Co’s responsibilities in relation to the prevention and detection of fraud and error. (4 marks)

(b) Describe SIX audit risks, and explain the auditor’s response to each risk, in planning the audit of Sycamore Science Co. (12 marks)

(c) Sycamore’s new finance director has read about review engagements and is interested in the possibility of Maple & Co undertaking these in the future. However, she is unsure how these engagements differ from an external audit and how much assurance would be gained from this type of engagement.

Required:

(i) Explain the purpose of review engagements and how these differ from external audits; and (2 marks)

(ii) Describe the level of assurance provided by external audits and review engagements. (2 marks)

正确答案:(a) Fraud responsibility

Maple & Co must conduct an audit in accordance with ISA 240 The Auditor’s Responsibilities Relating to Fraud in an Audit of Financial Statements and are responsible for obtaining reasonable assurance that the financial statements taken as a whole are free from material misstatement, whether caused by fraud or error.

In order to fulfil this responsibility, Maple & Co is required to identify and assess the risks of material misstatement of the financial statements due to fraud.

They need to obtain sufficient appropriate audit evidence regarding the assessed risks of material misstatement due to fraud, through designing and implementing appropriate responses. In addition, Maple & Co must respond appropriately to fraud or suspected fraud identified during the audit.

When obtaining reasonable assurance, Maple & Co is responsible for maintaining professional scepticism throughout the audit, considering the potential for management override of controls and recognising the fact that audit procedures which are effective in detecting error may not be effective in detecting fraud.

To ensure that the whole engagement team is aware of the risks and responsibilities for fraud and error, ISAs require that a discussion is held within the team. For members not present at the meeting, Sycamore’s audit engagement partner should determine which matters are to be communicated to them.

(b) Audit risks and auditors’ responses

(c) (i) Review engagements

Review engagements are often undertaken as an alternative to an audit, and involve a practitioner reviewing financial data, such as six-monthly figures. This would involve the practitioner undertaking procedures to state whether anything has come to their attention which causes the practitioner to believe that the financial data is not in accordance with the financial reporting framework.

A review engagement differs to an external audit in that the procedures undertaken are not nearly as comprehensive as those in an audit, with procedures such as analytical review and enquiry used extensively. In addition, the practitioner does not need to comply with ISAs as these only relate to external audits.

(ii) Levels of assurance

The level of assurance provided by audit and review engagements is as follows:

External audit – A high but not absolute level of assurance is provided, this is known as reasonable assurance. This provides comfort that the financial statements present fairly in all material respects (or are true and fair) and are free of material misstatements.

Review engagements – where an opinion is being provided, the practitioner gathers sufficient evidence to be satisfied that the subject matter is plausible; in this case negative assurance is given whereby the practitioner confirms that nothing has come to their attention which indicates that the subject matter contains material misstatements.

-

第8题:

You are the audit manager of Chestnut & Co and are reviewing the key issues identified in the files of two audit clients.

Palm Industries Co (Palm)

Palm’s year end was 31 March 2015 and the draft financial statements show revenue of $28·2 million, receivables of $5·6 million and profit before tax of $4·8 million. The fieldwork stage for this audit has been completed.

A customer of Palm owed an amount of $350,000 at the year end. Testing of receivables in April highlighted that no amounts had been paid to Palm from this customer as they were disputing the quality of certain goods received from Palm. The finance director is confident the issue will be resolved and no allowance for receivables was made with regards to this balance.

Ash Trading Co (Ash)

Ash is a new client of Chestnut & Co, its year end was 31 January 2015 and the firm was only appointed auditors in February 2015, as the previous auditors were suddenly unable to undertake the audit. The fieldwork stage for this audit is currently ongoing.

The inventory count at Ash’s warehouse was undertaken on 31 January 2015 and was overseen by the company’s internal audit department. Neither Chestnut & Co nor the previous auditors attended the count. Detailed inventory records were maintained but it was not possible to undertake another full inventory count subsequent to the year end.

The draft financial statements show a profit before tax of $2·4 million, revenue of $10·1 million and inventory of $510,000.

Required:

For each of the two issues:

(i) Discuss the issue, including an assessment of whether it is material;

(ii) Recommend ONE procedure the audit team should undertake to try to resolve the issue; and

(iii) Describe the impact on the audit report if the issue remains UNRESOLVED.

Notes:

1 The total marks will be split equally between each of the two issues.

2 Audit report extracts are NOT required.

正确答案:Audit reports

Palm Industries Co (Palm)

(i) A customer of Palm’s owing $350,000 at the year end has not made any post year-end payments as they are disputing the quality of goods received. No allowance for receivables has been made against this balance. As the balance is being disputed, there is a risk of incorrect valuation as some or all of the receivable balance is overstated, as it may not be paid.

This $350,000 receivables balance represents 1·2% (0·35/28·2m) of revenue, 6·3% (0·35/5·6m) of receivables and 7·3% (0·35/4·8m) of profit before tax; hence this is a material issue.

