(c) Issue of bondThe club proposes to issue a 7% bond with a face value of $50 million on 1 January 2007 at a discount of 5%that will be secured on income from future ticket sales and corporate hospitality receipts, which are approximately$20 million per

题目

(c) Issue of bond

The club proposes to issue a 7% bond with a face value of $50 million on 1 January 2007 at a discount of 5%

that will be secured on income from future ticket sales and corporate hospitality receipts, which are approximately

$20 million per annum. Under the agreement the club cannot use the first $6 million received from corporate

hospitality sales and reserved tickets (season tickets) as this will be used to repay the bond. The money from the

bond will be used to pay for ground improvements and to pay the wages of players.

The bond will be repayable, both capital and interest, over 15 years with the first payment of $6 million due on

31 December 2007. It has an effective interest rate of 7·7%. There will be no active market for the bond and

the company does not wish to use valuation models to value the bond. (6 marks)

Required:

Discuss how the above proposals would be dealt with in the financial statements of Seejoy for the year ending

31 December 2007, setting out their accounting treatment and appropriateness in helping the football club’s

cash flow problems.

(Candidates do not need knowledge of the football finance sector to answer this question.)

相似考题

更多“(c) Issue of bondThe club proposes to issue a 7% bond with a face value of $50 million on 1 January 2007 at a discount of 5%that will be secured on income from future ticket sales and corporate hospitality receipts, which are approximately$20 million per ”相关问题

-

第1题:

(b) On 31 May 2007, Leigh purchased property, plant and equipment for $4 million. The supplier has agreed to

accept payment for the property, plant and equipment either in cash or in shares. The supplier can either choose

1·5 million shares of the company to be issued in six months time or to receive a cash payment in three months

time equivalent to the market value of 1·3 million shares. It is estimated that the share price will be $3·50 in

three months time and $4 in six months time.

Additionally, at 31 May 2007, one of the directors recently appointed to the board has been granted the right to

choose either 50,000 shares of Leigh or receive a cash payment equal to the current value of 40,000 shares at

the settlement date. This right has been granted because of the performance of the director during the year and

is unconditional at 31 May 2007. The settlement date is 1 July 2008 and the company estimates the fair value

of the share alternative is $2·50 per share at 31 May 2007. The share price of Leigh at 31 May 2007 is $3 per

share, and if the director chooses the share alternative, they must be kept for a period of four years. (9 marks)

Required:

Discuss with suitable computations how the above share based transactions should be accounted for in the

financial statements of Leigh for the year ended 31 May 2007.

正确答案:(b) Transactions that allow choice of settlement are accounted for as cash-settled to the extent that the entity has incurred a

liability (IFRS2 para 34). The share based transaction is treated as the issuance of a compound financial instrument. IFRS2

applies similar measurement principles to determine the value of the constituent parts of a compound instrument as that

required by IAS32 ‘Financial Instruments: Disclosure and Presentation’. The purchase of the property, plant and equipment

(PPE) and the grant to the director, both fall under this section of IFRS2 as the supplier and the director have a choice of

settlement. The fair value of the goods can be measured directly as regards the purchase of the PPE and therefore this fact

determines that the transaction is treated in a certain way. In the case of the director, the fair value of the service rendered

will be determined by the fair value of the equity instruments given and IFRS2 says that this type of share based transaction

should be dealt with in a certain way. Under IFRS2, if the fair value of the goods or services received can be measured directly

and easily then the equity element is determined by taking the fair value of the goods or services less the fair value of the

debt element of this instrument. The debt element is essentially the cash payment that will occur. If the fair value of the goods

or services is measured by reference to the fair value of the equity instruments given then the whole of the compound

instrument should be fair valued. The equity element becomes the difference between the fair value of the equity instruments

granted less the fair value of the debt component. It should take into account the fact that the counterparty must forfeit its

right to receive cash in order to receive the equity instrument.

When Leigh received the property, plant and equipment it should have recorded a liability of $4 million and an increase in

equity of $0·55 million being the difference between the value of the property, plant and equipment and the fair value of theliability. The fair value of the liability is the cash payment of $3·50 x 1·3 million shares, i.e. $4·55 million.

The accounting entry would be:

-

第2题:

(c) At 1 June 2006, Router held a 25% shareholding in a film distribution company, Wireless, a public limited

company. On 1 January 2007, Router sold a 15% holding in Wireless thus reducing its investment to a 10%

holding. Router no longer exercises significant influence over Wireless. Before the sale of the shares the net asset

value of Wireless on 1 January 2007 was $200 million and goodwill relating to the acquisition of Wireless was

$5 million. Router received $40 million for its sale of the 15% holding in Wireless. At 1 January 2007, the fair

value of the remaining investment in Wireless was $23 million and at 31 May 2007 the fair value was

$26 million. (6 marks)

Required:

Discuss how the above items should be dealt with in the group financial statements of Router for the year ended

31 May 2007.Required:

Discuss how the above items should be dealt with in the group financial statements of Router for the year ended

31 May 2007.

正确答案:

(c) The investment in Wireless is currently accounted for using the equity method of accounting under IAS28 ‘Investments in

Associates’. On the sale of a 15% holding, the investment in Wireless will be accounted for in accordance with IAS39. Router

should recognise a gain on the sale of the holding in Wireless of $7 million (Working 1). The gain comprises the following:

(i) the difference between the sale proceeds and the proportion of the net assets sold and

(ii) the goodwill disposed of.

The total gain is shown in the income statement.

The remaining 10 per cent investment will be classified as an ‘available for sale’ financial asset or at ‘fair value through profit

or loss’ financial asset. Changes in fair value for these categories are reported in equity or in the income statement respectively.

At 1 January 2007, the investment will be recorded at fair value and a gain of $1 million $(23 – 22) recorded. At 31 May

2007 a further gain of $(26 – 23) million, i.e. $3 million will be recorded. In order for the investment to be categorised as

at fair value through profit or loss, certain conditions have to be fulfilled. An entity may use this designation when doing so

results in more relevant information by eliminating or significantly reducing a measurement or recognition inconsistency (an

‘accounting mismatch’) or where a group of financial assets and/or financial liabilities is managed and its performance is

evaluated on a fair value basis, in accordance with a documented risk management or investment strategy, and information

about the assets and/ or liabilities is provided internally to the entity’s key management personnel.

-

第3题:

(b) Calculate the percentage of maximum capacity at which the zoo will break even during the year ending

30 November 2007. You should assume that 50% of the revenue from sales of ticket type ZC is attributable

to the zoo. (7 marks)

正确答案:

-

第4题:

3 You are the manager responsible for the audit of Lamont Co. The company’s principal activity is wholesaling frozen

fish. The draft consolidated financial statements for the year ended 31 March 2007 show revenue of $67·0 million

(2006 – $62·3 million), profit before taxation of $11·9 million (2006 – $14·2 million) and total assets of

$48·0 million (2006 – $36·4 million).

The following issues arising during the final audit have been noted on a schedule of points for your attention:

(a) In early 2007 a chemical leakage from refrigeration units owned by Lamont caused contamination of some of its

property. Lamont has incurred $0·3 million in clean up costs, $0·6 million in modernisation of the units to

prevent future leakage and a $30,000 fine to a regulatory agency. Apart from the fine, which has been expensed,

these costs have been capitalised as improvements. (7 marks)

Required:

For each of the above issues:

(i) comment on the matters that you should consider; and

(ii) state the audit evidence that you should expect to find,

in undertaking your review of the audit working papers and financial statements of Lamont Co for the year ended

31 March 2007.

NOTE: The mark allocation is shown against each of the three issues.

正确答案:

3 LAMONT CO

(a) Chemical leakage

(i) Matters

■ $30,000 fine is very immaterial (just 1/4% profit before tax). This is revenue expenditure and it is correct that it

has been expensed to the income statement.

■ $0·3 million represents 0·6% total assets and 2·5% profit before tax and is not material on its own. $0·6 million

represents 1·2% total assets and 5% profit before tax and is therefore material to the financial statements.

■ The $0·3 million clean-up costs should not have been capitalised as the condition of the property is not improved

as compared with its condition before the leakage occurred. Although not material in isolation this amount should

be adjusted for and expensed, thereby reducing the aggregate of uncorrected misstatements.