(ii) A procedure to adopt includes:

– Review whether any payments have subsequently been made by this customer since the audit fieldwork was completed.

– Discuss with management whether the issue of quality of goods sold to the customer has been resolved, or whether it is still in dispute.

– Review the latest customer correspondence with regards to an assessment of the likelihood of the customer making payment.

(iii) If management refuses to provide against this receivable, the audit report will need to be modified. As receivables are overstated and the error is material but not pervasive a qualified opinion would be necessary.

A basis for qualified opinion paragraph would be needed and would include an explanation of the material misstatement in relation to the valuation of receivables and the effect on the financial statements. The opinion paragraph would be qualified ‘except for’.

Ash Trading Co (Ash)

(i) Chestnut & Co was only appointed as auditors subsequent to Ash’s year end and hence did not attend the year-end inventory count. Therefore, they have not been able to gather sufficient and appropriate audit evidence with regards to the completeness and existence of inventory.

Inventory is a material amount as it represents 21·3% (0·51/2·4m) of profit before tax and 5% (0·51/10·1m) of revenue; hence this is a material issue.

(ii) A procedure to adopt includes:

– Review the internal audit reports of the inventory count to identify the level of adjustments to the records to assess the reasonableness of relying on the inventory records.

– Undertake a sample check of inventory in the warehouse and compare to the inventory records and then from inventory records to the warehouse, to assess the reasonableness of the inventory records maintained by Ash.

(iii) The auditors will need to modify the audit report as they are unable to obtain sufficient appropriate evidence in relation to inventory which is a material but not pervasive balance. Therefore a qualified opinion will be required.

A basis for qualified opinion paragraph will be required to explain the limitation in relation to the lack of evidence over inventory. The opinion paragraph will be qualified ‘except for’.

-

第9题:

Text 1 Ruth Simmons joined Goldman Sachs's board as an outside director in January 2000;a year later she became president of Brown University.For the rest of the decade she apparently managed both roles without attracting much criticism.But by the end of 2009 Ms.Simmons was under fire for having sat on Goldman's compensation committee;how could she have let those enormous bonus payouts pass unremarked?By February the next year Ms.Simmons had left the board.The position was just taking up too much time,she said.Outside directors are supposed to serve as helpful,yet less biased,advisers on a firm's board.Having made their wealth and their reputations elsewhere,they presumably have enough independence to disagree with the chief executive's proposals.If the sky,and the share price,is falling,outside directors should be able to give advice based on having weathered their own crises.The researchers from Ohio University used a database that covered more than 10,000 firms and more than 64,000 different directors between 1989 and 2004.Then they simply checked which directors stayed from one proxy statement to the next.The most likely reason for departing a board was age,so the researchers concentrated on those“surprise”disappearances by directors under the age of 70.They found that after a surprise departure,the probability that the company will subsequently have to restate earnings increases by nearly 20%.The likelihood of being named in a federal classaction lawsuit also increases,and the stock is likely to perform worse.The effect tended to be larger for larger firms.Although a correlation between them leaving and subsequent bad performance at the firm is suggestive,it does not mean that such directors are always jumping off a sinking ship.Often they“trade up,”leaving riskier,smaller firms for larger and more stable firms.But the researchers believe that outside directors have an easier time of avoiding a blow to their reputations if they leave a firm before bad news break,even if a review of history shows they were on the board at the time any wrongdoing occurred.Firms who want to keep their outside directors through tough times may have to create incentives.Otherwise outside directors will follow the example of Ms.Simmons,once again very popular on campus.

The author's attitude toward the role of outside directors is_____A.permissive

B.positive

C.scornful

D.critical答案:B解析:态度题【命题思路】本题需要在理解文章主旨要义的前提下能够识别出作者对外部董事的态度。态度有正向答案,也有负向答案,此题首先考查考生锁定哪个方向的答案;其次考查考生在方向正确的基础上结合原文具体信息进行判断,从而得出作者对外部董事所持有的态度。【直击答案】根据题干信息“The author's attitude”和“the roleof outside directors”定位到第二段“Outside directors…on a firm's board.”。其中原文中的“be supposed to”等于题干中的“The author's attitude”,“serve as”等于题干中的“the role”。根据这句可知“外部董事在公司中应扮演有益而又相对公正的顾问角色。”由此可以判断出作者对外部董事这一角色持肯定态度。另外根据文章最后一段可知“想要在困难时期留住外部董事的公司可能不得不采取一些激励政策。”这说明外部董事对公司还是有积极作用的,综合全文,B项正确。【干扰排除】根据对文章第二段分析可知作者对外部董事的态度应是正向的,故C项和D项感情色彩错误,均不选。纵观整篇文章,作者只是对外部董事进行客观描述,并没有宽容放纵的态度,故A项错误。长难句解析 -

第10题:

Which segment would benefit from integrating the internal systems of a company, including those for inventory, payment processing, marketing, accounts, and order tracking?()