■ It may be correct that $0·6 million incurred in modernising the refrigeration units should be capitalised as a major

overhaul (IAS 16 Property, Plant and Equipment). However, any parts scrapped as a result of the modernisation

should be treated as disposals (i.e. written off to the income statement).

■ The carrying amount of the refrigeration units at 31 March 2007, including the $0·6 million for modernisation,

should not exceed recoverable amount (i.e. the higher of value in use and fair value less costs to sell). If it does,

an allowance for the impairment loss arising must be recognised in accordance with IAS 36 Impairment of Assets.

(ii) Audit evidence

■ A breakdown/analysis of costs incurred on the clean-up and modernisation amounting to $0·3 million and

$0·6 million respectively.

■ Agreement of largest amounts to invoices from suppliers/consultants/sub-contractors, etc and settlement thereof

traced from the cash book to the bank statement.

■ Physical inspection of the refrigeration units to confirm their modernisation and that they are in working order. (Do

they contain frozen fish?)

■ Sample of components selected from the non-current asset register traced to the refrigeration units and inspected

to ensure continuing existence.

■ $30,000 penalty notice from the regulatory agency and corresponding cash book payment/payment per the bank

statement.

■ Written management representation that there are no further penalties that should be provided for or disclosed other

than the $30,000 that has been accounted for. -

第5题:

1 Your client, Island Co, is a manufacturer of machinery used in the coal extraction industry. You are currently planning

the audit of the financial statements for the year ended 30 November 2007. The draft financial statements show

revenue of $125 million (2006 – $103 million), profit before tax of $5·6 million (2006 – $5·1 million) and total

assets of $95 million (2006 – $90 million). Your firm was appointed as auditor to Island Co for the first time in June

2007.

Island Co designs, constructs and installs machinery for five key customers. Payment is due in three instalments: 50%

is due when the order is confirmed (stage one), 25% on delivery of the machinery (stage two), and 25% on successful

installation in the customer’s coal mine (stage three). Generally it takes six months from the order being finalised until

the final installation.

At 30 November, there is an amount outstanding of $2·85 million from Jacks Mine Co. The amount is a disputed

stage three payment. Jacks Mine Co is refusing to pay until the machinery, which was installed in August 2007, is

running at 100% efficiency.

One customer, Sawyer Co, communicated in November 2007, via its lawyers with Island Co, claiming damages for

injuries suffered by a drilling machine operator whose arm was severely injured when a machine malfunctioned. Kate

Shannon, the chief executive officer of Island Co, has told you that the claim is being ignored as it is generally known

that Sawyer Co has a poor health and safety record, and thus the accident was their fault. Two orders which were

placed by Sawyer Co in October 2007 have been cancelled.

Work in progress is valued at $8·5 million at 30 November 2007. A physical inventory count was held on

17 November 2007. The chief engineer estimated the stage of completion of each machine at that date. One of the

major components included in the coal extracting machinery is now being sourced from overseas. The new supplier,

Locke Co, is located in Spain and invoices Island Co in euros. There is a trade payable of $1·5 million owing to Locke

Co recorded within current liabilities.

All machines are supplied carrying a one year warranty. A warranty provision is recognised on the balance sheet at

$2·5 million (2006 – $2·4 million). Kate Shannon estimates the cost of repairing defective machinery reported by

customers, and this estimate forms the basis of the provision.

Kate Shannon owns 60% of the shares in Island Co. She also owns 55% of Pacific Co, which leases a head office to

Island Co. Kate is considering selling some of her shares in Island Co in late January 2008, and would like the audit

to be finished by that time.

Required:

(a) Using the information provided, identify and explain the principal audit risks, and any other matters to be

considered when planning the final audit for Island Co for the year ended 30 November 2007.

Note: your answer should be presented in the format of briefing notes to be used at a planning meeting.

Requirement (a) includes 2 professional marks. (13 marks)

正确答案:

1 ISLAND CO

(a) Briefing Notes

Subject: Principal Audit Risks – Island Co

Revenue Recognition – timing

Island Co raises sales invoices in three stages. There is potential for breach of IAS 18 Revenue, which states that revenue

should only be recognised once the seller has the right to receive it, in other words the seller has performed its contractual

obligations. This right does not necessarily correspond to amounts falling due for payment in accordance with an invoice

schedule agreed with a customer as part of a contract. Island Co appears to receive payment from its customers in advance

of performing any obligation, as the stage one invoice is raised when an order is confirmed i.e. before any work has actually

taken place. This creates the potential for revenue to be recognised too early, in advance of any performance of contractual

obligation. When a payment is received in advance of performance, a liability should be recognised equal to the amount

received, representing the obligation under the contract. Therefore a significant risk is that revenue is overstated and liabilities

understated.

Tutorial note: Equivalent guidance is also provided in IAS 11 Construction Contracts and credit will be awarded where

candidates discuss revenue recognition under IAS 11 as Island Co is providing a single substantial asset for a customer

under the terms of a contract.

Disputed receivable

The amount owed from Jacks Mine Co is highly material as it represents 50·9% of profit before tax, 2·3% of revenue, and

3% of total assets. The risk is that the receivable is overstated if no impairment of the disputed receivable is recognised.

Legal claim

The claim should be investigated seriously by Island Co. The chief executive officer’s (CEO) opinion that the claim will not

result in any financial consequence for Island Co is na?ve and flippant. Damages could be awarded against Island Co if it is

found that the machinery is faulty. The recurring high level of warranty provision implies that machinery faults are fairly

common and therefore the accident could be the result of a defective machine being supplied to Sawyer Co. The risk is that

no provision is created for the potential damages under IAS 37 Provisions, Contingent Liabilities and Contingent Assets, if the

likelihood of paying damages is considered probable. Alternatively, if the likelihood of damages being paid to Sawyer Co is

considered a possibility then a disclosure note should be made in the financial statements describing the nature and possible

financial effect of the contingent liability. As discussed below, the CEO, Kate Shannon, has an incentive not to make a

provision or disclose a contingent liability due to the planned share sale post year end.

A further risk is that any legal fees associated with the claim have not been accrued within the financial statements. As the

claim has arisen during the year, the expense must be included in this year’s income statement, even if the claim is still ongoing

at the year end.

The fact that the legal claim is effectively being ignored may cast doubts on the overall integrity of senior management, and

on the integrity of the financial statements. Management representations should be approached with a degree of professional

scepticism during the audit.

Sawyer Co has cancelled two orders. If the amounts are still outstanding at the year end then it is highly likely that Sawyer

Co will not pay the invoiced amounts, and thus receivables are overstated. If the stage one payments have already been made,

then Sawyer Co may claim a refund, in which case a provision should be made to repay the amount, or a contingent liability

disclosed in a note to the financial statements.

Sawyer Co is one of only five major customers, and losing this customer could have future going concern implications for

Island Co if a new source of revenue cannot be found to replace the lost income stream from Sawyer Co. If the legal claim

becomes public knowledge, and if Island Co is found to have supplied faulty machinery, then it will be difficult to attract new

customers.

A case of this nature could bring bad publicity to Island Co, a potential going concern issue if it results in any of the five key

customers terminating orders with Island Co. The auditors should plan to extend the going concern work programme to

incorporate the issues noted above.

Inventories

Work in progress is material to the financial statements, representing 8·9% of total assets. The inventory count was held two

weeks prior to the year end. There is an inherent risk that the valuation has not been correctly rolled forward to a year end

position.

The key risk is the estimation of the stage of completion of work in progress. This is subjective, and knowledge appears to

be confined to the chief engineer. Inventory could be overvalued if the machines are assessed to be more complete than they

actually are at the year end. Absorption of labour costs and overheads into each machine is a complex calculation and must

be done consistently with previous years.

It will also be important that consumable inventories not yet utilised on a machine, e.g. screws, nuts and bolts, are correctly

valued and included as inventories of raw materials within current assets.

Overseas supplier

As the supplier is new, controls may not yet have been established over the recording of foreign currency transactions.

Inherent risk is high as the trade payable should be retranslated using the year end exchange rate per IAS 21 The Effects of

Changes in Foreign Exchange Rates. If the retranslation is not performed at the year end, the trade payable could be

significantly over or under valued, depending on the movement of the dollar to euro exchange rate between the purchase date

and the year end. The components should remain at historic cost within inventory valuation and should not be retranslated

at the year end.

Warranty provision

The warranty provision is material at 2·6% of total assets (2006 – 2·7%). The provision has increased by only $100,000,

an increase of 4·2%, compared to a revenue increase of 21·4%. This could indicate an underprovision as the percentage

change in revenue would be expected to be in line with the percentage change in the warranty provision, unless significant

improvements had been made to the quality of machines installed for customers during the year. This appears unlikely given

the legal claim by Sawyer Co, and the machines installed at Jacks Mine Co operating inefficiently. The basis of the estimate

could be understated to avoid charging the increase in the provision as an expense through the income statement. This is of

special concern given that it is the CEO and majority shareholder who estimates the warranty provision.

Majority shareholder

Kate Shannon exerts control over Island Co via a majority shareholding, and by holding the position of CEO. This greatly

increases the inherent risk that the financial statements could be deliberately misstated, i.e. overvaluation of assets,

undervaluation of liabilities, and thus overstatement of profits. The risk is severe at this year end as Kate Shannon is hoping

to sell some Island Co shares post year end. As the price that she receives for these shares will be to a large extent influenced

by the balance sheet position of the company at 30 November 2007, she has a definite interest in manipulating the financial

statements for her own personal benefit. For example:

– Not recognising a provision or contingent liability for the legal claim from Sawyer Co

– Not providing for the potentially irrecoverable receivable from Jacks Mines Co

– Not increasing the warranty provision

– Recognising revenue earlier than permitted by IAS 18 Revenue.

Related party transactions

Kate Shannon controls Island Co and also controls Pacific Co. Transactions between the two companies should be disclosed

per IAS 24 Related Party Disclosures. There is risk that not all transactions have been disclosed, or that a transaction has

been disclosed at an inappropriate value. Details of the lease contract between the two companies should be disclosed within

a note to the financial statements, in particular, any amounts owed from Island Co to Pacific Co at 30 November 2007 should

be disclosed.

Other issues

– Kate Shannon wants the audit to be completed as soon as possible, which brings forward the deadline for completion

of the audit. The audit team may not have time to complete all necessary procedures, or there may not be time for

adequate reviews to be carried out on the work performed. Detection risk, and thus audit risk is increased, and the

overall quality of the audit could be jeopardised.

– This is especially important given that this is the first year audit and therefore the audit team will be working with a

steep learning curve. Audit procedures may take longer than originally planned, yet there is little time to extend

procedures where necessary.

– Kate Shannon may also exert considerable influence on the members of the audit team to ensure that the financial

statements show the best possible position of Island Co in view of her share sale. It is crucial that the audit team

members adhere strictly to ethical guidelines and that independence is beyond question.

– Due to the seriousness of the matters noted above, a final matter to be considered at the planning stage is that a second

partner review (Engagement Quality Control Review) should be considered for the audit this year end. A suitable

independent reviewer should be indentified, and time planned and budgeted for at the end of the assignment.

Conclusion

From the range of issues discussed in these briefing notes, it can be seen that the audit of Island Co will be a relatively high

risk engagement. -

第6题:

These companies tend to issue regular __________because they seek to maximize shareholder wealth in ways aside from normal growth.A、profits

B、dividends

C、shares

D、income

参考答案:B

-

第7题:

JJG Co is planning to raise $15 million of new finance for a major expansion of existing business and is considering a rights issue, a placing or an issue of bonds. The corporate objectives of JJG Co, as stated in its Annual Report, are to maximise the wealth of its shareholders and to achieve continuous growth in earnings per share. Recent financial information on JJG Co is as follows:

Required:

(a) Evaluate the financial performance of JJG Co, and analyse and discuss the extent to which the company has achieved its stated corporate objectives of:

(i) maximising the wealth of its shareholders;

(ii) achieving continuous growth in earnings per share.

Note: up to 7 marks are available for financial analysis.(12 marks)

(b) If the new finance is raised via a rights issue at $7·50 per share and the major expansion of business has

not yet begun, calculate and comment on the effect of the rights issue on:

(i) the share price of JJG Co;

(ii) the earnings per share of the company; and

(iii) the debt/equity ratio. (6 marks)

(c) Analyse and discuss the relative merits of a rights issue, a placing and an issue of bonds as ways of raising the finance for the expansion. (7 marks)

正确答案:

AchievementofcorporateobjectivesJJGCohasshareholderwealthmaximisationasanobjective.Thewealthofshareholdersisincreasedbydividendsreceivedandcapitalgainsonsharesowned.Totalshareholderreturncomparesthesumofthedividendreceivedandthecapitalgainwiththeopeningshareprice.TheshareholdersofJJGCohadareturnof58%in2008,comparedwithareturnpredictedbythecapitalassetpricingmodelof14%.Thelowestreturnshareholdershavereceivedwas21%andthehighestreturnwas82%.Onthisbasis,theshareholdersofthecompanyhaveexperiencedasignificantincreaseinwealth.Itisdebatablewhetherthishasbeenasaresultoftheactionsofthecompany,however.Sharepricesmayincreaseirrespectiveoftheactionsanddecisionsofmanagers,orevendespitethem.Infact,lookingatthedividendpersharehistoryofthecompany,therewasoneyear(2006)wheredividendswereconstant,eventhoughearningspershareincreased.Itisalsodifficulttoknowwhenwealthhasbeenmaximised.Anotherobjectiveofthecompanywastoachieveacontinuousincreaseinearningspershare.Analysisshowsthatearningspershareincreasedeveryyear,withanaverageincreaseof14·9%.Thisobjectiveappearstohavebeenachieved.CommentonfinancialperformanceReturnoncapitalemployed(ROCE)hasbeengrowingtowardsthesectoraverageof25%onayear-by-yearbasisfrom22%in2005.Thissteadygrowthintheprimaryaccountingratiocanbecontrastedwithirregulargrowthinturnover,thereasonsforwhichareunknown.Returnonshareholders’fundshasbeenconsistentlyhigherthantheaverageforthesector.ThismaybeduemoretothecapitalstructureofJJGCothantogoodperformancebythecompany,however,inthesensethatshareholders’fundsaresmalleronabookvaluebasisthanthelong-termdebtcapital.Ineverypreviousyearbut2008thegearingofthecompanywashigherthanthesectoraverage.(b)CalculationoftheoreticalexrightspershareCurrentshareprice=$8·64pershareCurrentnumberofshares=5·5millionsharesFinancetoberaised=$15mRightsissueprice=$7·50pershareNumberofsharesissued=15m/7·50=2millionsharesTheoreticalexrightspricepershare=((5·5mx8·64)+(2mx7·50))/7·5m=$8·34pershareThesharepricewouldfallfrom$8·64to$8·34pershareHowever,therewouldbenoeffectonshareholderwealthEffectofrightsissueonearningspershareCurrentEPS=100centspershareRevisedEPS=100x5·5m/7·5m=73centspershareTheEPSwouldfallfrom100centspershareto73centspershareHowever,asmentionedearlier,therewouldbenoeffectonshareholderwealthEffectofrightsissueonthedebt/equityratioCurrentdebt/equityratio=100x20/47·5=42%Revisedmarketvalueofequity=7·5mx8·34=$62·55millionReviseddebt/equityratio=100x20/62·55=32%Thedebt/equityratiowouldfallfrom42%to32%,whichiswellbelowthesectoraveragevalueandwouldsignalareductioninfinancialrisk(c)Thecurrentdebt/equityratioofJJGCois42%(20/47·5).Althoughthisislessthanthesectoraveragevalueof50%,itismoreusefulfromafinancialriskperspectivetolookattheextenttowhichinterestpaymentsarecoveredbyprofits.Theinterestonthebondissueis$1·6million(8%of$20m),givinganinterestcoverageratioof6·1times.IfJJGCohasoverdraftfinance,theinterestcoverageratiowillbelowerthanthis,butthereisinsufficientinformationtodetermineifanoverdraftexists.Theinterestcoverageratioisnotonlybelowthesectoraverage,itisalsolowenoughtobeacauseforconcern.Whiletheratioshowsanupwardtrendovertheperiodunderconsideration,itstillindicatesthatanissueoffurtherdebtwouldbeunwise.Aplacing,oranyissueofnewsharessuchasarightsissueorapublicoffer,woulddecreasegearing.Iftheexpansionofbusinessresultsinanincreaseinprofitbeforeinterestandtax,theinterestcoverageratiowillincreaseandfinancialriskwillfall.GiventhecurrentfinancialpositionofJJGCo,adecreaseinfinancialriskiscertainlypreferabletoanincrease.Aplacingwilldiluteownershipandcontrol,providingthenewequityissueistakenupbynewinstitutionalshareholders,whilearightsissuewillnotdiluteownershipandcontrol,providingexistingshareholderstakeuptheirrights.Abondissuedoesnothaveownershipandcontrolimplications,althoughrestrictiveornegativecovenantsinbondissuedocumentscanlimittheactionsofacompanyanditsmanagers.Allthreefinancingchoicesarelong-termsourcesoffinanceandsoareappropriateforalong-terminvestmentsuchastheproposedexpansionofexistingbusiness.Equityissuessuchasaplacingandarightsissuedonotrequiresecurity.Noinformationisprovidedonthenon-currentassetsofJJGCo,butitislikelythattheexistingbondissueissecured.Ifanewbondissuewasbeingconsidered,JJGCowouldneedtoconsiderwhetherithadsufficientnon-currentassetstoofferassecurity,althoughitislikelythatnewnon-currentassetswouldbeboughtaspartofthebusinessexpansion. -