- A、 supply chain logistics

- B、 banking administration

- C、 retail supplier

- D、 healthcare administration

正确答案:A -

第11题:

单选题ou are the Exchange administrator for the Xxx Corporation’s Exchange 2010 organization.Xxx has recently merged with another corporation.The Exchange organization must comply with new legal and regulatory requirements.You must ensure that all e-mail messages that contain at least one recipient or sender who is a member of the tax@Xxx distribution list and which pass through the Hub Transport server in the Xxx Corporation, will store a copy of the message in an auditor’s mailbox. Which cmdlet should you use?()ASet-JournalRule -Name Tax Communications -JournalEmailAddress ’Auditor@Xxx ’ -Scope Internal -Recipient tax@Xxx -Enabled $True

BSet-JournalRule -Name Tax Communications -JournalEmailAddress ’Auditor@Xxx ’ -Scope Global -Recipient tax@Xxx -Enabled $True

CSet-JournalRule -Name Tax Communications -JournalEmailAddress ’Auditor@Xxx ’ -Scope External -Recipient tax@Xxx -Enabled $True

DNew-JournalRule -Name Tax Communications -JournalEmailAddress ’Auditor@Xxx ’ Scope Global -Recipient tax@Xxx -Enabled $True

正确答案: A解析: 暂无解析 -

第12题:

单选题A seaman dies during a voyage. What is NOT required to be entered into the Official Log? ()AStatement that the Master has taken custody of the deceased's MMD and passport

BAn inventory of the money and property

CStatement of the wages due

DStatement as to the total deductions to be made from the wages

正确答案: C解析: 暂无解析 -

第13题:

(ii) Audit work on after-date bank transactions identified a transfer of cash from Batik Co. The audit senior has

documented that the finance director explained that Batik commenced trading on 7 October 2005, after

being set up as a wholly-owned foreign subsidiary of Jinack. No other evidence has been obtained.

(4 marks)

Required:

Identify and comment on the implications of the above matters for the auditor’s report on the financial

statements of Jinack Co for the year ended 30 September 2005 and, where appropriate, the year ending

30 September 2006.

NOTE: The mark allocation is shown against each of the matters.

正确答案:

(ii) Wholly-owned foreign subsidiary

■ The cash transfer is a non-adjusting post balance sheet event. It indicates that Batik was trading after the balance

sheet date. However, that does not preclude Batik having commenced trading before the year end.

■ The finance director’s oral representation is wholly insufficient evidence with regard to the existence (or otherwise)

of Batik at 30 September 2005. If it existed at the balance sheet date its financial statements should have been

consolidated (unless immaterial).

■ The lack of evidence that might reasonably be expected to be available (e.g. legal papers, registration payments,

etc) suggests a limitation on the scope of the audit.

■ If such evidence has been sought but not obtained then the limitation is imposed by the entity (rather than by

circumstances).

■ Whilst the transaction itself may not be material, the information concerning the existence of Batik may be material

to users and should therefore be disclosed (as a non-adjusting event). The absence of such disclosure, if the

auditor considered necessary, would result in a qualified ‘except for’, opinion.

Tutorial note: Any matter that is considered sufficiently material to be worthy of disclosure as a non-adjusting

event must result in such a qualified opinion if the disclosure is not made.

■ If Batik existed at the balance sheet date and had material assets and liabilities then its non-consolidation would

have a pervasive effect. This would warrant an adverse opinion.

■ Also, the nature of the limitation (being imposed by the entity) could have a pervasive effect if the auditor is

suspicious that other audit evidence has been withheld. In this case the auditor should disclaim an opinion. -

第14题:

(b) You are the audit manager of Johnston Co, a private company. The draft consolidated financial statements for

the year ended 31 March 2006 show profit before taxation of $10·5 million (2005 – $9·4 million) and total

assets of $55·2 million (2005 – $50·7 million).

Your firm was appointed auditor of Tiltman Co when Johnston Co acquired all the shares of Tiltman Co in March

2006. Tiltman’s draft financial statements for the year ended 31 March 2006 show profit before taxation of

$0·7 million (2005 – $1·7 million) and total assets of $16·1 million (2005 – $16·6 million). The auditor’s

report on the financial statements for the year ended 31 March 2005 was unmodified.

You are currently reviewing two matters that have been left for your attention on the audit working paper files for

the year ended 31 March 2006:

(i) In December 2004 Tiltman installed a new computer system that properly quantified an overvaluation of

inventory amounting to $2·7 million. This is being written off over three years.

(ii) In May 2006, Tiltman’s head office was relocated to Johnston’s premises as part of a restructuring.

Provisions for the resulting redundancies and non-cancellable lease payments amounting to $2·3 million

have been made in the financial statements of Tiltman for the year ended 31 March 2006.