第8题:

The following trial balance relates to Sandown at 30 September 2009:

The following notes are relevant:

(i) Sandown’s revenue includes $16 million for goods sold to Pending on 1 October 2008. The terms of the sale are that Sandown will incur ongoing service and support costs of $1·2 million per annum for three years after the sale. Sandown normally makes a gross profit of 40% on such servicing and support work. Ignore the time value of money.

(ii) Administrative expenses include an equity dividend of 4·8 cents per share paid during the year.

(iii) The 5% convertible loan note was issued for proceeds of $20 million on 1 October 2007. It has an effective interest rate of 8% due to the value of its conversion option.

(iv) During the year Sandown sold an available-for-sale investment for $11 million. At the date of sale it had a

carrying amount of $8·8 million and had originally cost $7 million. Sandown has recorded the disposal of the

investment. The remaining available-for-sale investments (the $26·5 million in the trial balance) have a fair value of $29 million at 30 September 2009. The other reserve in the trial balance represents the net increase in the value of the available-for-sale investments as at 1 October 2008. Ignore deferred tax on these transactions.

(v) The balance on current tax represents the under/over provision of the tax liability for the year ended 30 September 2008. The directors have estimated the provision for income tax for the year ended 30 September 2009 at $16·2 million. At 30 September 2009 the carrying amounts of Sandown’s net assets were $13 million in excess of their tax base. The income tax rate of Sandown is 30%.

(vi) Non-current assets:

The freehold property has a land element of $13 million. The building element is being depreciated on a

straight-line basis.

Plant and equipment is depreciated at 40% per annum using the reducing balance method.

Sandown’s brand in the trial balance relates to a product line that received bad publicity during the year which led to falling sales revenues. An impairment review was conducted on 1 April 2009 which concluded that, based on estimated future sales, the brand had a value in use of $12 million and a remaining life of only three years.

However, on the same date as the impairment review, Sandown received an offer to purchase the brand for

$15 million. Prior to the impairment review, it was being depreciated using the straight-line method over a

10-year life.

No depreciation/amortisation has yet been charged on any non-current asset for the year ended 30 September

2009. Depreciation, amortisation and impairment charges are all charged to cost of sales.

Required:

(a) Prepare the statement of comprehensive income for Sandown for the year ended 30 September 2009.

(13 marks)

(b) Prepare the statement of financial position of Sandown as at 30 September 2009. (12 marks)

Notes to the financial statements are not required.

A statement of changes in equity is not required.

正确答案:

(i)IAS18Revenuerequiresthatwheresalesrevenueincludesanamountforaftersalesservicingandsupportcoststhenaproportionoftherevenueshouldbedeferred.Theamountdeferredshouldcoverthecostandareasonableprofit(inthiscaseagrossprofitof40%)ontheservices.Astheservicingandsupportisforthreeyearsandthedateofthesalewas1October2008,revenuerelatingtotwoyears’servicingandsupportprovisionmustbedeferred:($1·2millionx2/0·6)=$4million.Thisisshownas$2millioninbothcurrentandnon-currentliabilities. -

第9题:

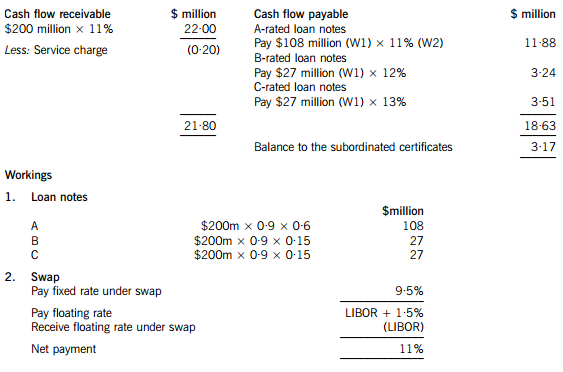

Moonstar Co is a property development company which is planning to undertake a $200 million commercial property development. Moonstar Co has had some difficulties over the last few years, with some developments not generating the expected returns and the company has at times struggled to pay its finance costs. As a result Moonstar Co’s credit rating has been lowered, affecting the terms it can obtain for bank finance. Although Moonstar Co is listed on its local stock exchange, 75% of the share capital is held by members of the family who founded the company. The family members who are shareholders do not wish to subscribe for a rights issue and are unwilling to dilute their control over the company by authorising a new issue of equity shares. Moonstar Co’s board is therefore considering other methods of financing the development, which the directors believe will generate higher returns than other recent investments, as the country where Moonstar Co is based appears to be emerging from recession.

Securitisation proposals

One of the non-executive directors of Moonstar Co has proposed that it should raise funds by means of a securitisation process, transferring the rights to the rental income from the commercial property development to a special purpose vehicle. Her proposals assume that the leases will generate an income of 11% per annum to Moonstar Co over a ten-year period. She proposes that Moonstar Co should use 90% of the value of the investment for a collateralised loan obligation which should be structured as follows:

– 60% of the collateral value to support a tranche of A-rated floating rate loan notes offering investors LIBOR plus 150 basis points

– 15% of the collateral value to support a tranche of B-rated fixed rate loan notes offering investors 12%

– 15% of the collateral value to support a tranche of C-rated fixed rate loan notes offering investors 13%

– 10% of the collateral value to support a tranche as subordinated certificates, with the return being the excess of receipts over payments from the securitisation process

The non-executive director believes that there will be sufficient demand for all tranches of the loan notes from investors. Investors will expect that the income stream from the development to be low risk, as they will expect the property market to improve with the recession coming to an end and enough potential lessees to be attracted by the new development.

The non-executive director predicts that there would be annual costs of $200,000 in administering the loan. She acknowledges that there would be interest rate risks associated with the proposal, and proposes a fixed for variable interest rate swap on the A-rated floating rate notes, exchanging LIBOR for 9·5%.

However the finance director believes that the prediction of the income from the development that the non-executive director has made is over-optimistic. He believes that it is most likely that the total value of the rental income will be 5% lower than the non-executive director has forecast. He believes that there is some risk that the returns could be so low as to jeopardise the income for the C-rated fixed rate loan note holders.

Islamic finance

Moonstar Co’s chief executive has wondered whether Sukuk finance would be a better way of funding the development than the securitisation.

Moonstar Co’s chairman has pointed out that a major bank in the country where Moonstar Co is located has begun to offer a range of Islamic financial products. The chairman has suggested that a Mudaraba contract would be the most appropriate method of providing the funds required for the investment.

Required:

(a) Calculate the amounts in $ which each of the tranches can expect to receive from the securitisation arrangement proposed by the non-executive director and discuss how the variability in rental income affects the returns from the securitisation. (11 marks)

(b) Discuss the benefits and risks for Moonstar Co associated with the securitisation arrangement that the non-executive director has proposed. (6 marks)

(c) (i) Discuss the suitability of Sukuk finance to fund the investment, including an assessment of its appeal to potential investors. (4 marks)

(ii) Discuss whether a Mudaraba contract would be an appropriate method of financing the investment and discuss why the bank may have concerns about providing finance by this method. (4 marks)

正确答案:(a) An annual cash flow account compares the estimated cash flows receivable from the property against the liabilities within the securitisation process. The swap introduces leverage into the arrangement.