Required:

Identify and comment on the implications of these two matters for your auditor’s reports on the financial

statements of Johnston Co and Tiltman Co for the year ended 31 March 2006. (10 marks)

正确答案:

(b) Tiltman Co

Tiltman’s total assets at 31 March 2006 represent 29% (16·1/55·2 × 100) of Johnston’s total assets. The subsidiary is

therefore material to Johnston’s consolidated financial statements.

Tutorial note: Tiltman’s profit for the year is not relevant as the acquisition took place just before the year end and will

therefore have no impact on the consolidated income statement. Calculations of the effect on consolidated profit before

taxation are therefore inappropriate and will not be awarded marks.

(i) Inventory overvaluation

This should have been written off to the income statement in the year to 31 March 2005 and not spread over three

years (contrary to IAS 2 ‘Inventories’).

At 31 March 2006 inventory is overvalued by $0·9m. This represents all Tiltmans’s profit for the year and 5·6% of

total assets and is material. At 31 March 2005 inventory was materially overvalued by $1·8m ($1·7m reported profit

should have been a $0·1m loss).

Tutorial note: 1/3 of the overvaluation was written off in the prior period (i.e. year to 31 March 2005) instead of $2·7m.

That the prior period’s auditor’s report was unmodified means that the previous auditor concurred with an incorrect

accounting treatment (or otherwise gave an inappropriate audit opinion).

As the matter is material a prior period adjustment is required (IAS 8 ‘Accounting Policies, Changes in Accounting

Estimates and Errors’). $1·8m should be written off against opening reserves (i.e. restated as at 1 April 2005).

(ii) Restructuring provision

$2·3m expense has been charged to Tiltman’s profit and loss in arriving at a draft profit of $0·7m. This is very material.

(The provision represents 14·3% of Tiltman’s total assets and is material to the balance sheet date also.)

The provision for redundancies and onerous contracts should not have been made for the year ended 31 March 2006

unless there was a constructive obligation at the balance sheet date (IAS 37 ‘Provisions, Contingent Liabilities and

Contingent Assets’). So, unless the main features of the restructuring plan had been announced to those affected (i.e.

redundancy notifications issued to employees), the provision should be reversed. However, it should then be disclosed

as a non-adjusting post balance sheet event (IAS 10 ‘Events After the Balance Sheet Date’).

Given the short time (less than one month) between acquisition and the balance sheet it is very possible that a

constructive obligation does not arise at the balance sheet date. The relocation in May was only part of a restructuring

(and could be the first evidence that Johnston’s management has started to implement a restructuring plan).

There is a risk that goodwill on consolidation of Tiltman may be overstated in Johnston’s consolidated financial

statements. To avoid the $2·3 expense having a significant effect on post-acquisition profit (which may be negligible

due to the short time between acquisition and year end), Johnston may have recognised it as a liability in the

determination of goodwill on acquisition.

However, the execution of Tiltman’s restructuring plan, though made for the year ended 31 March 2006, was conditional

upon its acquisition by Johnston. It does not therefore represent, immediately before the business combination, a

present obligation of Johnston. Nor is it a contingent liability of Johnston immediately before the combination. Therefore

Johnston cannot recognise a liability for Tiltman’s restructuring plans as part of allocating the cost of the combination

(IFRS 3 ‘Business Combinations’).

Tiltman’s auditor’s report

The following adjustments are required to the financial statements:

■ restructuring provision, $2·3m, eliminated;

■ adequate disclosure of relocation as a non-adjusting post balance sheet event;

■ current period inventory written down by $0·9m;

■ prior period inventory (and reserves) written down by $1·8m.

Profit for the year to 31 March 2006 should be $3·9m ($0·7 + $0·9 + $2·3).

If all these adjustments are made the auditor’s report should be unmodified. Otherwise, the auditor’s report should be

qualified ‘except for’ on grounds of disagreement. If none of the adjustments are made, the qualification should still be

‘except for’ as the matters are not pervasive.

Johnston’s auditor’s report

If Tiltman’s auditor’s report is unmodified (because the required adjustments are made) the auditor’s report of Johnston

should be similarly unmodified. As Tiltman is wholly-owned by Johnston there should be no problem getting the

adjustments made.

If no adjustments were made in Tiltman’s financial statements, adjustments could be made on consolidation, if

necessary, to avoid modification of the auditor’s report on Johnston’s financial statements.

The effect of these adjustments on Tiltman’s net assets is an increase of $1·4m. Goodwill arising on consolidation (if

any) would be reduced by $1·4m. The reduction in consolidated total assets required ($0·9m + $1·4m) is therefore

the same as the reduction in consolidated total liabilities (i.e. $2·3m). $2·3m is material (4·2% consolidated total

assets). If Tiltman’s financial statements are not adjusted and no adjustments are made on consolidation, the

consolidated financial position (balance sheet) should be qualified ‘except for’. The results of operations (i.e. profit for

the period) should be unqualified (if permitted in the jurisdiction in which Johnston reports).

Adjustment in respect of the inventory valuation may not be required as Johnston should have consolidated inventory

at fair value on acquisition. In this case, consolidated total liabilities should be reduced by $2·3m and goodwill arising

on consolidation (if any) reduced by $2·3m.

Tutorial note: The effect of any possible goodwill impairment has been ignored as the subsidiary has only just been

acquired and the balance sheet date is very close to the date of acquisition. -

第15题:

(b) You are an audit manager in a firm of Chartered Certified Accountants currently assigned to the audit of Cleeves

Co for the year ended 30 September 2006. During the year Cleeves acquired a 100% interest in Howard Co.

Howard is material to Cleeves and audited by another firm, Parr & Co. You have just received Parr’s draft

auditor’s report for the year ended 30 September 2006. The wording is that of an unmodified report except for

the opinion paragraph which is as follows:

Audit opinion

As more fully explained in notes 11 and 15 impairment losses on non-current assets have not been

recognised in profit or loss as the directors are unable to quantify the amounts.

In our opinion, provision should be made for these as required by International Accounting Standard 36

(Impairment). If the provision had been so recognised the effect would have been to increase the loss before

and after tax for the year and to reduce the value of tangible and intangible non-current assets. However,

as the directors are unable to quantify the amounts we are unable to indicate the financial effect of such

omissions.

In view of the failure to provide for the impairments referred to above, in our opinion the financial statements

do not present fairly in all material respects the financial position of Howard Co as of 30 September 2006

and of its loss and its cash flows for the year then ended in accordance with International Financial Reporting

Standards.

Your review of the prior year auditor’s report shows that the 2005 audit opinion was worded identically.

Required:

(i) Critically appraise the appropriateness of the audit opinion given by Parr & Co on the financial

statements of Howard Co, for the years ended 30 September 2006 and 2005. (7 marks)

正确答案:(b) (i) Appropriateness of audit opinion given

Tutorial note: The answer points suggested by the marking scheme are listed in roughly the order in which they might

be extracted from the information presented in the question. The suggested answer groups together some of these

points under headings to give the analysis of the situation a possible structure.

Heading

■ The opinion paragraph is not properly headed. It does not state the form. of the opinion that has been given nor

the grounds for qualification.

■ The opinion ‘the financial statements do not give a true and fair view’ is an ‘adverse’ opinion.

■ That ‘provision should be made’, but has not, is a matter of disagreement that should be clearly stated as noncompliance

with IAS 36. The title of IAS 36 Impairment of Assets should be given in full.

■ The opinion should be headed ‘Disagreement on Accounting Policies – Inappropriate Accounting Method – Adverse

Opinion’.

1 ISA 250 does not specify with whom agreement should be reached but presumably with those charged with corporate governance (e.g audit committee or

2 other supervisory board).

20

6D–INTBA

Paper 3.1INT

Content

■ It is appropriate that the opinion paragraph should refer to the note(s) in the financial statements where the matter

giving rise to the modification is more fully explained. However, this is not an excuse for the audit opinion being

‘light’ on detail. For example, the reason for impairment could be summarised in the auditor’s report.

■ The effects have not been quantified, but they should be quantifiable. The maximum possible loss would be the

carrying amount of the non-current assets identified as impaired.

■ It is not clear why the directors have been ‘unable to quantify the amounts’. Since impairments should be

quantifiable any ‘inability’ suggest a limitation in scope of the audit, in which case the opinion should be disclaimed

(or ‘except for’) on grounds of lack of evidence rather than disagreement.

■ The wording is confusing. ‘Failure to provide’ suggests disagreement. However, there must be sufficient evidence

to support any disagreement. Although the directors cannot quantify the amounts it seems the auditors must have

been able to (estimate at least) in order to form. an opinion that the amounts involved are sufficiently material to

warrant a qualification.

■ The first paragraph refers to ‘non-current assets’. The second paragraph specifies ‘tangible and intangible assets’.

There is no explanation why or how both tangible and intangible assets are impaired.

■ The first paragraph refers to ‘profit or loss’ and the second and third paragraphs to ‘loss’. It may be clearer if the

first paragraph were to refer to recognition in the income statement.

■ It is not clear why the failure to recognise impairment warrants an adverse opinion rather than ‘except for’. The

effects of non-compliance with IAS 36 are to overstate the carrying amount(s) of non-current assets (that can be

specified) and to understate the loss. The matter does not appear to be pervasive and so an adverse opinion looks

unsuitable as the financial statements as a whole are not incomplete or misleading. A loss is already being reported

so it is not that a reported profit would be turned into a loss (which is sometimes judged to be ‘pervasive’).

Prior year

■ As the 2005 auditor’s report, as previously issued, included an adverse opinion and the matter that gave rise to

the modification:

– is unresolved; and

– results in a modification of the 2006 auditor’s report,

the 2006 auditor’s report should also be modified regarding the corresponding figures (ISA 710 Comparatives).