The holders of the certificates are expected to receive $3·17million on $18 million, giving them a return of 17·6%. If the cash flows are 5% lower than the non-executive director has predicted, annual revenue received will fall to $20·90 million, reducing the balance available for the subordinated certificates to $2·07 million, giving a return of 11·5% on the subordinated certificates, which is below the returns offered on the B and C-rated loan notes. The point at which the holders of the certificates will receive nothing and below which the holders of the C-rated loan notes will not receive their full income will be an annual income of $18·83 million (a return of 9·4%), which is 14·4% less than the income that the non-executive director has forecast.

(b) Benefits

The finance costs of the securitisation may be lower than the finance costs of ordinary loan capital. The cash flows from the commercial property development may be regarded as lower risk than Moonstar Co’s other revenue streams. This will impact upon the rates that Moonstar Co is able to offer borrowers.

The securitisation matches the assets of the future cash flows to the liabilities to loan note holders. The non-executive director is assuming a steady stream of lease income over the next 10 years, with the development probably being close to being fully occupied over that period.

The securitisation means that Moonstar Co is no longer concerned with the risk that the level of earnings from the properties will be insufficient to pay the finance costs. Risks have effectively been transferred to the loan note holders.

Risks

Not all of the tranches may appeal to investors. The risk-return relationship on the subordinated certificates does not look very appealing, with the return quite likely to be below what is received on the C-rated loan notes. Even the C-rated loan note holders may question the relationship between the risk and return if there is continued uncertainty in the property sector.

If Moonstar Co seeks funding from other sources for other developments, transferring out a lower risk income stream means that the residual risks associated with the rest of Moonstar Co’s portfolio will be higher. This may affect the availability and terms of other borrowing.

It appears that the size of the securitisation should be large enough for the costs to be bearable. However Moonstar Co may face unforeseen costs, possibly unexpected management or legal expenses.

(c) (i) Sukuk finance could be appropriate for the securitisation of the leasing portfolio. An asset-backed Sukuk would be the same kind of arrangement as the securitisation, where assets are transferred to a special purpose vehicle and the returns and repayments are directly financed by the income from the assets. The Sukuk holders would bear the risks and returns of the relationship.

The other type of Sukuk would be more like a sale and leaseback of the development. Here the Sukuk holders would be guaranteed a rental, so it would seem less appropriate for Moonstar Co if there is significant uncertainty about the returns from the development.

The main issue with the asset-backed Sukuk finance is whether it would be as appealing as certainly the A-tranche of the securitisation arrangement which the non-executive director has proposed. The safer income that the securitisation offers A-tranche investors may be more appealing to investors than a marginally better return from the Sukuk. There will also be costs involved in establishing and gaining approval for the Sukuk, although these costs may be less than for the securitisation arrangement described above.

(ii) A Mudaraba contract would involve the bank providing capital for Moonstar Co to invest in the development. Moonstar Co would manage the investment which the capital funded. Profits from the investment would be shared with the bank, but losses would be solely borne by the bank. A Mudaraba contract is essentially an equity partnership, so Moonstar Co might not face the threat to its credit rating which it would if it obtained ordinary loan finance for the development. A Mudaraba contract would also represent a diversification of sources of finance. It would not require the commitment to pay interest that loan finance would involve.

Moonstar Co would maintain control over the running of the project. A Mudaraba contract would offer a method of obtaining equity funding without the dilution of control which an issue of shares to external shareholders would bring. This is likely to make it appealing to Moonstar Co’s directors, given their desire to maintain a dominant influence over the business.

The bank would be concerned about the uncertainties regarding the rental income from the development. Although the lack of involvement by the bank might appeal to Moonstar Co's directors, the bank might not find it so attractive. The bank might be concerned about information asymmetry – that Moonstar Co’s management might be reluctant to supply the bank with the information it needs to judge how well its investment is performing.

-

第10题:

For the year just ended, N company had an earnings of$ 2 per share and paid a dividend of $ 1. 2 on its stock. The growth rate in net income and dividend are both expected to be a constant 7 percent per year, indefinitely. N company has a Beta of 0. 8, the risk - free interest rate is 6 percent, and the market risk premium is 8 percent.

P Company is very similar to N company in growth rate, risk and dividend. payout ratio. It had 20 million shares outstanding and an earnings of $ 36 million for the year just ended. The earnings will increase to $ 38. 5 million the next year.

Requirement :

A. Calculate the expected rate of return on N company 's equity.

B. Calculate N Company 's current price-earning ratio and prospective price - earning ratio.

C. Using N company 's current price-earning ratio, value P company 's stock price.

D. Using N company 's prospective price - earning ratio, value P company 's stock price.

答案:解析:A. The expected rate of return on N company's equity =6% +0. 8*8% =12.4%

B. Current price -earning ratio = (1. 2/2) * (1 +7% )/ (12.4% -7% ) =11. 89

Prospective price - earning ratio = (1. 2/2) / (12. 4% - 70% ) =11. 11

C. P company's stock = 11. 89* 36/20 = 21. 4

D. P company's stock = 11. 11* 38. 5/20 = 21. 39

-

第11题:

Injuries from rear-end ______ were down,which could mean more than $45 million saved on accident damage per year.A.collisions

B.combats

C.contradictions

D.conflicts答案:A解析:选项A意为“碰撞”;选项B意为“战斗”;选项C意为“矛盾”;选项D意为“冲突”。根据题干,题目意为“尾部冲撞造成的伤害有所减少,这可能意味着每年节省下来超过4500万美元的意外事故损失。” rear-end collision为固定搭配,意为“追尾相撞”,故选A。

-

第12题:

单选题Mortgage and other financing income decreased $8.8 million to $18.8 for the year ended December 31, 2006.The income in 2006 was reducedAto $ 8.8 million.

Bto $18.8 million.

Cfrom $18.8 million to $8.8 million.

正确答案: A解析:

正确理解“decrease…”和“decrease to…”是本题解题的关键。前者的意思是“减少了…”,后者的意思是“减少到…”。根据原文可以知道“截止到2006年12月31日,抵押借款和其他融资收益减少了880万美元,是1880万美元”。所以,选项B正确。 -

第13题:

4 (a) Router, a public limited company operates in the entertainment industry. It recently agreed with a television

company to make a film which will be broadcast on the television company’s network. The fee agreed for the

film was $5 million with a further $100,000 to be paid every time the film is shown on the television company’s

channels. It is hoped that it will be shown on four occasions. The film was completed at a cost of $4 million and

delivered to the television company on 1 April 2007. The television company paid the fee of $5 million on

30 April 2007 but indicated that the film needed substantial editing before they were prepared to broadcast it,

the costs of which would be deducted from any future payments to Router. The directors of Router wish to

recognise the anticipated future income of $400,000 in the financial statements for the year ended 31 May

2007. (5 marks)

Required:

Discuss how the above items should be dealt with in the group financial statements of Router for the year ended

31 May 2007.

正确答案:

(a) Under IAS18 ‘Revenue’, revenue on a service contract is recognised when the outcome of the transaction can be measured

reliably. For revenue arising from the rendering of services, provided that all of the following criteria are met, revenue should

be recognised by reference to the stage of completion of the transaction at the balance sheet date (the percentage-ofcompletion

method) (IAS18 para 20):

(a) the amount of revenue can be measured reliably;

(b) it is probable that the economic benefits will flow to the seller;

(c) the stage of completion at the balance sheet date can be measured reliably; and

(d) the costs incurred, or to be incurred, in respect of the transaction can be measured reliably.

When the above criteria are not met, revenue arising from the rendering of services should be recognised only to the extent

of the expenses recognised that are recoverable. Because the only revenue which can be measured reliably is the fee for

making the film ($5 million), this should therefore be recognised as revenue in the year to 31 May 2007 and matched against

the cost of the film of $4 million. Only when the television company shows the film should any further amounts of $100,000

be recognised as there is an outstanding ‘performance’ condition in the form. of the editing that needs to take place before the

television company will broadcast the film. The costs of the film should not be carried forward and matched against

anticipated future income unless they can be deemed to be an intangible asset under IAS 38 ‘Intangible Assets’. Additionally,

when assessing revenue to be recognised in future years, the costs of the editing and Router’s liability for these costs should

be assessed.