■ The 2006 auditor’s report does not refer to the prior period modification nor highlight that the matter resulting in

the current period modification is not new. For example, the report could say ‘As previously reported and as more

fully explained in notes ….’ and state ‘increase the loss by $x (2005 – $y)’. -

第16题:

(b) State the enquiries you would make of the directors of Mulligan Co to ascertain the adequacy of the

$3 million finance requested for the new production facility. (7 marks)

正确答案:

(b) It is important to appreciate that the finance request should cover not only the cost of the construction of the new facility, but

also costs in order to get the business unit up and running, and enough cash to meet initial working capital requirements.

Mulligan Co may have sufficient cash to cover such additional expenses, but the bank will want comfort that this is the case.

Enquiries would include the following:

Who has prepared the forecast? It is important to evaluate the experience and competence of the preparer. If management

has previously prepared forecasts and capital expenditure budgets that were reliable and accurate, this adds a measure of

confidence in the preparation of the new forecast and the underlying assumptions used.

To what extent is internal finance available to cover any shortfall in the finance requirement? If there is surplus cash within

the organisation then the bank need not provide the full amount of finance necessary to start up the new business operation.

Has the cost of finance been included in the forecast? It appears that this cost is missing. Finance costs should be calculated

based on the anticipated interest rate to be applied to the loan advanced, and included in the total finance requirement.

What is the forecast operating cycle of the new business unit? In particular how long is the work in progress period, and how

much credit will be extended to customers? i.e. when will cash inflows specific to the new business unit be received? More

finance might be required to fund initial working capital shortfalls during the period when work in progress is occurring, and

before cash receipts from customers are received.

Will further raw materials be required? A request has been made for $250,000 for raw materials of timber. Other materials

may need to be purchased, for example, non-timber raw materials, and inventory of other consumables such as nuts and

bolts.

How long will the ‘initial’ inventory of raw material last? What is the planned work in progress time for the new product? More

finance may be needed to avoid a stock out of raw materials.

Construction of the new factory – is there any documentation to support the capital expenditure? For example, architect’s

plans, surveyor’s reports. This will support the accuracy of the finance requested and is an important source of evidence given

the materiality of the premises to the total amount of finance requested.

How likely is it that costs may be subject to inflation before actually being incurred? This could increase the amount of finance

required by several percentage points.

Have quotes been obtained for the new machinery to be purchased?

Purchase of new machinery – will any specific installation costs be incurred? These costs can be significant for large pieces

of capital equipment. Also, enquiries should be made regarding any delivery costs.

The budget does not appear to contain any finance request for overheads such as use of electricity during the construction

period, and hire of installation equipment. Have these overheads been included in the construction cost estimate?

Will staff need to be trained in using the new machinery? If so, any incremental costs should be included in the finance

request.

Advertising and marketing of new product – enquire of Patrick Tiler the methods that will be used to market the new product.

Some types of advertising are more of a cash drain due to their high expense e.g. television advertising is expensive and ‘up

front’ compared to magazine advertising, which is cheap and spread out. As Patrick Tiler is new to Mulligan Co, his forecast

is not based on past experience of this particular business.

LCT Bank will also consider the recoverability of the amount advanced by looking at the cash generating potential of the new

business unit. Enquiries should therefore be made regarding the likely success of the new products, for example:

– Has any market research been carried out to support the commercial viability of the new products?

– Have any contracts with retailers to carry the new products been negotiated?

– How quickly have past products generated a cash inflow?

– Is there a contingency plan in place in case the new products fail to be successful? -

第17题:

Following a competitive tender, your audit firm Cal & Co has just gained a new audit client Tirrol Co. You are the manager in charge of planning the audit work. Tirrol Co’s year end is 30 June 2009 with a scheduled date to complete the audit of 15 August 2009. The date now is 3 June 2009.

Tirrol Co provides repair services to motor vehicles from 25 different locations. All inventory, sales and purchasing systems are computerised, with each location maintaining its own computer system. The software in each location is

the same because the programs were written specifically for Tirrol Co by a reputable software house. Data from each location is amalgamated on a monthly basis at Tirrol Co’s head office to produce management and financial accounts.

You are currently planning your audit approach for Tirrol Co. One option being considered is to re-write Cal & Co’s audit software to interrogate the computerised inventory systems in each location of Tirrol Co (except for head office)

as part of inventory valuation testing. However, you have also been informed that any computer testing will have to be on a live basis and you are aware that July is a major holiday period for your audit firm.

Required:

(a) (i) Explain the benefits of using audit software in the audit of Tirrol Co; (4 marks)

(ii) Explain the problems that may be encountered in the audit of Tirrol Co and for each problem, explain

how that problem could be overcome. (10 marks)

(b) Following a discussion with the management at Tirrol Co you now understand that the internal audit department are prepared to assist with the statutory audit. Specifically, the chief internal auditor is prepared to provide you with documentation on the computerised inventory systems at Tirrol Co. The documentation provides details of the software and shows diagrammatically how transactions are processed through the inventory system. This documentation can be used to significantly decrease the time needed to understand the computer systems and enable audit software to be written for this year’s audit.

Required:

Explain how you will evaluate the computer systems documentation produced by the internal audit

department in order to place reliance on it during your audit. (6 marks)

正确答案:

(a)(i)BenefitsofusingauditsoftwareStandardsystemsatclientThesamecomputerisedsystemsandprogramsasusedinall25branchesofTirrolCo.Thismeansthatthesameauditsoftwarecanbeusedineachlocationprovidingsignificanttimesavingscomparedtothesituationwhereclientsystemsaredifferentineachlocation.UseactualcomputerfilesnotcopiesorprintoutsUseofauditsoftwaremeansthattheTirrolCo’sactualinventoryfilescanbetestedratherthanhavingtorelyonprintoutsorscreenimages.Thelattercouldbeincorrect,byaccidentorbydeliberatemistake.Theauditfirmwillhavemoreconfidencethatthe‘real’fileshavebeentested.TestmoreitemsUseofsoftwarewillmeanthatmoreinventoryrecordscanbetested–itispossiblethatallproductlinescouldbetestedforobsolescenceratherthanasampleusingmanualtechniques.Theauditorwillthereforegainmoreevidenceandhavegreaterconfidencethatinventoryisvaluedcorrectly.CostTherelativecostofusingauditsoftwaredecreasesthemoreyearsthatsoftwareisused.Anycostoverrunsthisyearcouldbeoffsetagainsttheauditfeesinfutureyearswhentheactualexpensewillbeless.(ii)ProblemsontheauditofTirrolTimescale–sixweekreportingdeadline–auditplanningTheauditreportisduetobesignedsixweeksaftertheyearend.Thismeansthattherewillbeconsiderablepressureontheauditortocompleteauditworkwithoutcompromisingstandardsbyrushingprocedures.Thisproblemcanbeovercomebycarefulplanningoftheaudit,useofexperiencedstaffandensuringotherstaffsuchassecondpartnerreviewsarebookedwellinadvance.Timescale–sixweekreportingdeadline–softwareissuesTheauditreportisduetobesignedaboutsixweeksaftertheyearend.Thismeansthatthereislittletimetowriteandtestauditsoftware,letaloneusethesoftwareandevaluatetheresultsoftesting.Thisproblemcanbealleviatedbycarefulplanning.AccesstoTirrolCo’ssoftwareanddatafilesmustbeobtainedassoonaspossibleandworkcommencedontailoringCal&Co’ssoftwarefollowingthis.Specialistcomputerauditstaffshouldbebookedassoonaspossibletoperform.thiswork.FirstyearauditcostsTherelativecostsofanauditinthefirstyearataclienttendtobegreaterduetotheadditionalworkofascertainingclientsystems.ThismeansthatCal&Comayhavealimitedbudgettodocumentsystemsincludingcomputersystems.Thisproblemcanbealleviatedtosomeextentagainbygoodauditplanning.Themanagermustalsomonitortheauditprocesscarefully,ensuringthatanyadditionalworkcausedbytheclientnotprovidingaccesstosystemsinformationincludingcomputersystemsisidentifiedandaddedtothetotalbillingcostoftheaudit.StaffholidaysMostoftheauditworkwillbecarriedoutinJuly,whichisalsothemonthwhenmanyofCal&Costafftaketheirannualholiday.Thismeansthattherewillbeashortageofauditstaff,particularlyasauditworkforTirrolCoisbeingbookedwithlittlenotice.Theproblemcanbealleviatedbybookingstaffassoonaspossibleandthenidentifyinganyshortages.Wherenecessary,staffmaybeborrowedfromotherofficesorevendifferentcountriesonasecondmentbasiswhereshortagesareacute.Non-standardsystemsTirrolCo’scomputersoftwareisnon-standard,havingbeenwrittenspecificallyfortheorganisation.Thismeansthatmoretimewillbenecessarytounderstandthesystemthanifstandardsystemswereused.Thisproblemcanbealleviatedeitherbyobtainingdocumentationfromtheclientorbyapproachingthesoftwarehouse(withTirrolCo’spermission)toseeiftheycanassistwithprovisionofinformationondatastructuresfortheinventorysystems.ProvisionofthisinformationwilldecreasethetimetakentotailorauditsoftwareforuseinTirrolCo.IssuesoflivetestingCal&Cohasbeeninformedthatinventorysystemsmustbetestedonalivebasis.Thisincreasestheriskofaccidentalamendmentordeletionofclientdatasystemscomparedtotestingcopyfiles.Tolimitthepossibilityofdamagetoclientsystems,Cal&CocanconsiderperforminginventorytestingondayswhenTirrolCoisnotoperatinge.g.weekends.Attheworst,backupsofdatafilestakenfromthepreviousdaycanbere-installedwhenCal&Co’stestingiscomplete.ComputersystemsTheclienthas25locations,witheachlocationmaintainingitsowncomputersystem.Itispossiblethatcomputersystemsarenotcommonacrosstheclientduetoamendmentsmadeatthebranchlevel.Thisproblemcanbeovercometosomeextentbyaskingstaffateachbranchwhethersystemshavebeenamendedandfocusingauditworkonmaterialbranches.UsefulnessofauditsoftwareTheuseofauditsoftwareatTirrolCodoesappeartohavesignificantproblemsthisyear.Thismeansthateveniftheauditsoftwareisready,theremaystillbesomeriskofincorrectconclusionsbeingderivedduetolackoftesting,etc.Thisproblemcanbealleviatedbyseriouslyconsideringthepossibilityofusingamanualauditthisyear.Themanagermayneedtoinvestigatewhetheramanualauditisfeasibleandifsowhetheritcouldbecompletedwithinthenecessarytimescalewithminimalauditrisk.(b)RelianceoninternalauditdocumentationTherearetwoissuestoconsider;theabilityofinternalaudittoproducethedocumentationandtheactualaccuracyofthedocumentationitself.Theabilityoftheinternalauditdepartmenttoproducethedocumentationcanbedeterminedby:–Ensuringthatthedepartmenthasstaffwhohaveappropriatequalifications.Provisionofarelevantqualificatione.g.membershipofacomputerrelatedinstitutewouldbeappropriate.–Ensuringthatthisandsimilardocumentationisproducedusingarecognisedplanandthatthedocumentationistestedpriortouse.Theuseofdifferentstaffintheinternalauditdepartmenttoproduceandtestdocumentationwillincreaseconfidenceinitsaccuracy.–Ensuringthatthedocumentationisactuallyusedduringinternalauditworkandthatproblemswithdocumentationarenotedandinvestigatedaspartofthatwork.Beinggivenaccesstointernalauditreportsontheinventorysoftwarewillprovideappropriateevidence.Regardingtheactualdocumentation:–Reviewingthedocumentationtoensurethatitappearslogicalandthattermsandsymbolsareusedconsistentlythroughout.Thiswillprovideevidencethattheflowcharts,etcshouldbeaccurate.–Comparingthedocumentationagainstthe‘live’inventorysystemtoensureitcorrectlyreflectstheinventorysystem.Thiscomparisonwillincludetracingindividualtransactionsthroughtheinventorysystems.–UsingpartofthedocumentationtoamendCal&Co’sauditsoftware,andthenensuringthatthesoftwareprocessesinventorysystemdataaccurately.However,thisstagemaybelimitedduetotheneedtouselivefilesatTirrolCo. -