-

第14题:

(b) One of the hotels owned by Norman is a hotel complex which includes a theme park, a casino and a golf course,

as well as a hotel. The theme park, casino, and hotel were sold in the year ended 31 May 2008 to Conquest, a

public limited company, for $200 million but the sale agreement stated that Norman would continue to operate

and manage the three businesses for their remaining useful life of 15 years. The residual interest in the business

reverts back to Norman after the 15 year period. Norman would receive 75% of the net profit of the businesses

as operator fees and Conquest would receive the remaining 25%. Norman has guaranteed to Conquest that the

net minimum profit paid to Conquest would not be less than $15 million. (4 marks)

Norman has recently started issuing vouchers to customers when they stay in its hotels. The vouchers entitle the

customers to a $30 discount on a subsequent room booking within three months of their stay. Historical

experience has shown that only one in five vouchers are redeemed by the customer. At the company’s year end

of 31 May 2008, it is estimated that there are vouchers worth $20 million which are eligible for discount. The

income from room sales for the year is $300 million and Norman is unsure how to report the income from room

sales in the financial statements. (4 marks)

Norman has obtained a significant amount of grant income for the development of hotels in Europe. The grants

have been received from government bodies and relate to the size of the hotel which has been built by the grant

assistance. The intention of the grant income was to create jobs in areas where there was significant

unemployment. The grants received of $70 million will have to be repaid if the cost of building the hotels is less

than $500 million. (4 marks)

Appropriateness and quality of discussion (2 marks)

Required:

Discuss how the above income would be treated in the financial statements of Norman for the year ended

31 May 2008.

正确答案:

(b) Property is sometimes sold with a degree of continuing involvement by the seller so that the risks and rewards of ownership

have not been transferred. The nature and extent of the buyer’s involvement will determine how the transaction is accounted

for. The substance of the transaction is determined by looking at the transaction as a whole and IAS18 ‘Revenue’ requires

this by stating that where two or more transactions are linked, they should be treated as a single transaction in order to

understand the commercial effect (IAS18 paragraph 13). In the case of the sale of the hotel, theme park and casino, Norman

should not recognise a sale as the company continues to enjoy substantially all of the risks and rewards of the businesses,

and still operates and manages them. Additionally the residual interest in the business reverts back to Norman. Also Norman

has guaranteed the income level for the purchaser as the minimum payment to Conquest will be $15 million a year. The

transaction is in substance a financing arrangement and the proceeds should be treated as a loan and the payment of profits

as interest.

The principles of IAS18 and IFRIC13 ‘Customer Loyalty Programmes’ require that revenue in respect of each separate

component of a transaction is measured at its fair value. Where vouchers are issued as part of a sales transaction and are

redeemable against future purchases, revenue should be reported at the amount of the consideration received/receivable less

the voucher’s fair value. In substance, the customer is purchasing both goods or services and a voucher. The fair value of the

voucher is determined by reference to the value to the holder and not the cost to the issuer. Factors to be taken into account

when estimating the fair value, would be the discount the customer obtains, the percentage of vouchers that would be

redeemed, and the time value of money. As only one in five vouchers are redeemed, then effectively the hotel has sold goods

worth ($300 + $4) million, i.e. $304 million for a consideration of $300 million. Thus allocating the discount between the

two elements would mean that (300 ÷ 304 x $300m) i.e. $296·1 million will be allocated to the room sales and the balance

of $3·9 million to the vouchers. The deferred portion of the proceeds is only recognised when the obligations are fulfilled.

The recognition of government grants is covered by IAS20 ‘Accounting for government grants and disclosure of government

assistance’. The accruals concept is used by the standard to match the grant received with the related costs. The relationship

between the grant and the related expenditure is the key to establishing the accounting treatment. Grants should not be

recognised until there is reasonable assurance that the company can comply with the conditions relating to their receipt and

the grant will be received. Provision should be made if it appears that the grant may have to be repaid.

There may be difficulties of matching costs and revenues when the terms of the grant do not specify precisely the expense

towards which the grant contributes. In this case the grant appears to relate to both the building of hotels and the creation of

employment. However, if the grant was related to revenue expenditure, then the terms would have been related to payroll or

a fixed amount per job created. Hence it would appear that the grant is capital based and should be matched against the

depreciation of the hotels by using a deferred income approach or deducting the grant from the carrying value of the asset

(IAS20). Additionally the grant is only to be repaid if the cost of the hotel is less than $500 million which itself would seem

to indicate that the grant is capital based. If the company feels that the cost will not reach $500 million, a provision should

be made for the estimated liability if the grant has been recognised. -

第15题:

(b) The marketing director of CTC has suggested the introduction of a new toy ‘Nellie the Elephant’ for which the

following estimated information is available:

1. Sales volumes and selling prices per unit

Year ending, 31 May 2009 2010 2011

Sales units (000) 80 180 100

Selling price per unit ($) 50 50 50

2. Nellie will generate a contribution to sales ratio of 50% throughout the three year period.

3. Product specific fixed overheads during the year ending 31 May 2009 are estimated to be $1·6 million. It

is anticipated that these fixed overheads would decrease by 10% per annum during each of the years ending

31 May 2010 and 31 May 2011.

4. Capital investment amounting to $3·9 million would be required in June 2008. The investment would have

no residual value at 31 May 2011.

5. Additional working capital of $500,000 would be required in June 2008. A further $200,000 would be

required on 31 May 2009. These amounts would be recovered in full at the end of the three year period.

6. The cost of capital is expected to be 12% per annum.

Assume all cash flows (other than where stated) arise at the end of the year.

Required:

(i) Determine whether the new product is viable purely on financial grounds. (4 marks)

正确答案:

-

第16题:

(b) You are the audit manager of Petrie Co, a private company, that retails kitchen utensils. The draft financial

statements for the year ended 31 March 2007 show revenue $42·2 million (2006 – $41·8 million), profit before

taxation of $1·8 million (2006 – $2·2 million) and total assets of $30·7 million (2006 – $23·4 million).

You are currently reviewing two matters that have been left for your attention on Petrie’s audit working paper file

for the year ended 31 March 2007:

(i) Petrie’s management board decided to revalue properties for the year ended 31 March 2007 that had

previously all been measured at depreciated cost. At the balance sheet date three properties had been

revalued by a total of $1·7 million. Another nine properties have since been revalued by $5·4 million. The

remaining three properties are expected to be revalued later in 2007. (5 marks)

Required:

Identify and comment on the implications of these two matters for your auditor’s report on the financial

statements of Petrie Co for the year ended 31 March 2007.

NOTE: The mark allocation is shown against each of the matters above.

正确答案:

(b) Implications for auditor’s report

(i) Selective revaluation of premises

The revaluations are clearly material to the balance sheet as $1·7 million and $5·4 million represent 5·5% and 17·6%

of total assets, respectively (and 23·1% in total). As the effects of the revaluation on line items in the financial statements

are clearly identified (e.g. revalued amount, depreciation, surplus in statement of changes in equity) the matter is not

pervasive.

The valuations of the nine properties after the year end provide additional evidence of conditions existing at the year end

and are therefore adjusting events per IAS 10 Events After the Balance Sheet Date.

Tutorial note: It is ‘now’ still less than three months after the year end so these valuations can reasonably be expected

to reflect year end values.

However, IAS 16 Property, Plant and Equipment does not permit the selective revaluation of assets thus the whole class

of premises would need to have been revalued for the year to 31 March 2007 to change the measurement basis for this

reporting period.

The revaluation exercise is incomplete. Unless the remaining three properties are revalued before the auditor’s report on

the financial statements for the year ended 31 March 2007 is signed off:

(1) the $7·1 revaluation made so far must be reversed to show all premises at depreciated cost as in previous years;

OR

(2) the auditor’s report would be qualified ‘except for’ disagreement regarding non-compliance with IAS 16.

When it is appropriate to adopt the revaluation model (e.g. next year) the change in accounting policy (from a cost model

to a revaluation model) should be accounted for in accordance with IAS 16 (i.e. as a revaluation).

Tutorial note: IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors does not apply to the initial

application of a policy to revalue assets in accordance with IAS 16.

Assuming the revaluation is written back, before giving an unmodified opinion, the auditor should consider why the three

properties were not revalued. In particular if there are any indicators of impairment (e.g. physical dilapidation) there

should be sufficient evidence on the working paper file to show that the carrying amount of these properties is not

materially greater than their recoverable amount (i.e. the higher of value in use and fair value less costs to sell).

If there is insufficient evidence to confirm that the three properties are not impaired (e.g. if the auditor was prevented

from inspecting the properties) the auditor’s report would be qualified ‘except for’ on grounds of limitation on scope.

If there is evidence of material impairment but management fail to write down the carrying amount to recoverable

amount the auditor’s report would be qualified ‘except for’ disagreement regarding non-compliance with IAS 36

Impairment of Assets.

-

第17题:

Apart from borrowing from hanks, a firm or an individual can obtain funds in a financial market in two ways. The most common method is to issue a (61) , such as a bond or a mortgage, which is a (62) by the borrower to pay the holder of it at (63) until a specified date, when a final payment is made. The (64) of it is the time of expiration date. The second method of raising funds is by issuing (65) , such as common stock, which are claims to share in the net income and the assets of a business.

(46)

A.debt instrument

B.letter of credit

C.letter of guarantee

D.certificate of deposit

正确答案:A

解析:句意:最常见的一种方法是发行债务工具,比如债券或抵押。debt instrument债务工具。letter of credit信用证。letter of guarantee保证函。certificate of deposit大额定期存单。 -

第18题:

Background information

B-Star is a theme park based on a popular series of children’s books. Customers pay a fixed fee to enter the park,where they can participate in a variety of activities such as riding roller-coasters, playing on slides and purchasing themed souvenirs from gift shops.

The park is open all year and has been in operation for the last seven years. It is located in a country which has very little rainfall – the park is open-air so poor weather such as rain results in a significant fall in the number of customers for that day (normally by 50%). During the last seven years there have been on average 30 days each year with rain.

B-Star is now very successful; customer numbers are increasing at approximately 15% each year.

Ticket sales

Customers purchase tickets to enter the theme park from ticket offices located outside the park. Tickets are only valid on the day of purchase. Adults and children are charged the same price for admission to the park. Tickets are preprinted and stored in each ticket office.

Tickets are purchased using either cash or credit cards.

Each ticket has a number comprising of two elements – two digits relating to the ticket office followed by six digits to identify the ticket. The last six digits are in ascending sequential order.

Cash sales

1. All ticket sales are recorded on a computer showing the amount of each sale and the number of tickets issued.

This information is transferred electronically to the accounts office.

2. Cash is collected regularly from each ticket office by two security guards. The cash is then counted by two

accounts clerks and banked on a daily basis.

3. The total cash from each ticket office is agreed to the sales information that has been transferred from each office.

4. Total cash received is then recorded in the cash book, and then the general ledger.

Credit card sales

1. Payments by credit cards are authorised online as the customers purchase their tickets.

2. Computers in each ticket office record the sales information which is transferred electronically to the accounts office.

3. Credit card sales are recorded for each credit card company in a receivables ledger.

4. When payment is received from the credit card companies, the accounts clerks agree the total sales values to the amounts received from the credit card companies, less the commission payable to those companies. The receivables ledger is updated with the payments received.

You are now commencing the planning of the annual audit of B-Star. The date is 3 June 2009 and B-Star’s year end is 30 June 2009.

Required:

(a) List and explain the purpose of the main sections of an audit strategy document and for each section, provide an example relevant to B-Star. (8 marks)

(b) (i) For the cash sales system of B-Star, identify the risks that could affect the assertion of completeness of sales and cash receipts; (4 marks)

(ii) Discuss the extent to which tests of controls and substantive procedures could be used to confirm the

assertion of completeness of income in B-Star. (6 marks)

(c) (i) List the substantive analytical procedures that may be used to give assurance on the total income from

ticket sales for one day in B-Star;

(ii) List the substantive analytical procedures that may be used to give assurance on the total income from

ticket sales in B-Star for the year. (8 marks)

(d) List the audit procedures you should perform. on the credit card receivables balance. (4 marks)

正确答案:

(b)(i)Riskaffectingcompleteness–Thecomputersystemdoesnotrecordsalesaccuratelyand/orinformationislostortransferredincorrectlyfromtheticketofficecomputertotheaccountsdepartmentcomputer.–Cashsalesarenotrecordedinthecashbook;cashisstolenbytheaccountsclerks.–Ticketsareissuedbutnopaymentisreceived–thatisthesaleisnotrecorded.–Cashisremovedbytheticketofficepersonnel,bythesecurityguardsorbytheaccountclerks.–Theaccountclerksmiscounttheamountofcashreceivedfromaticketoffice.(ii)UseoftestsofcontrolsandsubstantiveproceduresTestsofcontrolsTestsofcontrolaredesignedtoensurethatdocumentedcontrolsareoperatingeffectively.Ifcontrolsoverthecompletenessofincomewereexpectedtooperatecorrectly,thentheauditorwouldtestthosecontrols.InB-Star,whilecontrolscouldbeinoperation,e.g.theaccountclerksagreeingphysicalcashtocomputersummaries,thereisnoindicationthatthecontrolisdocumented;thatisthecomputersummaryisnotsignedtoshowthecomparisonhastakenplace.Theauditorcouldusethetestofinquiry–askingtheclerkswhetherthecontrolhasbeenused,andobservation–actuallywatchingtheclerkscarryoutthecontrols.Asnotedabovethough,lackofdocumentationofthecontroldoesmeanrelyingontestsofcontrolfortheassertioncompletenessofincomehaslimitedvalue.SubstantiveproceduresSubstantiveproceduresincludeanalyticalproceduresandotherprocedures.Analyticalproceduresincludetheanalysisofsignificantratiosandtrendsandsubsequentinvestigationofanytrendsorrelationshipsthatappeartobeabnormal.TheseprocedurescanbeusedeffectivelyinB-Starasanapproximationofincomethatcanbeobtainedfromsourcesotherthanthecashreceiptrecords.Otherprocedures,ortestsofdetail,arenormallyusedtoverifystatementoffinancialpositionassertionsandincludeobtainingauditevidencerelevanttospecificassertions.However,theycouldbeusedinB-Startotraceindividualtransactionsthroughthesales/cashsystemstoensureallticketsaleshavebeenrecorded(completenessassertion).Theuseofotherprocedureswillbetimeconsuming.(c)(i)Substantiveanalyticalprocedures–completenessofincomeforoneday–Obtainproofintotal.Ticketssoldtimespriceshouldequalday’sincome.–Comparedailysalestobudgeteddailysales(forexampleweekendsandbankholidayswouldexpectmoreincome).–Comparesaleswithpreviousdaysandaccountforchangessuchasvariationsforweather.–Comparesalestosouvenirssales(morepeopleinparkmeansmoresouvenirsales).–Compareticketofficesday-by-dayandstaffrotationtoseeifsaleslowersomeday/somestaff(attempttoidentifyfraudalso).–Comparetheexpectedsalesfromticketnumberstothetotalsalesamountfromcashandcreditsalesforeachticketoffice.(ii)Substantiveanalyticalprocedures–completenessofincomefortheyear–Obtainthesalesincomefromthepreviousyear.Multiplythisby115%toprovidearoughestimateoftheincomeforthisyear.–Obtaininformationonthenumberofdayswithrainduringthelastyear.Wherethisismoreorlessthan30,adjusttheincomeestimateby1/730downforeachdayofrainabove30or1/730upforeachdayofrainlessthan30.(Note:B-Staronlyattracts50%ofthenormalnumberofcustomersonarainyday;henceonedayofraindecreasestotalcustomersby1/730intheyear.)–Compareactualincometobudgetedincomefortheyear.Askthedirectorstoexplainanysignificantdeviations.–Obtainindustryinformationonthepopularityofthemeparks,andchangeincustomernumbers.ComparethesetrendstotheresultsobtainedbyB-Star.WhereB-Starperformedsignificantlybetterorworsethanaverage,obtainexplanationsfromthedirectors.(d)Auditofyearendcreditcardreceivable–Agreethebalancesoneachcreditcardcompany’sledgeraccounttothelistofreceivables.–Castthelistofreceivablesandagreethetotaltothetotalonthereceivablesledgercontrolaccount.–Forthelastdayofthefinancialyearandthefirstdayofthenewfinancialyear,agreetotalsalesincomefromticketofficerecordstothecashbookandreceivablesledgerensuringtheyarerecordedinthecorrectperiod.Forasampleofmaterialbalancesandarandomsampleofimmaterialitems,–ObtaindirectconfirmationfromthecreditcardcompanyoftheamountduetoB-Starusingareceivablesconfirmationletter.–Wheredirectconfirmationisnotpossible,obtainevidenceofcashreceiptaftertheendofthefinancialyear.AgreetheamountonthebankstatementspostyearendofB-Startotheamountdueinthereceivablesledger(lessanycommissiondue).–Reviewafterdatesalesdaybookfordebitnotesindicatingthatsalesmayhavebeenoverstatedintheprioryear.–ObtainthefinancialstatementsofB-Starandensurethatthereceivablesamountisdisclosedasacurrentassetnetofcommissionduetothecreditcardcompanies. -

第19题:

On 1 April 2009 Pandar purchased 80% of the equity shares in Salva. The acquisition was through a share exchange of three shares in Pandar for every five shares in Salva. The market prices of Pandar’s and Salva’s shares at 1 April

2009 were $6 per share and $3.20 respectively.

On the same date Pandar acquired 40% of the equity shares in Ambra paying $2 per share.

The summarised income statements for the three companies for the year ended 30 September 2009 are:

The following information is relevant:

(i) The fair values of the net assets of Salva at the date of acquisition were equal to their carrying amounts with the exception of an item of plant which had a carrying amount of $12 million and a fair value of $17 million. This plant had a remaining life of five years (straight-line depreciation) at the date of acquisition of Salva. All depreciation is charged to cost of sales.

In addition Salva owns the registration of a popular internet domain name. The registration, which had a

negligible cost, has a five year remaining life (at the date of acquisition); however, it is renewable indefinitely at a nominal cost. At the date of acquisition the domain name was valued by a specialist company at $20 million.

The fair values of the plant and the domain name have not been reflected in Salva’s financial statements.

No fair value adjustments were required on the acquisition of the investment in Ambra.

(ii) Immediately after its acquisition of Salva, Pandar invested $50 million in an 8% loan note from Salva. All interest accruing to 30 September 2009 had been accounted for by both companies. Salva also has other loans in issue at 30 September 2009.

(iii) Pandar has credited the whole of the dividend it received from Salva to investment income.

(iv) After the acquisition, Pandar sold goods to Salva for $15 million on which Pandar made a gross profit of 20%. Salva had one third of these goods still in its inventory at 30 September 2009. There are no intra-group current account balances at 30 September 2009.

(v) The non-controlling interest in Salva is to be valued at its (full) fair value at the date of acquisition. For this

purpose Salva’s share price at that date can be taken to be indicative of the fair value of the shareholding of the non-controlling interest.

(vi) The goodwill of Salva has not suffered any impairment; however, due to its losses, the value of Pandar’s

investment in Ambra has been impaired by $3 million at 30 September 2009.

(vii) All items in the above income statements are deemed to accrue evenly over the year unless otherwise indicated.

Required:

(a) (i) Calculate the goodwill arising on the acquisition of Salva at 1 April 2009; (6 marks)

(ii) Calculate the carrying amount of the investment in Ambra to be included within the consolidated

statement of financial position as at 30 September 2009. (3 marks)

(b) Prepare the consolidated income statement for the Pandar Group for the year ended 30 September 2009.(16 marks)

正确答案:

-

第20题:

(a) The following figures have been calculated from the financial statements (including comparatives) of Barstead for

the year ended 30 September 2009:

increase in profit after taxation 80%

increase in (basic) earnings per share 5%

increase in diluted earnings per share 2%

Required:

Explain why the three measures of earnings (profit) growth for the same company over the same period can

give apparently differing impressions. (4 marks)

(b) The profit after tax for Barstead for the year ended 30 September 2009 was $15 million. At 1 October 2008 the company had in issue 36 million equity shares and a $10 million 8% convertible loan note. The loan note will mature in 2010 and will be redeemed at par or converted to equity shares on the basis of 25 shares for each $100 of loan note at the loan-note holders’ option. On 1 January 2009 Barstead made a fully subscribed rights issue of one new share for every four shares held at a price of $2·80 each. The market price of the equity shares of Barstead immediately before the issue was $3·80. The earnings per share (EPS) reported for the year ended 30 September 2008 was 35 cents.

Barstead’s income tax rate is 25%.

Required:

Calculate the (basic) EPS figure for Barstead (including comparatives) and the diluted EPS (comparatives not required) that would be disclosed for the year ended 30 September 2009. (6 marks)

正确答案:

(a)Whilstprofitaftertax(anditsgrowth)isausefulmeasure,itmaynotgiveafairrepresentationofthetrueunderlyingearningsperformance.Inthisexample,userscouldinterpretthelargeannualincreaseinprofitaftertaxof80%asbeingindicativeofanunderlyingimprovementinprofitability(ratherthanwhatitreallyis:anincreaseinabsoluteprofit).Itispossible,evenprobable,that(someof)theprofitgrowthhasbeenachievedthroughtheacquisitionofothercompanies(acquisitivegrowth).Wherecompaniesareacquiredfromtheproceedsofanewissueofshares,orwheretheyhavebeenacquiredthroughshareexchanges,thiswillresultinagreaternumberofequitysharesoftheacquiringcompanybeinginissue.ThisiswhatappearstohavehappenedinthecaseofBarsteadastheimprovementindicatedbyitsearningspershare(EPS)isonly5%perannum.ThisexplainswhytheEPS(andthetrendofEPS)isconsideredamorereliableindicatorofperformancebecausetheadditionalprofitswhichcouldbeexpectedfromthegreaterresources(proceedsfromthesharesissued)ismatchedwiththeincreaseinthenumberofshares.Simplylookingatthegrowthinacompany’sprofitaftertaxdoesnottakeintoaccountanyincreasesintheresourcesusedtoearnthem.Anyincreaseingrowthfinancedbyborrowings(debt)wouldnothavethesameimpactonprofit(asbeingfinancedbyequityshares)becausethefinancecostsofthedebtwouldacttoreduceprofit.ThecalculationofadilutedEPStakesintoaccountanypotentialequitysharesinissue.Potentialordinarysharesarisefromfinancialinstruments(e.g.convertibleloannotesandoptions)thatmayentitletheirholderstoequitysharesinthefuture.ThedilutedEPSisusefulasitalertsexistingshareholderstothefactthatfutureEPSmaybereducedasaresultofsharecapitalchanges;inasenseitisawarningsign.InthiscasethelowerincreaseinthedilutedEPSisevidencethatthe(higher)increaseinthebasicEPShas,inpart,beenachievedthroughtheincreaseduseofdilutingfinancialinstruments.Thefinancecostoftheseinstrumentsislessthantheearningstheirproceedshavegeneratedleadingtoanincreaseincurrentprofits(andbasicEPS);however,inthefuturetheywillcausemoresharestobeissued.ThiscausesadilutionwherethefinancecostperpotentialnewshareislessthanthebasicEPS. -

第21题:

You are the audit manager of Chestnut & Co and are reviewing the key issues identified in the files of two audit clients.

Palm Industries Co (Palm)

Palm’s year end was 31 March 2015 and the draft financial statements show revenue of $28·2 million, receivables of $5·6 million and profit before tax of $4·8 million. The fieldwork stage for this audit has been completed.

A customer of Palm owed an amount of $350,000 at the year end. Testing of receivables in April highlighted that no amounts had been paid to Palm from this customer as they were disputing the quality of certain goods received from Palm. The finance director is confident the issue will be resolved and no allowance for receivables was made with regards to this balance.

Ash Trading Co (Ash)

Ash is a new client of Chestnut & Co, its year end was 31 January 2015 and the firm was only appointed auditors in February 2015, as the previous auditors were suddenly unable to undertake the audit. The fieldwork stage for this audit is currently ongoing.

The inventory count at Ash’s warehouse was undertaken on 31 January 2015 and was overseen by the company’s internal audit department. Neither Chestnut & Co nor the previous auditors attended the count. Detailed inventory records were maintained but it was not possible to undertake another full inventory count subsequent to the year end.

The draft financial statements show a profit before tax of $2·4 million, revenue of $10·1 million and inventory of $510,000.

Required:

For each of the two issues:

(i) Discuss the issue, including an assessment of whether it is material;

(ii) Recommend ONE procedure the audit team should undertake to try to resolve the issue; and

(iii) Describe the impact on the audit report if the issue remains UNRESOLVED.

Notes:

1 The total marks will be split equally between each of the two issues.

2 Audit report extracts are NOT required.

正确答案:Audit reports

Palm Industries Co (Palm)