第18题:

One of your audit clients is Tye Co a company providing petrol, aviation fuel and similar oil based products to the government of the country it is based in. Although the company is not listed on any stock exchange, it does follow best practice regarding corporate governance regulations. The audit work for this year is complete, apart from the matter referred to below.

As part of Tye Co’s service contract with the government, it is required to hold an emergency inventory reserve of 6,000 barrels of aviation fuel. The inventory is to be used if the supply of aviation fuel is interrupted due to unforeseen events such as natural disaster or terrorist activity.

This fuel has in the past been valued at its cost price of $15 a barrel. The current value of aviation fuel is $120 a barrel. Although the audit work is complete, as noted above, the directors of Tye Co have now decided to show the ‘real’ value of this closing inventory in the financial statements by valuing closing inventory of fuel at market value, which does not comply with relevant accounting standards. The draft financial statements of Tye Co currently show a profit of approximately $500,000 with net assets of $170 million.

Required:

(a) List the audit procedures and actions that you should now take in respect of the above matter. (6 marks)

(b) For the purposes of this section assume from part (a) that the directors have agreed to value inventory at

$15/barrel.

Having investigated the matter in part (a) above, the directors present you with an amended set of financial

statements showing the emergency reserve stated not at 6,000 barrels, but reported as 60,000 barrels. The final financial statements now show a profit following the inclusion of another 54,000 barrels of oil in inventory. When queried about the change from 6,000 to 60,000 barrels of inventory, the finance director stated that this change was made to meet expected amendments to emergency reserve requirements to be published in about six months time. The inventory will be purchased this year, and no liability will be shown in the financial statements for this future purchase. The finance director also pointed out that part of Tye Co’s contract with the government requires Tye Co to disclose an annual profit and that a review of bank loans is due in three months. Finally the finance director stated that if your audit firm qualifies the financial statements in respect of the increase in inventory, they will not be recommended for re-appointment at the annual general meeting. The finance director refuses to amend the financial statements to remove this ‘fictitious’ inventory.

Required:

(i) State the external auditor’s responsibilities regarding the detection of fraud; (4 marks)

(ii) Discuss to which groups the auditors of Tye Co could report the ‘fictitious’ aviation fuel inventory;

(6 marks)

(iii) Discuss the safeguards that the auditors of Tye Co can use in an attempt to overcome the intimidation

threat from the directors of Tye Co. (4 marks)

正确答案: